") US stocks saw another volatile day on February 6 as ripples spread to global markets.

US stocks saw another volatile day on February 6 as ripples spread to global markets.

The Dow Jones industrial average dropped more than 4 percent—a nearly 1,200-point decline—on February 5. The declines for the S&P 500 index and the Dow Jones Industrial Average were the biggest single-day percentage drops since August 2011. The Dow closed 567 points higher on February 6.

The market’s troubles unfolded even as the US economy has continued to strengthen with low unemployment, higher wages, and greater consumer spending. [A Labor Department report on February 2 found that the US economy added 200,000 jobs in January and wages grew at the fastest pace since 2009.] If the economy gets overheated, however, it could trigger inflation, which could force the Federal Reserve to raise interest rates sooner rather than later.

Bart Oosterveld, the C. Boyden Gray fellow on Global Finance and Growth and the director of the Global Business and Economics Program at the Atlantic Council, discussed the situation in an interview with the New Atlanticist’s Ashish Kumar Sen. Here are excerpts from our interview.

Q: Is this a long-overdue reality check?

Oosterveld: It is a correction that was bound to happen. It had been hard to understand what was driving the very significant increases in stock markets everywhere as exemplified by the Dow and S&P indices. They seemed disconnected from economic reality. The sharp continued rise was what was surprising in recent years, and especially in the past year. So, the correction in that sense is not surprising.

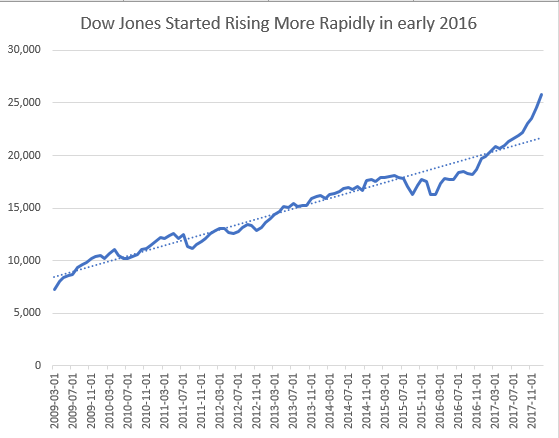

Q: Where do you see this settling?

Oosterveld: In the weeks ahead, the market will be volatile, much more volatile than it has been over the past few years. That means that there will be days when it will be sharply back up as well. The Dow started rapidly rising in early 2016—had it instead continued along its post-crisis trendline, it would be around 21,000 now.

Q: Meanwhile, the economy is booming—job growth is strong, wages have increased, consumer spending is up. Is too much good news bad for the market?

Oosterveld: It is true that the economy is doing well. The economy was nearing full employment when the current [US] administration took office. The risk that the economy might overheat has been present for some time. None of the things that you hear about—the risk of rising interest rates or the like—are new or surprising. Those have been around and well-signaled for some time.

Q: Should investors be worried?

Oosterveld: This is worrisome for people who have invested in equity markets to save for retirement or college education. It is too early to tell whether big investors like pension funds or people with significant equity holdings need to worry long term.

The fundamental underlying economic issue is that at some point the business cycle needs to turn, since we have enjoyed such a prolonged recovery.

Q: In previous instances, the Federal Reserve (Fed) has reacted aggressively to similar situations by raising interest rates? Is that prudent? How should the Fed respond?

Oosterveld: The Fed has been very careful to signal exactly what it was going to do at any point in time since the crisis and before. To the extent that it intervenes, the signaling of the intervention is what is important.

Ashish Kumar Sen is deputy director of communications at the Atlantic Council. Follow him on Twitter @AshishSen.

Image: A trader worked on the floor of the New York Stock Exchange in New York on February 6 as US stocks saw a second volatile day. (Reuters/Brendan Mcdermid)