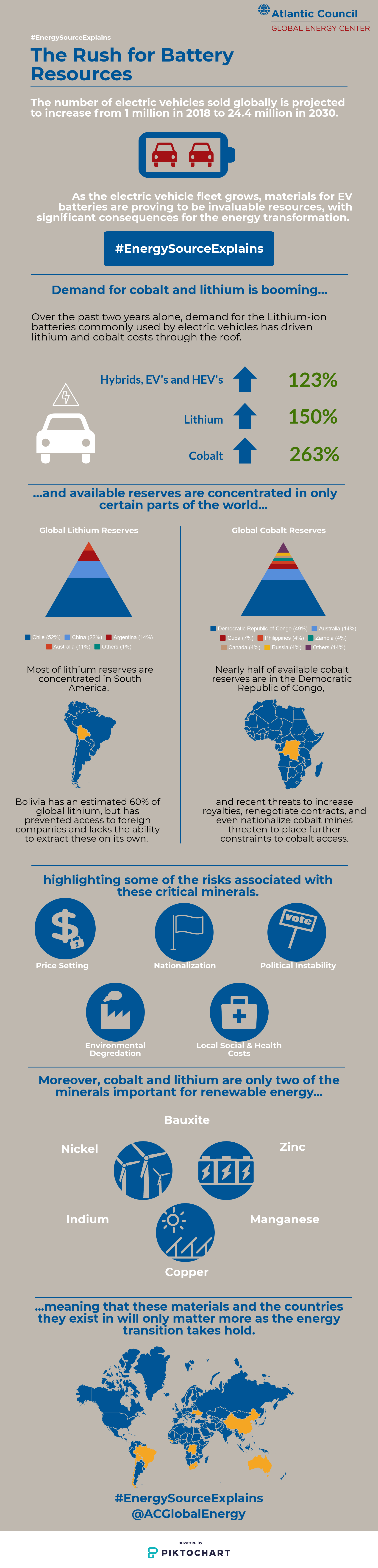

The transition to electric vehicles (EVs) is already underway, and its pace is expected to increase in the coming years. The number of EVs on the road worldwide is projected to grow from one million this year to 24.4 million by 2030.

Such growth in the EV fleet will require a significant expansion of battery production, specifically of Lithium-ion batteries. Although several types of Lithium-ion batteries can be used in EVs, they all contain lithium, cobalt, and nickel, metals which can carry significant supply and price risks.

The nickel market will be affected by the EV boom, but far less so than lithium and cobalt, since the existing market is larger and EVs will claim a much smaller portion of the future market.

Lithium and cobalt supplies are more likely to pose problems for future EV demand. One reason is that, despite a greater margin for meeting demand, the price of lithium has more than doubled, rising from $6,000 to $15,000 per metric ton in the last two years. Similarly, cobalt has nearly quadrupled in price between 2016 and 2018, increasing from $22,000 to almost $80,000 per metric ton.

The risks of inadequate lithium and cobalt supplies also go beyond high prices. Reserves of both are geographically concentrated in countries that could pose problems for supply chains. This problem is less serious for lithium, since Chile and Argentina hold around two-thirds of world reserves. Lithium resources that nearly match Chile and Argentina’s reserves can also be found in Bolivia, although President Evo Morales has severely stunted lithium production by preventing the entry of technologically-advanced foreign companies.

Inadequate supplies of cobalt pose a much more serious risk because about half of the world’s current production and reserves are found in the conflict-prone Democratic Republic of Congo. Recently, the Congolese parliament even passed a bill that could raise royalties on cobalt from 2 percent to 10 percent and the state-owned mining company announced it would renegotiate all foreign contracts in the next year and consider nationalization.

Yet, measures can be taken to mitigate these risks. Advances have already been made to reduce the share of cobalt needed in Lithium-ion batteries, and with 95 percent of Lithium-ion batteries currently being dumped in landfills, recycling recovery could ease the risks of extraction and development. Finally, general advances in battery technology have and will continue to make Lithium-ion batteries longer-lasting, faster-charging, and safer to use.

Looking beyond EVs, the supply risks of metals related to energy generation and storage also apply to many other areas of advanced energy. Wind, solar, and smart grid technologies all require specialized metals, including bauxite, manganese, and neodymium. As the energy transformation continues, we must be cognizant that these supply risks may become a fact of life, just like current concerns about oil.

Reed Blakemore is an associate director and Jens Jessen is an intern at the Atlantic Council Global Energy Center. You can follow Reed on Twitter @reed_blakemore