") European finance ministers meeting in Brussels on July 11 endorsed a number of significant new policy initiatives in an attempt to accelerate the development of European capital markets over the next six months. These initiatives point to a policy priority that aims to strengthen European banks.

European finance ministers meeting in Brussels on July 11 endorsed a number of significant new policy initiatives in an attempt to accelerate the development of European capital markets over the next six months. These initiatives point to a policy priority that aims to strengthen European banks.

While concerns regarding the United Kingdom’s expected departure from the European Union (EU) may accelerate the speed with which some of these reforms are implemented, Brexit is not the most important impetus for this week’s policy decisions. European policymakers are just as focused on two additional policy priorities: sparking an investment-led economic recovery and accelerating much-needed balance-sheet repair within the banking sector.

As the recent report from the EuroGrowth Initiative indicated and as Bank of England Governor Mark Carney underscored, the current recovery lacks sufficient depth to deliver sustainable economic repair and momentum in Europe. Consumer spending needs to be augmented by significant investment in order to generate a more reliable foundation for economic growth in the near term. Success will require increased reliance on market-based funding mechanisms as well as on centralized European-level standards.

Background

Construction of a unified capital market in Europe (a Capital Markets Union) has been underway since the 2008 financial crisis. The most recent legislation (promulgated in May 2017 and finalized by the European Parliament this week) increases access to capital for early-stage firms. While this was analyzed in our June 3 blog post, this analysis takes a look at the new policy initiatives that focus on increased access to initial public offering (IPO) markets for more mature firms; increase reliance on financial technology, or FinTech, firms; and on bank balance-sheet repair.

More diversified funding sources for growing companies

The decisions taken by the finance ministers at the European Council session accelerate the shift in Europe toward increased reliance on market-based (rather than bank-based) finance for more mature firms.

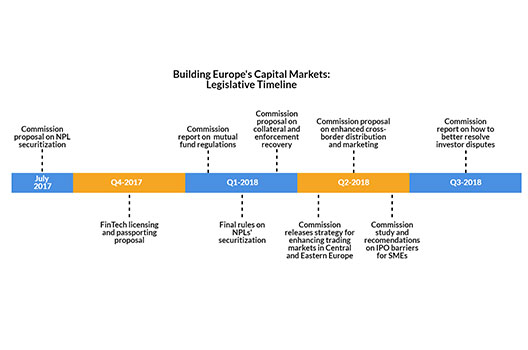

(i) IPOs: The European Commission has been asked to identify barriers for small and medium-sized enterprise (SME) listing and to undertake an impact assessment designed to identify “targeted changes in sectoral legislation in Q2 2018.”

(ii) UCITS/mutual funds: The European Commission will assess (through an impact assessment) whether new regulations can enhance the distribution and marketing of investment products within the EU. Proposals are expected in the first quarter of 2018.

(iii) Dispute resolution/investor rights: The European Commission will assess whether the EU needs a more centralized and standardized investor-protection framework. Specifically, the European Commission will deliver an impact assessment in the third quarter of 2018 regarding dispute resolution involving investors and recommending improvements in those processes. The initiative is paired with a promise to pursue aggressive enforcement against bilateral investment treaties among EU member states, thus centralizing investor protection at the EU level rather than through a member state dispute resolution processes.

(iv) Technical support/infrastructure construction: The European Commission will deliver in the second quarter of 2018 a strategy for accelerating the development of trading markets in Central and Eastern Europe.

(v) Embracing the FinTech revolution: By the end of 2017, the European Commission will issue proposals on whether (a) a special FinTech banking license should be issued and (b) whether FinTech firms should be permitted to operate on a cross-border basis within Europe.

Individually, each of these initiatives is technical and incremental. Yet taken together they present an integrated effort to expand the scale and scope of trading markets in Europe. They also imply a renewed effort to consolidate standard-setting once again in EU institutions.

Strengthening banks, softening some post-crisis reforms

European policymakers simultaneously remain committed to the bank-centered, collateralized lending economic model. Three significant initiatives were agreed in order to strengthen European banks:

(i) Clearing the non-performing loan (NPL) overhang: The finance ministers endorsed proposals to begin a discussion on how to permit banks to offload NPLs to capital markets through securitization. The European Commission immediately issued a consultative paper on the topic. Final rules are expected by the first quarter of 2018.

(ii) Accelerating collateral recovery: finance ministers authorized the Commission to propose (by the first quarter of 2018) mechanisms to expand the authority for secured creditors (mostly banks) to collect on collateral supporting soured loans from companies (including entrepreneurs, but not homeowners). Successful implementation will generate lower loss given default values for bank portfolios, thus decreasing regulatory capital requirements for banks (and expanding their ability to underwrite new loans) without changing the underlying rules.

(iii) Regulatory review for trading firms: Most investment firms operating within Europe are affiliated with banks. The post-crisis reforms in Europe extended to all investment firms the key components of the Basel III framework—which provides recommendations on banking regulations with regard to capital, market, and operational risk—through a trio of legislative instruments (the Markets in Financial Instruments Directive, the Capital Requirements Regulation, and the Capital Requirements Directive).

(iv) The finance ministers have authorized the European Commission to explore how these rules could be adjusted in order to facilitate SME access to European IPO funding markets. Proposals are expected in the second quarter of 2018.

These initiatives demonstrate a concrete policy priority aimed at strengthening European banks in two key ways. First, they facilitate loss recognition for legacy loans, thus accelerating balance-sheet repair in the banking sector. Second, they increase their role in Europe’s capital markets both as issuers (of NLP securitization vehicles) and as underwriters (under possibly relaxed regulations regarding SME IPOs). For these policies to achieve the goal of diversifying the NPL overhang away from the banking sector, policymakers will need to build a more diverse and deep capital market so that purchasers of the securitization vehicles are not just banks from different countries.

Expanded role for EU institutions

The past few years have been dominated by a significant populist backlash against centralized cross-border entities around the world. In Europe, the backlash has focused on EU entities in particular. Addressing the euro area sovereign debt crisis similarly required a shift in the political center of gravity away from Brussels and toward national capitals.

The finance ministers who met in Brussels seem to be reversing this trend with their actions. They have authorized the European Commission to propose that one of the EU’s supervisory bodies (the European Securities Markets Authority) be permitted to exercise direct supervision over firms. Various initiatives described above also imply a more proactive role for EU institutions in defining listing standards, collateral enforcement standards, and FinTech expansion standards. If these proposals move forward they will constitute the first major expansions of EU authority since 2010.

Conclusion

Success in these areas is far from assured. Implementation will require the creation of an equity culture in Europe. It also implies increased reliance on transparent market-based mechanisms for setting asset values. The shift toward market-based funding mechanisms is tempered by a parallel policy effort to increase financial support for innovative companies that promote European social and environmental policy priorities. This may mitigate some traditional political resistance to market-based finance in Europe.

The true test of the current policy shift toward market-based finance will occur in 2018 when policymakers attempt to replace or change a number of classic member state standards regarding collateral, capital cover for trading activities, and cross-border investment products. Capital Markets Union initiatives during 2018 seem poised to become the next battle between those in Europe seeking increased integration (and power sharing) and populists seeking increased authority for member states. Europe’s growth prospects may thus hinge on how the power-sharing debates evolve within the highly technical arena of financial regulation.

Barbara C. Matthews is the managing director of BCM International Regulatory Analytics LLC and a senior fellow with the Global Business and Economics Program at the Atlantic Council. You can follow her on Twitter @bcmstrategy.

Image: European Commission Vice President Valdis Dombrovskis and European Economic and Financial Affairs Commissioner Pierre Moscovici attend an European Union finance ministers meeting in Brussels, Belgium, July 11, 2017. (REUTERS/Francois Lenoir)