Over the last ten years, the United States has become the world’s leading producer of oil and gas, going from energy import dependence to energy dominance. This shift is due to the ability to produce from shale plays, a story which started in Texas and grew to have global ramifications. In a new report, “The future of shale: The US story and its implications,” Global Energy Center Senior Fellow Ellen Scholl looks at the factors which enabled the rise of oil and gas production from shale deposits, focusing on the developments which have transpired in Texas.

This Global Energy Center report examines the Texas experience to draw lessons learned for countries hoping to utilize their shale resource potential and implications for global energy markets and geopolitics. The report concludes that the US case illustrates the challenges of operating in both a rural and an urban environment, underscores the unique advantages of the enabling ecosystem in the country, and demonstrates the importance of size and scale.

Table of contents

- Introduction

- The shale boom: how did it happen?

- The rise of shale and its impacts

- Looking forward: progress made but challenges remain

- Conclusions and lessons learned

1. Introduction

Driven by production from previously inaccessible shale deposits enabled by technological breakthroughs and advancements, US oil and gas production has risen dramatically over the last ten years. This breakthrough, which combined hydraulic fracturing, horizontal drilling, and advances in seismic technology, has enabled gas production to increase from 546.1 billion cubic meters (bcm) in 2008 to 7,345 bcm in 20181BP Statistical Review of World Energy 2018, BP, June 2018, 28, https://www.bp.com/content/dam/bp/en/corporate/pdf/energy-economics/statistical-review/bp-stats-review-2018-full-report.pdf. and oil production to rise from 5 million barrels per day in 2008 to over 9 million barrels per day in 2017,2“Crude Oil Production: Petroleum and Other Liquids,” US Energy Information Administration website, data released November 30, 2018, https://www.eia.gov/dnav/pet/pet_crd_crpdn_adc_mbblpd_a.htm. increasing to reach a record monthly output of 11.65 million barrels per day in September 2018.3Stephanie Yang and Amrith Ramkumar, “In Oil’s Huge Drop, All Signs Say Made in the U.S.A.,” Wall Street Journal, November 23, 2018, https://www.wsj.com/articles/in-oils-huge-drop-all-signs-say-made-in-the-u-s-a-1543003398. This shift in the US energy profile has major implications for the industry as well as for domestic and global markets. It also provides a crucial case study and example for other countries looking to capitalize on their shale resource potential.

The initial breakthrough in US shale production was the culmination of decades of trial and error, driven by a robust and experienced industry aided by a strong tradition of research and development efforts. The transformative events occurred in North Texas’s Barnett Shale in 2008, a relatively small play, or grouping of fields or prospects characterized by similar geological conditions, by international standards at 5,000 square miles. The techniques employed in the Barnett Shale basin were just the beginning, kicking off increases in production of natural gas as well as oil from shale plays around the country. From the Marcellus in Pennsylvania to the Bakken in North Dakota to the Eagle Ford in South Texas, hydraulic fracturing led to dramatic increases in oil and gas production from new shale plays as well as a resurgence in production from more established fields like the Permian. As a result, the United States became the largest crude oil producer in the world in 2018,4“The United State Is Now the Largest Global Crude Oil Producer,” Today in Energy, US Energy Information Administration, September 12, 2018, https://www.eia.gov/todayinenergy/detail.php?id=37053. having claimed the top spot for natural gas in 2009 and for petroleum hydrocarbons in 2013.5“United States Remains the World’s Top Producer of Petroleum and Natural Gas Hydrocarbons,” Today in Energy, US Energy Information Administration, May 21, 2018, https://www.eia.gov/todayinenergy/detail.php?id=36292#. As the United States rose to prominence as a global leader in oil and gas production, Texas rose once again to prominence as the state driving these massive increases, particularly in oil production.

Texas’s renewed role on the global stage represents a new chapter in a longer narrative of the state’s relevance to global oil (and gas) markets. While the first oil well in the United States was in Pennsylvania, not Texas, the largest oil field in the United States, the East Texas Oil Field, drove US production and US oil industry culture for generations. As chronicled in Daniel Yergin’s The Prize, perhaps the most widely known historical account of the oil industry, the Organization of the Petroleum Exporting Countries (OPEC), the international group of oil producing countries founded to manage oil market output, was modeled after the Railroad Commission, the state’s regulatory body. While the Railroad Commission has always served as a regulator, in the early years following its founding it also managed Texas’s oil output, responding to changes in price by increasing or decreasing production.

Fast forward, and the Permian is considered one of the most prolific producing fields in the world as production across the United States has increased since 2008. This shale story, which began with Texas producers and is now largely focused on the Permian, has changed oil and gas markets in profound ways. The shale revolution drove changes in US electricity markets as gas displaced coal in the power sector, while the advent of US Liquefied Natural Gas exports has driven and continues to drive the development of a more liquid global gas market. The gains in oil production enabled by the rise of shale also influenced Saudi Arabia’s production policy, resulting in the country’s late 2014 decision to push for market share. This decision resulted in a global oil supply glut that Saudi Arabia would later push OPEC to correct, resulting in a historic agreement between OPEC and non-OPEC producers to limit production in late 2016, and renewed again in December 2018. In this manner, the impacts of shale continue to reverberate in oil markets.

Over a decade after the breakthrough in the Barnett, much has changed, and many are looking to emulate what has transpired in the United States. A major remaining question is whether the US shale story will be replicated elsewhere and how shale production in China, Canada, Argentina, Bahrain, the United Arab Emirates, and elsewhere might progress. This paper, the first in a series of Global Energy Center papers on the future of shale, draws on interviews with public and private sector experts and looks at the impact of US shale production domestically, globally, and on the industry. It also examines the key enabling conditions which helped facilitate the rise of shale, factors which further enabled shale production to continue and flourish, remaining challenges for US shale producers, and lessons learned.

A major remaining question is whether the US shale story will be replicated elsewhere and how shale production in China, Canada, Argentina, Bahrain, the United Arab Emirates, and elsewhere might progress.

2. The shale boom: how did it happen?

The combination of hydraulic fracturing and horizontal drilling enabled production from previously inaccessible shale deposits, resulting in a surge of both oil and natural gas production in the United States. This production has come from new plays, like the Barnett, a gas-heavy play, and the Bakken, an oil-heavy play in North Dakota. However, the techniques employed have also enabled new production from older, more established fields like the Permian, an oil-rich play with substantial associated gas production.

Enabling environment

There are many factors that contributed to the United States, and Texas in particular, being the birthplace of the shale revolution. The state’s history of oil production contributed greatly to it being the locus of the shale revolution, in addition to the obvious factors of world class geology and luck. This revolution occurred under the umbrella of the US legacy of private ownership of mineral rights and an environment of low political risk and stable investment conditions. As Russell Gold, a Wall Street Journal senior energy reporter, concluded in his book on the shale boom, “This decidedly pro-drilling legal framework is one of the reasons fracking was an American invention. The right conditions existed in the United States to encourage oil and gas exploration and the risk taking necessary to propel the industry forward.”6Zhongmin Wang and Alan Krupnick, US Shale Gas Development: What Led to the Boom? Resources for the Future Issue Brief 13-04, May 2013, http://www.rff.org/files/sharepoint/WorkImages/Download/RFF-IB-13-04.pdf.

Existing literature on the development of shale resources has largely identified many of these factors, which are reviewed and outlined below.7Paul Stevens, The “Shale Gas Revolution”: Hype and Reality, Chatham House, September 2010, https://www.chathamhouse.org/sites/default/files/field/field_document/r_0910stevens.pdf. Countries seeking to develop their own shale resources should look to these enabling factors as baseline conditions and the progression of US shale development over time to draw lessons learned.

Regulatory, business, legal environment

Texas benefited from more than one hundred years of experience with oil and gas production, during which time it developed a stringent, tested regulatory structure which was in place at the outset of the shale revolution. This stable regulatory environment was aided by an understandable, straightforward, and predictable fiscal regime, a key factor that is not necessarily present elsewhere. The role that private ownership of mineral rights, versus ownership by the state as is the case in many oil producing countries, played in enabling the shale revolution is also well documented and hard to overstate.

Having a mature and predictable regulatory environment and a competent regulator and staff have been critical to Texas’s success. This legacy and the regulatory structure and expertise developed over time meant that in 2008 and onward there were existing rules in place considered by many in the industry as the gold standard, including Statewide Rule 13 to protect groundwater. That is not to say additional rules or updating were not necessary—rather, in 2013, the Texas Legislature adopted amendments that addressed shale development. These amendments addressed areas where additional requirements might be needed to address risks to groundwater, adding the definition of hydraulic fracturing treatment, and additional requirements for wells on which hydraulic fracturing treatments can be conducted.

Shale producers in Texas (and the United Stated more broadly) benefited from easy access to capital, and Texas also offered a low tax environment with relatively predictable cost-recovery mechanisms dictated by the Railroad Commission. The commission also offers several incentive programs for reductions in severance taxes, or state taxes imposed on the extraction of mineral resources. These include incentives for enhanced oil recovery projects,8Texas Administrative Code, Title 16, Part 1, Chapter 3, Rule 3.50, Enhanced Oil Recovery Projects—Approval and Certification for Tax Incentive, The Texas Railroad Commission, http://texreg.sos.state.tx.us/public/readtac$ext.TacPage?sl=R&app=9&p_dir=&p_rloc=&p_tloc=&p_ploc=&pg=1&p_tac=&ti=16&pt=1&ch=3&rl=50. gas produced from high cost wells,9Texas Administrative Code, Title 16, Part 1, Chapter 3, Rule 3.101, Certification for Severance Tax Exemption or Reduction for Gas Produced from High-Cost Gas Wells, The Texas Railroad Commission, http://texreg.sos.state.tx.us/public/readtac$ext.TacPage?sl=R&app=9&p_dir=&p_rloc=&p_tloc=&p_ploc=&pg=1&p_tac=&ti=16&pt=1&ch=3&rl=101. for incremental production,10Texas Administrative Code, Title 16, Part 1, Chapter 3, Rule 3.102, Tax Reduction for Incremental Production, The Texas Railroad Commission, http://texreg.sos.state.tx.us/public/readtac$ext.TacPage?sl=R&app=9&p_dir=&p_rloc=&p_tloc=&p_ploc=&pg=1&p_tac=&ti=16&pt=1&ch=3&rl=102. and for casinghead gas previously vented or flared.11Texas Administrative Code, Title 16, Part 1, Chapter 3, Rule 3.103, Certification for Severance Tax Exemption for Casinghead Gas Previously Vented or Flared, The Texas Railroad Commission, http://texreg.sos.state.tx.us/public/readtac$ext.TacPage?sl=R&app=9&p_dir=&p_rloc=&p_tloc=&p_ploc=&pg=1&p_tac=&ti=16&pt=1&ch=3&rl=103.

Legacy of drilling

The more than century-long legacy of oil and gas development in Texas enabled the rise of shale development in Texas. This legacy helped create a political economy (and constituency) of oil and gas; a culture of entrepreneurship and innovation; institutional knowledge and workforce development; and an ecosystem of services and infrastructure.

The oil and gas industry has been and continues to be an economic force in Texas as a driver of employment, a source of tax revenue, and a contributor to the state budget, creating a strong political economy in its favor. According to a report by PricewaterhouseCoopers (PwC), the industry in 2015 accounted for roughly 12 percent of total state employment, directly or indirectly supporting nearly two million jobs.12“Impacts of the Oil and Natural Gas Industry on the US Economy in 2015,” PwC, July 2017, https://www.api.org/~/media/Files/Policy/Jobs/Oil-and-Gas-2015-Economic-Impacts-Final-Cover-07-17-2017.pdf. Over the period of 2016-2017, oil production and regulation taxes contributed over $3.5 billion to Texas’s General Revenue funds, and natural gas production taxes added $1.34 billion.13Texas Comptroller of Public Accounts, “Biennial Revenue Estimate,” 2018-2019 Biennium, 85th Texas Legislature, January 2017, https://comptroller.texas.gov/transparency/reports/biennial-revenue-estimate/2018-19/. A portion of the tax revenue from oil and gas production also goes directly into the state’s Economic Stabilization Fund, commonly referred to as the rainy day fund, currently around $11 billion and expected to rise to nearly $11.9 billion in 2019, which the current state comptroller is pushing to turn into a Legacy Fund,Texas Comptroller Glenn Hegar, “A Chance to Guarantee Texas’ Legacy,” 14Texas Comptroller of Public Accounts, June 20, 2018, https://comptroller.texas.gov/about/media-center/op-eds/2018/ftd-18-06-20.php. a “severance tax based sovereign wealth fund” which could generate revenue to pay for services.15“From Volatile Severance Taxes to Sustained Revenue,” Pew Charitable Trusts, October 2016, https://www.pewtrusts.org/~/media/assets/2016/10/fromvolatileseverancetaxestosustainedrevenue.pdf. Regardless, the contribution of oil and gas to the state economy, as well as the long history of production, makes for a relatively positive—or at least accepting—relationship with the public and provides a strong contrast with many areas unaccustomed to drilling, for example New York State.

Beyond direct economic impacts, this legacy has fostered the development of institutional knowledge, a developed culture of experimentation and iterative learning, and an ecosystem to support the industry. It also means that economies of scale have developed, as well as an ecosystem of suppliers, contractors, and service providers and infrastructure, leading to cost reductions.

Institutional knowledge and expertise are housed and passed on at public universities Texas A&M and the University of Texas at Austin, which have two of the top geology and petroleum engineering schools in the country (and the world). Indeed, the Santa Rita well, which kicked off production in the Permian basin, was located on land owned by the University of Texas. This pipeline of expertise gives the state an edge in quality, proximity, and availability of skilled labor for regulators and the industry. Texas is also headquarters to international oil companies like Exxon Mobil Corp., based in Irving and operating as ExxonMobil, and independents who led the shale breakthrough and are major players in the Permian, including Pioneer Natural Resources Co. and Concho Resources Inc., the biggest oil producer in the Permian, as well as service providers like Halliburton Co.

In terms of culture, the term “wildcat” is often used to explain why or how independent producers were able to take a risk on and work through difficult geology in the Barnett Shale, paving the way for major international oil companies (IOCs) to buy in or enter into joint venture with these smaller firms. Over time, a culture of experimentation and error, encouraged by the opportunity to generate wealth for a group of investors, has developed and is now backed up by the balance sheets and economies of scale of IOCs.

Between Texas and neighboring Oklahoma and New Mexico, the state is a hub for a cluster of service industries. This includes small companies that supply machinery and equipment, water services, sand, trucking, as well as major oil and gas service companies like Halliburton, which operate globally but have the basis of their supply chains in Texas and Oklahoma. This network of contractors, service companies, and suppliers provides essential support for oil and gas development, and their proximity to fields in Texas provides a competitive advantage. To illustrate this point one article explained, “Operators engaged in onshore exploratory drilling in advanced industrialized nations in Europe are dismayed to learn they are in ‘frontier areas’ with respect to oil field services, where costs can be double or triple those prevailing in Texas or Oklahoma.”16R. L. Kleinberg, S. Paltsev, C.K.E. Ebinger, D.A. Hobbs, and T. Boersma, “Tight Oil Market Dynamics: Benchmarks, Breakeven Points, and Inelasticities,” Energy Economics 70 (2018) 70-83, https://www.sciencedirect.com/science/article/pii/S0140988317304103.

This legacy of development also resulted in an extensive system of existing infrastructure, with pipelines and gas transmission systems in place to transport oil and gas. The importance of this is highlighted by the experience in North Dakota, where much of the crude had to be transported via rail or truck in the absence of adequate existing pipeline infrastructure.

As shale production increased, so has the pipeline capacity of the United States. Crude oil pipeline mileage has increased across the United States, from less than 50,000 miles in 2004 to over 70,000 miles in 2016.17Gregory Meyer, “US Oil Pipelines Pivot South as Shale Surges,” Financial Times, March 6, 2018, https://www.ft.com/content/7a5f7236-1d94-11e8-aaca-4574d7dabfb6. The availability of infrastructure is also important in gas-rich or associated gas-rich plays, as transmission options are more limited (truck and rail not being options), increasing the cost of moving gas to market in areas with limited or nonexistent infrastructure.

The story continues

As shale production increased in traditional oil and gas states like Texas, it also spread to states with less experience with the industry, such as North Dakota, and started to garner national attention. In the following years, several factors or updates in legislation, technology, and production trends, together with the global market, helped facilitate shale production. That said, many of those interviewed for this paper noted that one of the most important factors over this period was that US conditions largely did not change, meaning that the stable and predictable regulatory environment stayed stable and predictable.

Major policy changes

At the state level, Texas tweaked its existing regulatory structure to account for fracking and passed a statewide fracking-fluid disclosure law in 2011 to alleviate public concerns with the composition of the fracking fluid. The law mandated that companies declare the chemicals used (names, not volumes) in fracking fluid on a well-by-well basis and that this information be published on FracFocus, the national hydraulic fracturing chemical disclosure registry managed by the Ground Water Protection Council and the Interstate Oil and Gas Compact Commission, whose membership includes more than half of all US states.18FracFocus, https://fracfocus.org/.

While states focused on the regulatory environment for production, two major changes occurred in Washington. The first was the advent of LNG exports from the United States, enabled by the streamlining of the approval process at the Department of Energy, and the lifting of the crude oil export ban.

In 2012, the Federal Energy Regulatory Commission (FERC) approved Cheniere Energy Inc.’s application for an LNG export facility at Sabine Pass, marking the “the Commission’s first authorization of a project that would export liquefied natural gas (LNG) from production resources within the United States.”19Federal Energy Regulatory Commission news release, “FERC Approves LNG Export Project,” April 16, 2012, https://www.ferc.gov/media/news-releases/2012/2012-2/04-16-12-sabine.asp. This was followed by US Department of Energy (DOE) efforts to streamline the permitting-approval process, which helped give the glut of US gas an outlet.20Amy Harder, “Trump Touts Natural Gas Exports Obama Approved,” Axios, June 29, 2017, https://www.axios.com/trump-touts-natural-gas-exports-obama-approved-1513388188-294269ed-e10d-4867-9575-6cc63d4299f1.html.

In 2016 US LNG exports started from Sabine Pass, totaling 0.5 billion cubic feet/day before quadrupling to 1.94 bcf/day in 2017.21“U.S. Liquified Natural Gas Exports Quadrupled in 2017,” Today in Energy, US Energy Information Administration, March 27, 2018, https://www.eia.gov/todayinenergy/detail.php?id=35512. In the first half of 2018, US LNG exports were more than double the average over the same period in the previous year, as exports continued to increase and a second facility, Dominion’s Cove Point in Maryland, shipped its first cargo in March.22“U.S. Net Natural Gas Exports in First Half of 2018 Were More than Double the 2017 Average,” Today in Energy, US Energy Information Administration, October 1, 2018, https://www.eia.gov/todayinenergy/detail.php?id=37172. The higher price for LNG in markets in Asia, Latin America, and Europe, compared to the low US Henry Hub price, provided a financial incentive and physical outlet for US gas, enabled by shale production.

However, perhaps the most dramatic change prompted by the shale revolution was the lifting of the forty-year restriction on US crude oil exports in December 2015 as part of an omnibus budget deal. The post-2014 period of historically low oil prices focused attention on the need for an export outlet for US crude, and the move provided a market for rising production and helped turn West Texas Intermediate into a global benchmark. As a result, US crude oil exports went from 520,000 barrels per day in 201623“U.S. Exports of Crude Oil and Petroleum Products More than Doubled Since 2010,” Today in Energy, US Energy Information Administration, December 26, 2017, https://www.eia.gov/todayinenergy/detail.php?id=34272. to an average of 1.1 million barrels per day in 2017, reaching thirty-seven destinations that year.24“U.S. Crude Oil Exports Increased and Reached More Destinations in 2017,” Today in Energy, US Energy Information Administration, March 15, 2018, https://www.eia.gov/todayinenergy/detail.php?id=35352. In the first half of 2018, crude oil exports reached an average 1.8 million barrels per day.25“Crude Oil Was the Largest U.S. Petroleum Export in the First Half of 2018,” Today in Energy, US Energy Information Administration, September 24, 2018, https://www.eia.gov/todayinenergy/detail.php?id=37092. Going forward, the United States is projected to become a net energy exporter, thanks to these changes in oil and gas markets and domestic production.26“The United States Is Projected to Become a Net Energy Exporter in Most AEO2018 Cases,” Today in Energy, US Energy Information Administration, February 12, 2018, https://www.eia.gov/todayinenergy/detail.php?id=34912.

Technology and production trends

As shale producers continued to experiment and conduct trial and error in shale plays, technology and production techniques continued to evolve, and were replicated on a larger scale. Some of the noteworthy developments, which are ongoing, include drilling increasingly long laterals and “supersizing” wells; the development of movable or “walking” drill rigs; and the ability to drill multiple wells on a single well pad. These developments helped refine the ability to target resources and increase utilization rates and was undergirded by the previously noted culture of professionalism and expertise, which enabled an iterative experimentation and improvement process. These developments also led to declines in time spent on the drill site, which in turn reduce labor and equipment costs. Given these efficiencies, the rig count, long the barometer of productivity in the industry, is no longer the most reliable measure as more wells can be drilled from one rig and the productivity of those wells has increased.

Global market dynamics

Industry expert Tisha Schuller described the evolution and improvement of drilling technology as a “continuing march that really improves when the price either goes way up or way down.”27Tisha Schuller (author and principal of Adamantine Energy), in discussion with the author, October 2018. In that sense, broader oil market dynamics, namely the dramatic price decline which followed Saudi Arabia’s decision to push for market share in late 2014, actually drove the shale industry to become more creative and ultimately, some industry analysts argue, more competitive.

The lower price environment drove companies to cut costs, increase efficiency, and increase productivity per well. (It also drove some smaller players out of the market and led to consolidation.) In a high-price environment, shale producers could throw money at a problem or a supplier, while the low-price environment forced them to wring efficiencies out of the process. As a result, US shale producers adjusted exploration and extraction techniques to weather the turmoil of low oil prices and Saudi oil-market policies prior to the Vienna agreement.28OPEC and Non-OPEC producers agreed in December 2016 to cut crude oil production, effective in 2017. While there were bankruptcies and job losses, healthier companies emerged.29Clifford Kraus, “Oil Boom Gives the U.S. a New Edge in Energy and Diplomacy,” New York Times, January 28, 2018, https://www.nytimes.com/2018/01/28/business/energy-environment/oil-boom.html. As a Bloomberg article put it bluntly, “OPEC helped create the monster that haunts its sleep.”30Javier Blas, “Texas Is About to Create OPEC’s Worst Nightmare,” Bloomberg, November 21, 2018, https://www.bloomberg.com/news/articles/2018-11-21/opec-s-worst-nightmare-the-permian-is-about-to-pump-a-lot-more.

3. The rise of shale and its impacts

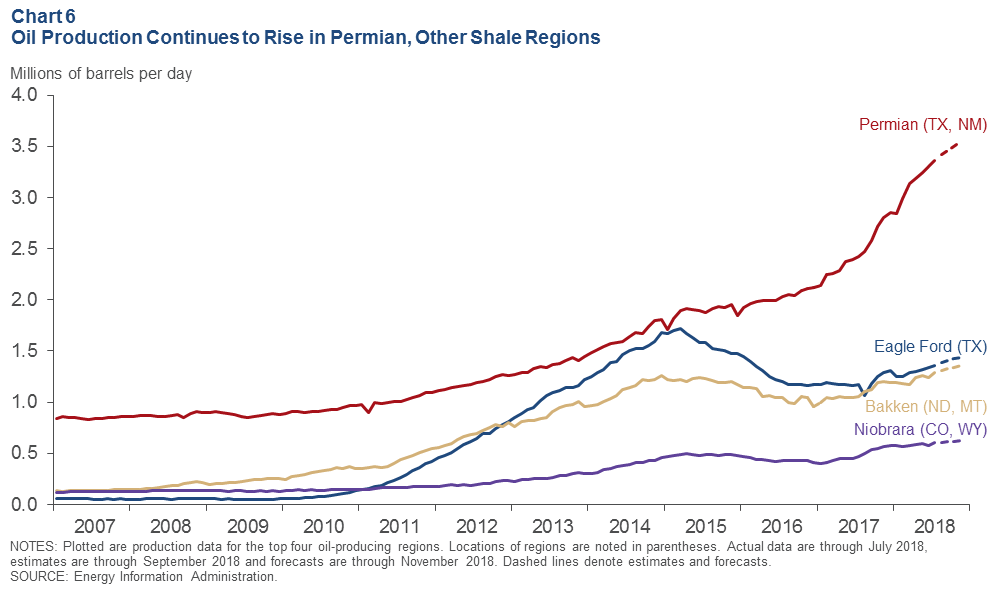

Prior to the rise of shale production, oil production in Texas peaked in 1972 when year-end production reached 1.26 billion barrels.31Texas Comptroller of Public Accounts, Biennial Revenue Estimates 2018-2019. In the decades that followed, total production plummeted to as low as 336 million barrels in 2007, before rising from 2008 on to reach nearly 1.03 billion barrels in 2017.32Texas Railroad Commission website, “Crude Oil Production and Well Counts (since 1935),” last accessed December 5, 2018, http://www.rrc.state.tx.us/oil-gas/research-and-statistics/production-data/historical-production-data/crude-oil-production-and-well-counts-since-1935/. This resurgence has been largely fueled by Permian output, which has increased 60 percent over the last two years.33Ed Crooks, “US Oil Producers Battle to Meet Iran Shortfall,” Financial Times, May 10, 2018, https://www.ft.com/content/fac73006-53c9-11e8-b3ee-41e0209208ec. Now, ten years in to this shift in US production, all eyes are on the Permian, where the Texas oil story took off with the Santa Rita discovery in the 1920s.34Jeffrey Ball and Benjamin Lowy, “Lone Star Rising,” Fortune, May 25, 2018, http://fortune.com/longform/permian-basin-oil-fortune-500/.

The Permian is currently the leader in the United States in oil production, the number two gas-producing play in the United States, and is the top location for infrastructure investment and capital expenditure investment.35RBN Energy LLC website, https://rbnenergy.com/products/permian-natgas/. Going forward, the US Energy Information Administration (US EIA) predicts Permian output will average 3.3 million barrels per day in 2018 and 3.9 million barrels per day in 2020.36“Permian Region Is Expected to Drive US Crude Oil Production Growth through 2018,” Today in Energy, US Energy Information Administration, August 23, 2018, https://www.eia.gov/todayinenergy/detail.php?id=36936. Other projections, including from the International Energy Agency (IEA), have suggested output could top 4 million barrels per day within the next two years, meaning the output of this single field would be on par with global producers and OPEC members like Iran and Iraq.37Alison Snider and Bradley Olson, “Is the U.S. Shale Boom Hitting a Bottleneck?” Wall Street Journal, April 18, 2018, https://www.wsj.com/articles/is-the-u-s-shale-boom-choking-on-growth-1524056400.

Implications of rise of US shale

Successful shale production has resulted in dramatic increases in both domestic oil and gas production, which in turn has had profound domestic implications and for global oil and gas markets. At home, the rise of domestic oil and gas production has lowered US consumer prices for energy, while in certain states the importance of the energy sector in the economy has either been maintained and underscored (Texas, Oklahoma), grown (Ohio, Pennsylvania), and even transformed the state economy (North Dakota). It has also resulted in a decrease in US crude oil imports, which have fallen dramatically over the last ten years, with net imports anticipated to fall to 320,000 barrels per day in December 2019, which would be the lowest total since 1949.38Blas, “Texas Is About to Create OPEC’s Worst Nightmare.” While crude oil imports are falling, and crude oil exports rising, the United States will likely continue to import crude as the domestic refining complex was set up to process heavier blends, imported from Canada, Venezuela, and elsewhere, rather than the light sweet crude produced in shale plays.

Implications for oil

The rise of US shale production has also impacted global oil and gas markets in profound ways. With respect to oil, rising US production led to a growing perception among some oil producing countries that they might be losing market share to new rivals. Thus, in November 2014, Saudi Arabia announced it would abandon its former policy of pursuing price in global markets, opting instead to compete for market share. This strategic shift, ostensibly aimed at flooding the market and dropping the price for oil in the hopes of driving US producers out of business, backfired as shale producers adapted and the breakeven price for some US shale producers proved lower than anticipated. While oil production from shale fell in the Bakken and Eagle Ford by the middle of 2015, Permian production continued to rise.39Kleinberg, Paltsev, Ebinger, Hobbs, and Boersma, “Tight Oil Market Dynamics.” As discussed in the previous section, the low-price environment had the unintended effect of forcing shale producers to cut costs and increase efficiency to survive, leading to a more resilient industry.

Given these dynamics and the pressure that the low-price environment placed on oil producing nations (particularly whose budgets are reliant on oil revenue), OPEC and eleven non-OPEC producers agreed in 2016 to curtail production by nearly 2 million barrels per day. By the spring of 2017 this agreement had resulted in production cuts of 1.73 million barrels per day, compared to the October 2016 level. As the price of oil crept up in 2017 and 2018 (albeit aided by geopolitical factors like the re-imposition of US sanctions on Iran), the success of the deal in reducing the global supply overhang was dampened by oil production from the United States. At the 2018 Abu Dhabi International Petroleum Conference (ADIPEC), Saudi Oil Minister Khalid Al-Falih announced Saudi Arabia planned to cut exports in December and called for output cuts from other producers, signaling an interest in keeping global inventories low.40“Saudi Arabia Calls for Oil Output Cuts,” CNN Business, November 12, 2018, https://www.cnn.com/videos/business/2018/11/12/saudi-arabia-oil-cuts.cnn-business. Saudi Arabia went further in calling for 1 million barrels per day in production cuts among the group of OPEC and non-OPEC producers. On December 6, OPEC and its oil-producing allies solidified their intention to continue limitations on production, agreeing to curb production by 1.2 million barrels per day.41Benoit Faucon, Summer Said, and Christopher Alessi, “OPEC, Russia Strike Deal to Cut Oil Production,” Wall Street Journal, December 7, 2018, https://www.wsj.com/articles/saudis-still-skeptical-of-opec-coalition-cuts-1544178705. The agreement was enabled by cooperation between Saudi Arabia and Russia, which are, along with the United States, the largest producers in the world.

Implications for gas

Oil markets are not the only place that shale producers have made their mark. Gas markets have also been upended by the shale revolution. While US gas exports via pipeline have increased since 2000, the commencement of US LNG exports in 2016 was a seminal event, turning the US into an LNG exporter and helping drive changes in global LNG markets. Projected growth in US LNG export capacity is anticipated to continue to drive the market, as the International Energy Agency predicts the United States will account for roughly 75 percent of new export capacity through 2023,42“The Gas Industry’s Future Looks Bright over Next Five Years, According to IEA Analysis,” International Energy Agency, June 26, 2018, https://www.iea.org/newsroom/news/2018/june/the-gas-industrys-future-looks-bright-over-next-five-years-according-to-iea-ana.html. and Bloomberg New Energy Finance predicts US LNG export capacity will double by 2030.43“Global LNG Outlook 2018,” Bloomberg New Energy Finance, https://about.bnef.com/lng-outlook/.

The impact of the United States as an LNG exporter is aided by the rise of China as a major gas importer, fuel switching in the power sector from coal to gas, and growth in industrial gas consumption, all of which are contributing to a changing global gas market. Due to these factors, the global LNG market is evolving from the traditional oil price-linked long-term contracts with take or pay clauses to gas-indexed contracts with flexible destination clauses. The market has also witnessed a rise in spot purchases, leading to a more flexible, liquid market for exporters and importers alike (even as this poses issues for project financing for new import facilities). For example, nearly 60 percent of US LNG was sold on a spot basis in 2017.

The rise of shale gas production has also transformed the US power sector, as the low price of natural gas resulted in a market-driven transition from coal to gas. This has also had a direct impact on US greenhouse gas emissions. Between 2007 and 2016, US carbon dioxide emissions dropped by 25 percent due to fuel switching from coal to cheaper natural gas in the power sector.44Daniel Raimi, The Shale Revolution and Climate Change, Resources for the Future, Issue Brief 18-01, January 2018. Increased US gas production led to a decrease in gas prices, and this combined with reduced costs for renewable energy has led to a shift in the power sector, a trend the US EIA projects will continue as coal’s share of total power generation declines and the share of natural gas increases.45The EIA projects that the natural gas share of electricity generation will rise from 32 percent in 2017 to 35 percent in 2018 and to 36 percent in 2019, while coal’s share in total electricity generation will average 28 percent in 2017 and fall to 26 percent in 2019, down from 30 percent in 2017. “2018 Short Term Energy Outlook,” US Energy Information Administration, November 2018, https://www.eia.gov/outlooks/steo/.

Implications for the industry

The rise of shale has also impacted the oil and gas industry itself. The production timeline of shale investment and production has changed industry time horizons and mindset. Many companies are shifting to short-cycle investment because the ability to ramp production up or down balances portfolios by enabling the industry to adjust production based on market conditions. This approach gives the industry the ability to be flexible, nimble, and responsive to market conditions, which is particularly attractive in an era of energy transition in which questions regarding the future of oil demand and peak demand are part of broader questions over the pace and nature of change in the energy system.

These characteristics differ dramatically from areas such as offshore production (where many firms were investing heavily prior to the ability to produce shale), which is more time and capital intensive. For example, Royal Dutch Shell PLC’s US business has stated explicitly that shale production serves as a balance for deepwater projects and helps give companies flexibility.46Anji Raval, “Shell Bets on Shale for Flexibility in Energy Transition,” Financial Times, October 18, 2018, https://www.ft.com/content/700e9ef4-d268-11e8-a9f2-7574db66bcd5?utm_source=dlvr.it&utm_medium=twitter&utm_campaign=newsletter_axiosgenerate&stream=top. As an article in Energy Economics put it, “Unlike deepwater and Arctic projects, for which lead times are typically a decade or more, a tight oil well can be planned, drilled, and completed in months.”47Kleinberg, Paltsev, Ebinger, Hobbs, and Boersma, “Tight Oil Market Dynamics.” As the article points out, the ability to add barrels to the market quickly, even in low price environments, also contributes to shale being a price maker, rather than a price taker, as is the case for longer term, more complex plays.48Ibid. Shale production can also serve as a hedge against political risk, given the shorter production time frames.

Production from shale has also shifted thinking from a focus on volumes to a focus on efficiency and improving overall performance rates. This has moved the industry to focus heavily on logistics, optimizing the supply chain, and infrastructure. As the Financial Times noted in a story about shale producers becoming financially sustainable, “many shale companies have been saying they will focus on improving returns rather than growth at all costs.”49Ed Crooks and Nicole Bullock, “US Shale Groups Reach Self-financing Milestone as Oil Prices Rise,” Financial Times, April 23, 2018, https://www.ft.com/content/ea3ff3a0-4639-11e8-8ee8-cae73aab7ccb. This means improving efficiency, capitalizing on scale, and potentially moving toward more of a manufacturing model of production, with shale producers focused on cheap and efficient barrels and return on investment and margins over absolute production volume. The goal has shifted from chasing the big well to raising overall productivity, driven by data analytics and technology.

As a profile on the field in Fortune put it: “Unlike in, say, deepwater basins off Africa or Asia, the goal in the Permian isn’t so much to find the oil, because the oil here in West Texas long ago was found. The goal here is more workmanlike: to assemble the acreage that contains the most oil and to execute the drilling and fracking plan that will pull it out at the lowest cost.”50Jeffrey Ball and Benjamin Lowy, “Lone Star Rising.” The average production per well in Texas bears this out. As the combination of horizontal drilling and hydraulic fracturing started to change the industry, average production per oil well in Texas stood at 6.07 barrels per day in 2008 and more than doubled to 15.03 by 2017.51Texas Railroad Commission, Crude Oil Production and Well Counts (Since 1935), http://www.rrc.state.tx.us/oil-gas/research-and-statistics/production-data/historical-production-data/crude-oil-production-and-well-counts-since-1935/.

Another major shift is underway from the independents to the oil majors. While the independents were responsible for the breakthrough in shale and the early days of production, more IOCs have entered the game, particularly after the post-2014 low-price environment made it difficult for some independents to survive. This has signaled another shift, as IOCs are able to bring economies of scale and experience not just in upstream, but also in midstream and downstream assets and experiences to bear, suggesting that shale producers are moving more toward a manufacturing model as bigger companies look to utilize scale and drive efficiency.

4. Looking forward: progress made but challenges remain

While oil and gas production continue to rise and producers harness more improvements in technology and efficiency, the industry still has obstacles to overcome. Challenges remain, particularly when it comes to the difficulties of drilling near communities, managing the strain on infrastructure, and operating in an increasingly climate-conscious world. Interestingly, many of these challenges are not necessarily industry specific, but rather related to the operational challenges of being in an urban environment and managing demand for services and stressed capacity. These challenges relate to broader public-policy challenges such as infrastructure investment and maintenance, education funding, and housing prices, along with issues such as demand for labor, services, and key supplies.

While there are challenges to operating in a highly urban and population dense environment as in the Barnett Shale, there are also challenges to operating in more rural areas, or in smaller urban environments less equipped to handle the increase in activity across multiple supporting sectors. For instance, in the Permian, producers are finding it difficult to recruit and maintain the workforce they need. According to the Chamber of Commerce in Midland, the heart of the Permian, at least 15,000 jobs remain open at any given time, and many jobs remain vacant for months before being filled.52Jordan Blum, “Companies, Needing Permian Workers, Find West Texas a Hard Sell,” Houston Chronicle, June 1, 2018, https://www.houstonchronicle.com/business/energy/article/Companies-needing-Permian-workers-find-West-12960385.php. Workforce will also likely remain a challenge in the future, even as technology evolves and automation advances, which will raise questions as to how to transition from a relatively low-tech to high-tech industry when it comes to workforce development.

Roads in traditionally rural areas are facing issues of wear and tear from industry traffic, particularly heavy sand and water trucks and semitrucks carrying pipes and supplies, as well as overcapacity, traffic, and congestion. These combined issues have resulted in a stretch of highway from Carlsbad to Pecos in West Texas being dubbed the “Death Highway.” Similarly, schools are filled beyond capacity as the Midland metro area population has grown by more than 20 percent since 2010, making Midland the country’s hottest housing market.53Cicely Wedgeworth, “The Hottest Markets in June 2018: What Happens When They Get Too Hot?” Realtor.com, July 5, 2018, https://www.realtor.com/news/trends/hottest-markets-june-2018/. This is an unusual distinction for a city located in the middle of a fairly rural part of Texas, and one that makes it difficult to recruit teachers, nurses, and other essential workers.

To address these issues in the Permian, a group of producers has joined together to form the Permian Strategic Partnership, intended to create a cooperative model between industry and the local community to grapple with some of these issues and provide financial support through public-private partnerships. These issues include roads, public education, workforce development, healthcare, and housing, and this model of industry partnering with local and city governments and providing funding through a public-private partnership model could prove a useful example of how the industry might look to solve challenges related to the impact it has on local communities.

As the area’s infrastructure is stretched thin, increasingly so are the service companies and equipment suppliers, leading to rising costs and impacting availability of labor, proppant supplies, water and water services, and equipment rentals. Infrastructure needed to move crude to market and to capture and move associated gas is also increasingly constrained in the Permian, an issue which largely impacts smaller companies that lack their own midstream assets or the balance sheet or scale to book capacity well in advance. However, pipeline constraints are largely expected to be ameliorated by late 2019 or 2020 at latest.

The Permian is facing gas takeaway capacity constraints as associated gas production has made the field the second-largest gas-producing play in the United States. While gas pipelines reached near capacity in 2018, a proposed 14 bcf/day in additional capacity should help alleviate these constraints over the next four years.54Eklavya Gupte, “Analysis: Permian Basin Gas Constraints on Track to Ease in 2019,” S&P Global Platts, October 19, 2018, https://www.spglobal.com/platts/en/market-insights/latest-news/natural-gas/101918-analysis-permian-basin-gas-constraints-on-track-to-ease-in-2019. Anticipated pipelines include the Gulf Coast Express project, expected to enter into service in fall 2019, the Permian Highway Pipeline, the Pecos Trail Pipeline, and the North Texas Expansion line.

Crude oil pipeline takeaway capacity is also anticipated to improve over the course of 2019 to 2020, and a 2018 third-quarter survey by the Federal Reserve Bank of Dallas suggests this will be resolved by the fourth quarter of 2019 (although some respondents anticipate the issue will not be fully resolved until 2020).55Federal Reserve Bank of Dallas, Dallas Fed Energy Survey, Third Quarter, October 1, 2018, https://www.dallasfed.org/research/surveys/des/2018/1803.aspx#. Crude pipelines expected to come online in 2019 include the Cactus II, Enterprise, EPIC, and Gray Oak, while in 2020 potential pipelines include the Permian-Gulf Coast, Jupiter, and the Lotus Midstream, ExxonMobil, and Plains All American Pipeline Joint Venture.56Blas, “Texas Is About to Create OPEC’s Worst Nightmare. Many anticipate this will lead to a bump in Permian production in late 2019 as many of the drilled but uncompleted wells are completed and brought online as infrastructure constraints ease.

Other infrastructure constraints or existing challenges include the ability to handle the giant tanker ships, called Very Large Crude Carriers (VLCCs) (2 million barrels), used to transport crude to Asia and Europe, and there is need for a more efficient way to ship crude out of the Gulf. Currently, the only place in the United States these ships can load in port is Louisiana Offshore Oil Port. At other US ports, smaller ships are used for costly ship-to-ship transfers to load the crude onto the VLCCs, at a cost of between $750,000 and $1 million per loading.57Rebecca Elliot, “Frackers Bet on New Terminals to Boost Oil Exports,” Wall Street Journal, October 21, 2018, https://www.wsj.com/articles/frackers-bet-on-new-terminals-to-boost-oil-exports-1540119600?utm_source=newsletter&utm_medium=email&utm_campaign=newsletter_axiosgenerate&stream=top.

Perhaps a longer-term challenge facing shale production, even as it finds itself in the spotlight, is how to respond to or address climate change, an issue that is before the oil and gas industry more broadly. The prominence of climate change as an issue and the way in which the oil and gas industry reacts will likely be a focal point in the broader conversation about energy transition. Currently the US case provides evidence that shale gas can play a positive role in reducing greenhouse gas emissions, part of a larger global narrative about whether and how natural gas can serve as a fuel of choice in the energy transition.

However, this narrative is not yet fully decided, and the way the industry grapples with existing issues related to methane could have an outsized impact on public perception. While methane is not the only issue, it may well serve as a litmus test for how the industry responds to questions over emissions reductions and the broader set of challenges related to climate change. Failing to acknowledge these issues, and more specifically operating without a methane capture program could leave the industry open to criticism. Given the reality of climate change as part of the public discourse, the industry would benefit from being (and being seen as) proactive rather than reactive. As one industry expert put it, “Methane is what health and safety was twenty years ago.”58Schuller, in discussion with the author.

The September 2018 pledge announced by the Oil and Gas Climate Initiative, an industry-led group focused on reducing the energy value chain carbon footprint, accelerating low carbon solutions, and enabling a circular carbon model, to reduce the methane intensity of operations was one positive step in this direction.

The prominence of climate change as an issue and the way in which the oil and gas industry reacts will likely be a focal point in the broader conversation about the energy transition.

While methane may prove a current flashpoint, there are several other ways the climate challenge may manifest itself, including divestiture movements, shareholder initiatives, and the appeal of a rising narrative surrounding technology and renewables whereby new energy sources are seen as the solution to “old” ones.

5. Conclusions and lessons learned

As other countries look to capitalize on their shale resource potential, the US case provides useful enabling characteristics and lessons learned. While each shale play comes with its own unique characteristics, each oil and gas company with its own methods and expertise, and each country with its own laws, regulations, and fiscal environments, there is value in drawing lessons from what happened in the United States, particularly in Texas. Few areas in the world have a comparably long history with drilling, making it a useful base case but also a unique one, as it does not necessarily have the same public sentiment that has driven fracking bans in places like France and Germany.

1. Geology still matters.

The US case demonstrates one obvious point: geology remains important. While the geology of US shale plays has been proven to be “there,” this is not necessarily the case in other areas identified as having shale resource potential. In China the geology has proven much more complex (and perhaps unfavorable) than anticipated, while in Poland excitement gave way to disappointment as exploration did not yield the hoped-for results. It is only when the geology is certain that exploration risks subside, production can be relied on, and efficiencies are maximized.

2. US case illustrates challenges of both rural and urban environments.

Another lesson is that both rural and urban areas come with their own set of unique production challenges. Drilling near urban environments requires more targeted public outreach, engagement, relationship building, and education. In rural areas, while the urban interface might not be a problem, there may be challenges related to overwhelming more limited infrastructure given the remote location. Texas experienced shale production in urban areas like the Barnett as well as rural areas like the Permian. In the Barnett, shale issues of proximity to homes, schools, and communities meant grappling with the associated issues of noise and nuisance and setback distance. The boom in the Permian, in contrast, overwhelmed the infrastructure (roads, schools, and available housing) of a more rural area, forcing companies to grapple with broader public-policy problems and community services and relations.

3. The US enabling ecosystem provides a unique advantage.

A further key lesson is the importance of the enabling ecosystem of labor, services, equipment, and infrastructure, including ports. Absent the history and concentration of production found between Texas, Oklahoma, and Louisiana and the assets both bring, producers in other nations may need to build up from scratch. While not impossible, it is simply to suggest that hoping for the breakeven numbers and efficiencies achieved by US shale producers is likely unreasonable for shale producers elsewhere. That said, many countries hoping to capitalize on domestic shale resources may enjoy the benefits of well-financed state-owned companies (or at least state-owned companies whose motives and purpose extend beyond turning a profit). They may also benefit from lower labor costs depending on the country and the market, although this raises questions of whether the local labor force includes the skills needed for the industry in the same way as in the United States.

4. Scale and size make factory model increasingly attractive.

Additionally, larger IOCs are pursuing the development of a “factory model” of shale production, looking to capitalize on economies of scale and big balance sheets and to streamline and transfer expertise and resources across their portfolio. For countries hoping to develop shale resources, looking to IOCs with the ability to bring these resources and expertise to bear would seem to be the most successful option, even as those companies still might struggle with limitations related to infrastructure or skilled labor in various countries. Conversely, while well-financed national oil companies (NOCs) might lack the technical know-how or experience with shale production, they similarly could bring substantial financial resources, economy of scale, and a more factory-like approach to shale production.

There is evidence of this in the United States, as bigger companies like ExxonMobil and Chevron Corp. have taken the lead in a fracking field they were late to enter. As Chevron’s president of North America exploration and production, Jeff Shellebarger, put it, “You need scale once you’re in development mode to be able to succeed at the margins that you have.”59Bradley Olson and Rebecca Elliot, “Oil Giants Start to Dominate U.S. Shale Boom,” Wall Street Journal, November 15, 2018, https://www.wsj.com/articles/oil-giants-start-to-dominate-u-s-shale-boom-1542286801 Scale helps drive down costs, maximize efficiencies, and negotiate for better contracts, including for pipeline capacity (or own their own midstream assets).

5. Stable policy environment is a crucial baseline condition.

Ultimately the US case shows that perhaps the most critical element to the development of shale resources is the presence of a stable and consistent policy environment. Beyond that, in the absence of a well-developed industry, including an ecosystem of suppliers, service companies, infrastructure, and qualified labor as well as easy access to capital, shale production in some countries will likely take some time as the starting point is dramatically different than that which previously existed in Texas. In instances in which seasoned US companies and IOCs are willing to undertake shale development, or where state-owned companies take a longer-term approach less bound by profitability, shale development will likely occur elsewhere. While it might be improbable that shale production elsewhere will amount to a “revolution” or have outsized market impact to the degree the United States experience has, the US case provides an understanding of key conditions that enable the swift rise of shale production for other countries to consider.

Image: Horizontal drilling rigs like this one owned by Parsley Energy near Midland, Texas dot the landscape in the Permian. CREDIT: REUTERS/Nick Oxford