The 2014 oil price collapse sent shockwaves across the oil industry and put economies from North Dakota to Nigeria on notice that $100 oil is not a sure thing. The economy of Texas, however, fared far better during the years of low prices than many experienced oil watchers predicted. Its relative resilience, explained in part by a recent paper from the Dallas Fed, provides a good lesson for countries, like Saudi Arabia and the UAE, working on ambitious diversification plans to better weather the regular downturns in commodities markets and prepare for a future in which oil demand is uncertain. Unfortunately, the paper also suggests just how challenging real diversification for these countries will be.

By 2014, the US shale boom was in full force and Texas was one of its epicenters, accounting for sixty percent of new US reserves and nearly forty percent of total US production. Oil’s percentage of the state economy was only slightly smaller in 2014 as compared to 1986, when an oil price drop sent the Texas economy into a tailspin. As the price collapse of the second half 2014 started to sink in, some economists predicted the worst. In December 2014, JPMorgan Chief Economist Michael Feroli argued, “We think Texas will, at the least, have a rough 2015 ahead, and is at risk of slipping into a regional recession.”

But even with oil prices dipping as low as $27 by February 2016, 1986 did not repeat itself. While the Texas oil and gas industry contracted and GDP growth slowed, the Texas economy did not go into recession.

The Dallas Fed explains: “Although the upstream oil and gas sector became more closely linked with other sectors of the Texas economy in the 2000s, it is less central to the Texas economy today than it was during energy’s previous heyday. Instead, service-providing industries—particularly financial and business services—have achieved outsized contributions to overall connectedness across the economy.”

The somewhat vague concept of “connectedness”—how much changes in one sector of the economy impact other sectors—is crucial to understanding how an oil price drop will impact an economy. Jamie Dimon summarized the connectedness of the 1986 Texas oil industry in JPMorgan’s 2014 annual report: “ … when oil collapsed in the late 1980s … Texas banks went bankrupt because of their direct exposure to oil companies and also because of their exposure to real estate whose value depended largely on the success of the oil business.”

In 2014, the financial and business services sectors in Texas were no longer primarily serving oil and gas companies. Their clients also included technology firms, defense contractors, a large renewable energy business, a major national grocery chain, and a much larger downstream oil sector, which provided a hedge against low crude prices. While some of these firms were impacted by a downturn in the local economy caused by oil job losses, as multinational companies operating in a growing global economy they were better prepared to weather a downturn in their home market. Many even benefited from a drop in fuel prices.

This suggests that the percentage of non-oil activity in an economy is only part of the diversification story. For diversification to be successful, the non-oil economy must be de-linked from the oil economy to include stand-alone economic activities. For example, a law firm or airline whose primary clients are the oil industry will be much harder hit by an oil price collapse than one that has a diverse client base with non-oil revenue.

This seems fairly obvious, but when conversations about economic diversification are often comparisons between oil and non-oil GDP, it is easy to miss this broader point about the relationship between the oil and non-oil sectors.

8,000 miles away, Christof Ruhl, global head of research at the Abu Dhabi Investment Authority, alluded to the issue of “connectedness” of the oil and non-oil economies of Gulf Cooperation Council (GCC) countries at the recent Atlantic Council Global Energy Forum in Abu Dhabi:

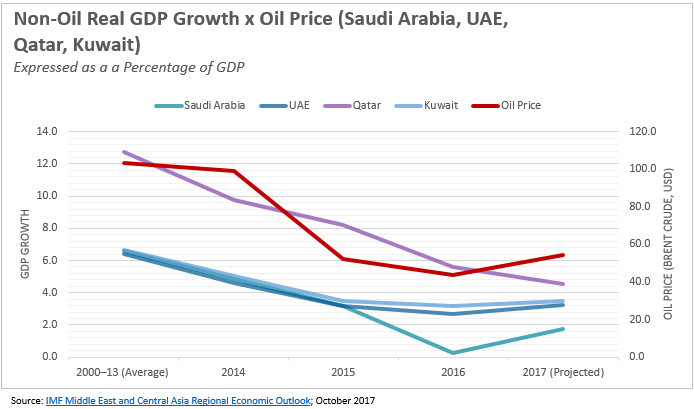

“While it looks as if the share of non-oil of GDP … is steadily rising … there is a puzzling sign here, which is that when you take the growth of non-oil GDP for the GCC year after year and you overlay it with the oil price … you get a relationship of one to one. Every single year the oil price goes up, growth of the non-oil sector increases. Every single year the oil price goes down, growth of the non-oil sector decreases.”

While some GCC countries happily report how much of their economy comes from non-oil activities, Ruhl’s research suggests that the “connectedness” of the GCC’s oil and gas sector to the rest of the economy is still high.

This is where it gets challenging: it is far easier to build hotels, restaurants, retail, a financial sector, etc, that rely on the oil business than to grow new standalone sectors. Texas was successful in doing so for a range of reasons including favorable demographics, relatively low real estate prices, a strong university system that created a well-educated labor pool (including a number of tech entrepreneurs), and government efforts to attract businesses and build industry clusters. The applicability of these factors within the GCC varies from country to country, and each would be wise to consider which are pertinent given their individual circumstances.

The broader lesson is that diversification of the economy cannot be measured by comparing oil to non-oil GDP alone. Instead, countries need to examine how connected their oil economy is to the rest of their economic activities and work to develop sectors that will thrive independently of whether oil is at $20, $60, or $100 per barrel.

Put in more practical terms, efforts to attract tech talent and build innovation hubs; the expansion of the petrochemical sector (which has different demand drivers than crude); and the development of the renewable energy industry are likely moves in the right direction. But if Saudi Arabia’s planned resorts on the Red Sea coast don’t become destinations in their own right instead of just convenient afterthoughts for oil executives adding a holiday on to a trip to the Gulf, the GCC will continue the cycle Ruhl describes while Texas continues its march onward.

Randy Bell is managing director of the Atlantic Council Global Energy Center.