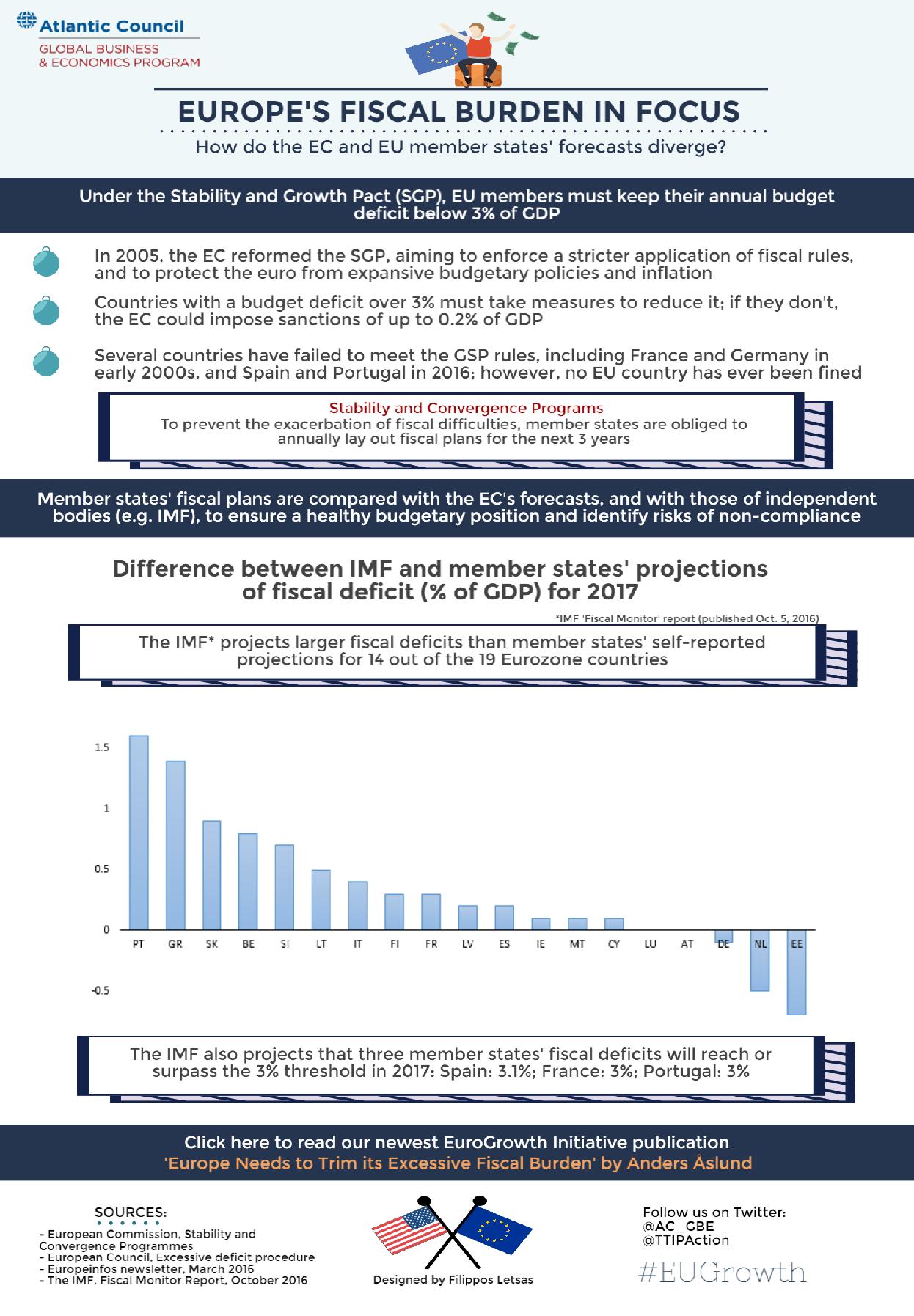

The European Union’s (EU) Stability and Growth Pact requires Eurozone countries to annually lay out their fiscal plans for the following three years. The European Commission (EC) then compares the member states’ reports with its own projections and those produced by independent bodies, such as the International Monetary Fund (IMF), to evaluate whether the member states are on track to reach their Medium-Term Budgetary Objectives (MTOs). It is important to note that Eurozone countries’ macroeconomic forecasts usually diverge, sometimes significantly, from the reports produced by the EC and the IMF.

For instance, the most recent IMF ‘Fiscal Monitor’ report predicts larger fiscal deficits (as percentage of GDP) than member states’ self-reported projections for 14 out of the 19 Eurozone countries in 2017. At the same time, European Commissioner Pierre Moscovici re-emphasized yesterday, at an Atlantic Council conference on Europe’s future post-Brexit, that fiscal discipline is a precondition for solidarity among EU member states. The close link of fiscal discipline to member states’ solidarity underscores why it is so important for the EC to be able to identify potential violations of the Stability and Growth Pact ahead of time. The persistent discrepancies between member states and independent bodies’ estimations could threaten the cohesion of the Eurozone and potentially undermine confidence in the European economic recovery.

For more information on Europe’s fiscal burden please take a look at the most recent EuroGrowth Initiative publication “Europe Needs To Trim Its Excessive Fiscal Burden”. In this issue brief, Anders Åslund explains why excessive public spending is one of the most crucial structural challenges that Europe is facing today.