With the snapback of significant US sanctions against Iran fast approaching on November 5th, speculation is mounting over how the Trump Administration will enforce the sanctions, and how its European allies might attempt to bypass them. The previous EconoGraphic outlined how a Special Purpose Vehicle (SPV) may facilitate trade between European small and medium-sized enterprises (SMEs) and Iran after US sanctions go back into effect. This edition of the EconoGraphic provides a primer on the Society for Worldwide Interbank Financial Telecommunication (SWIFT) and explains why sanctioning the financial messaging service would likely cause more harm than good.

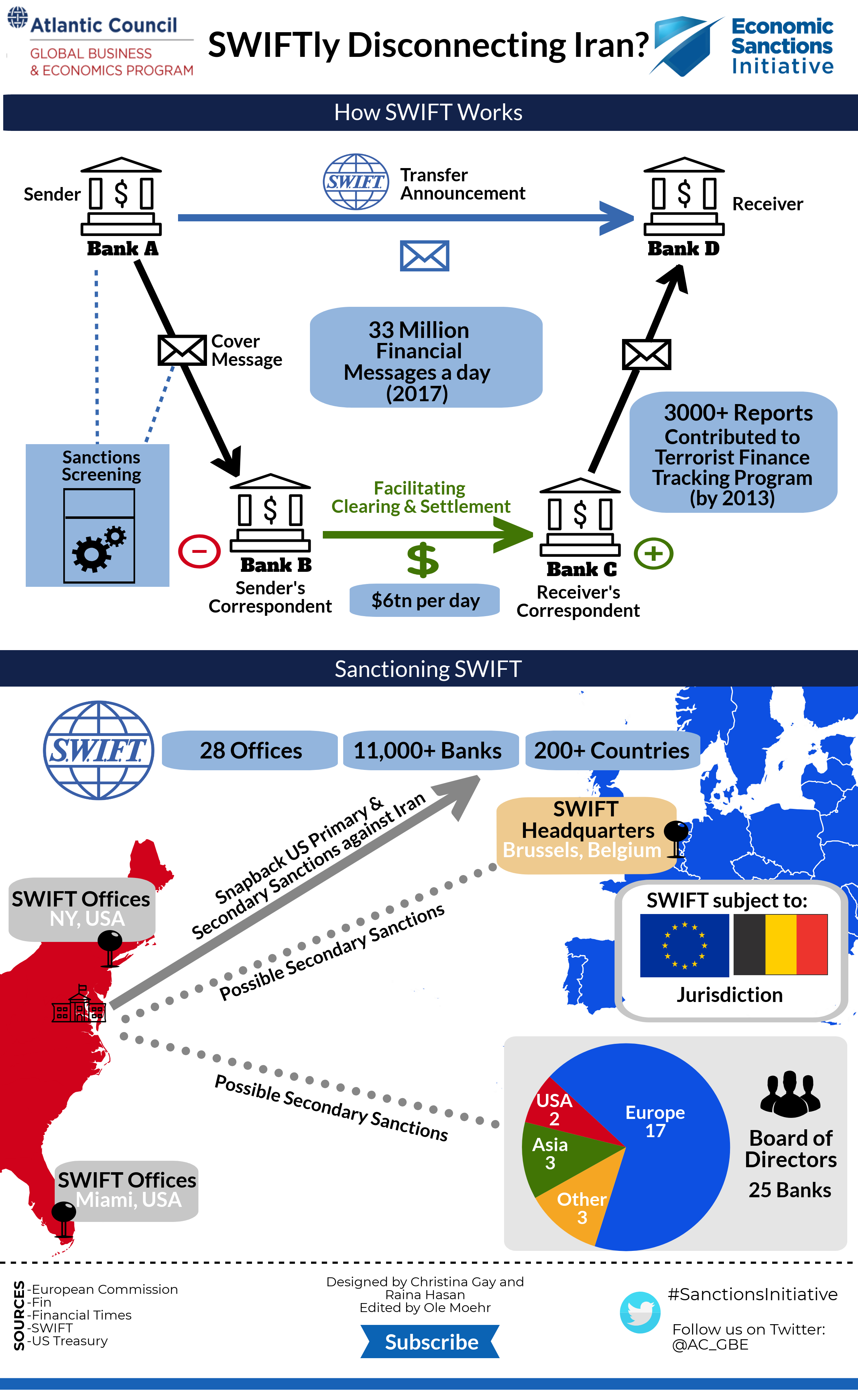

SWIFT is the most widely used electronic payment messaging system in the world. Financial institutions rely on SWIFT to move money across borders. It is important to note that SWIFT only facilitates the exchanges of money in the international financial system, it does not execute the transfer of funds between banks or other financial intermediaries. Simply put, SWIFT never touches money. Our graphic shows SWIFT’s “cover method”, which is European banks’ preferred way to move funds (US banks usually use the “serial method”). The sender institution facilitates the transfer of funds by dispatching two messages. The transfer announcement message notifies the receiver institution, which holds the beneficiary’s account, that funds are on their way and specifies the receiver’s correspondent bank, whose account will be credited. Since sender and receiver usually do not own bank branches in the same country, the transaction usually flows through correspondent banks, which are in the same country or monetary zone, to facilitate the payment. The cover message initiates the transfer of funds by instructing the sender’s correspondent (Bank B) to debit the sender’s account and credit the specified amount to the receiver’s account at its correspondent bank (Bank C).

The Trump Administration is reportedly considering several policy options, including sanctioning SWIFT itself, its member banks, and/or the organization’s officials, to compel SWIFT to disconnect Iranian banks from its network. In theory, the US Treasury could cut-off a European commercial bank that is a member of SWIFT’s board of directors, such as BNP Paribas, from the American financial system. A more likely scenario would see Washington target specific directors on SWIFT’s board by freezing their US assets and banning travel to the United States. According to our assessment, however, sanctioning SWIFT would likely result in economic costs and national security risks that outweigh the sanctions’ potential benefits for the US government. As our visiting senior fellow, Samantha Sultoon, explains in her recent piece, sanctioning SWIFT “risks hampering the flow of global financial transactions and trade, harming [US, EU, and other allies’] businesses.” In addition, sanctions against European banks or individuals could undermine transatlantic cooperation on the Terrorist Finance Tracking Program that is informed by SWIFT data. Finally, the US primary and secondary sanctions against Iran that go into effect on November 5th already provide ample deterrence to ensure almost none of the more than 11,000 financial institutions that comprise SWIFT engage in transactions with US-designated Iranian banks. In sum, coercing a disconnection of Iranian banks from SWIFT could lead to a small increase of pressure on Iran’s leaders, but, in our estimation, the action’s prohibitive downside risks outweigh its modest benefits.