Last week, the new vice chair of the US Federal Reserve, Lael Brainard, testified before Congress that the United States was at risk of falling behind in the race for the future of money. Judging by the number of countries that have embraced fiat-based digital assets, she’s right.

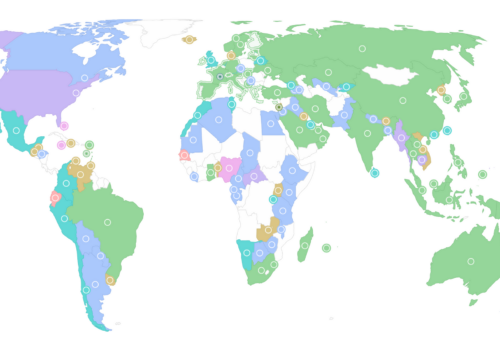

Two years ago, when the Atlantic Council’s GeoEconomics Center began our Central Bank Digital Currency tracker project, we highlighted thirty-five countries that were on their way to developing their government’s version of a stablecoin. Today, we’re releasing a major update, which now shows that 105 countries have jumped on the idea.

Here, we take you inside our new research and highlight the six key takeaways—and what they’ll mean for your wallet in the years ahead.

1. 105 countries, representing more than 95 percent of global GDP, are now exploring a CBDC. In May 2020, only thirty-five countries were considering a CBDC. Fifty countries are now in an advanced phase of exploration (development, pilot, or launch).

It’s not just that three times more countries are exploring CBDCs now than when we started our work—it’s that about half of them are serious about delivering a CBDC to their citizens. Our latest report shows that countries ranging from India to Ukraine to Brazil are all moving forward quickly. As part of our work, we convene a working group of fintech leaders from central banks every six weeks to discuss their progress. The overarching message we hear from all of them: They’re eager to see a US digital currency model—one that protects privacy and ensures cybersecurity—but their countries will press ahead with or without US guidance. We may not like what they come up with.

2. Ten countries have fully launched a digital currency, with China’s pilot set to expand in 2023. Jamaica is the latest country to launch a CBDC, the JAM-DEX. Nigeria, Africa’s largest economy, launched its CBDC in October 2021.

The list of countries with a fully launched (available to every citizen) CBDC is growing. What motivates these countries? Our research shows there are two main drivers. The first is cryptocurrency: The rise and fall of not-so-stable algorithmic stablecoins such as TerraUSD, as well as full cryptocurrencies such as Bitcoin, have made central banks worry about financial stability in their own economies. The second is the pandemic: In the two years since we started this project, the world has unleashed an unprecedented amount of fiscal and monetary stimulus. Governments and central banks realized they needed a faster and safer way to get money in people’s hands. It turns out CBDCs might be the answer.

3. Many countries are exploring alternative international payment systems. The trend is likely to accelerate following financial sanctions on Russia. There are nine cross-border wholesale (bank-to-bank) CBDC tests and three cross-border retail projects.

Retail CBDCs (meaning currency you can use to buy, for example, a cup of coffee) get most of the headlines. But some of the most interesting developments have come in the wholesale space, where banks transfer money between one another. Why does that matter? Consider this: If you’re a bank in China, watching Russia being cut off from the international financial system, you might want a backup plan. A cross-country CBDC system could be the solution, avoiding any need for the SWIFT system. Our data show new projects popping up all over the world, not only between China, Thailand, and the United Arab Emirates but also between South Africa, Australia, and Malaysia. Expect more of these throughout 2022.

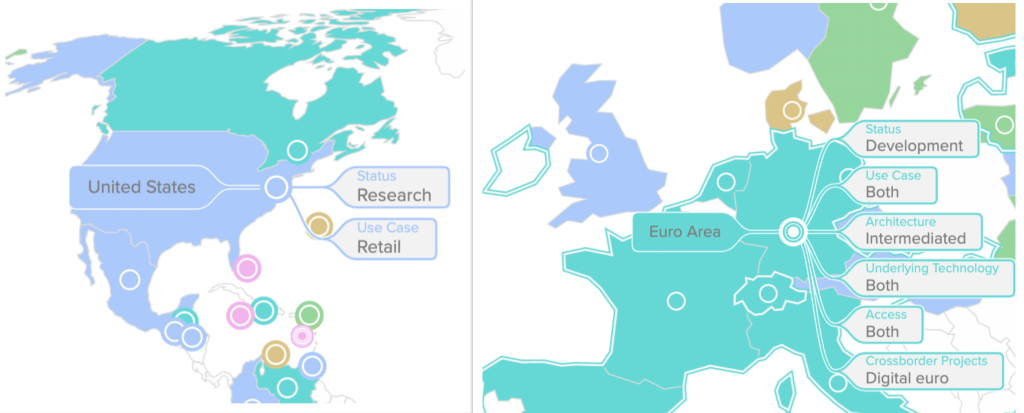

4. Of the Group of Seven (G7) economies, the United States and United Kingdom are the furthest behind on CBDC development. The European Central Bank (ECB), meanwhile, has signaled that it will deliver a digital euro by the middle of the decade.

The old guard of the global currency game—the pound and the dollar—are moving slowly, and a relatively new kid on the block, the euro, is moving forward the fastest. We now expect a digital euro to be widely available within the next few years, a change from our most recent update in December 2021. And the Federal Reserve has noticed: Brainard referenced the ECB’s progress multiple times in her testimony. In fact, she mentioned it even more than China.

5. Nineteen of the Group of Twenty (G20) countries are exploring a CBDC, with sixteen already in the development or pilot stage. This includes South Korea, Japan, India, and Russia, each of which has made significant progress over the past six months.

Central banks are cautious institutions by design, so when they decide to pursue a pilot project, there’s a good chance a fully launched digital currency will follow. China’s e-CNY project is the largest pilot with hundreds of millions of users. In February, we spoke to project leader Mu Changchun, who explained how they use distributed-ledger technology and create digital wallets with different tiers. But it’s not all about China: Other major economies are making rapid progress, too. Of the G20, only the United States, United Kingdom, and Mexico are still in the research stage.

6. The financial system may face a significant interoperability problem in the near future. The proliferation of different CBDC models is creating new urgency for international standard setting.

The White House has taken notice of the problem with a recent executive order calling for digital assets with democratic values. But what does that mean in practice? A digital currency that protects users’ privacy, is safe from cyberattacks, and helps bring more people into the financial system. The problem, however, is that the world is moving fast and the United States needs to be at the table to help ensure that the wrong kind of CBDC—one that is used to surveil citizens—doesn’t proliferate across the global economy. Otherwise, we’ll be facing a fractured global financial system with the strength of the dollar slowly eroded.

There’s more to find as you explore the tracker—from the corporate partners countries are working with, to the types of back-end technology central banks are using, to how you might actually use digital currencies on your phone.

The bottom line is that the race for the future of money is well underway but it’s not too late for the United States to catch up. If the United States can harness new technology to deliver faster and safer payments, the entire world will be paying attention.

Ananya Kumar is the assistant director of digital currencies at the Atlantic Council’s GeoEconomics Center.

Josh Lipsky is the senior director of the GeoEconomics Center.

Further reading

Mon, Apr 4, 2022

Can crypto deliver aid amid war? Ukraine holds the answer.

New Atlanticist By Ananya Kumar, Nikhil Raghuveera

Ukraine’s current experience could transform how aid is disbursed across the world.

Fri, Mar 11, 2022

What does Biden’s executive order on crypto actually mean? We gave it a close read.

Markup By

What signals does this order send about the Biden administration’s approach to cryptocurrency as well as a potential central bank digital currency?

Tue, Mar 1, 2022

A Report Card on China’s Central Bank Digital Currency: the e-CNY

Econographics By Ananya Kumar

China's CBDC, the e-CNY debuted at the world stage during the Olympic Games. Here's what we know so far.

Image: A sign indicating digital yuan, also referred to as e-CNY, is pictured at a shopping mall in Shanghai, China on May 5, 2021. Photo by Aly Song/Reuters.