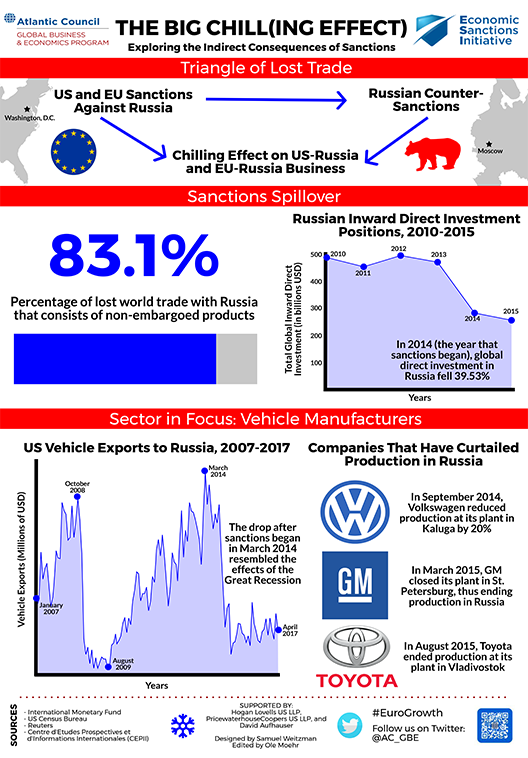

In March 2014, the United States and the European Union (EU) issued the first in a series of sanctions against the Russian Federation for its destabilization of Ukraine and annexation of Crimea. These restrictions, which initially focused on senior Russian government officials and private individuals, have expanded to include large corporations, financial institutions, and even entire economic sectors. In retaliation, Russia has adopted counter-sanctions of its own. With the US Treasury Department adding new sanctions in recent weeks—after the US Senate had passed its own legislation on the issue with almost unanimous support—it appears unlikely that the West will relent in the near future.

While sanctions’ efficacy as a foreign policy tool remains open to debate, economic data shows that the measures imposed by the United States and European Union have damaged Russia’s economy severely. By reducing trade opportunities and access to financial capital for many Russian firms, the restrictions have decreased Russia’s gross domestic product (GDP) by between 1 percent and 2 percent, thereby deepening the economic recession caused by the simultaneous nosedive in oil prices.

As the significant reduction in Russian GDP suggests, the effects of sanctions are not limited to those individuals and sectors targeted directly by the measures. A report by the International Monetary Fund (IMF) posits that US and EU sanctions had an indirect “chilling effect” on investment and trade for non-sanctioned industries. One sector where such a chilling effect may be discerned is in vehicular manufacturing. Multiple sanctions-related factors—including a shrinking economy and investor uncertainty—have led all of the world’s three largest automakers—Toyota, General Motors, and Volkswagen—to reduce production or even shutter factories in Russia. All told, between March 2014 and April 2017, US vehicle exports to Russia plummeted 89.26 percent. Likewise, in the first eight months of 2014 alone, German exports of motor vehicles and automobile parts to Russia decreased by 27 percent. As such, vehicle manufacturers—who were not themselves the targets of US or EU restrictions—experienced secondary economic effects on account of the sanctions.

One important caveat is that many of the effects of sanctions—both direct and indirect—are hard to disentangle from the concurrent fall in global oil prices during the same period of time. Russia’s economy depends heavily upon revenue from its hydrocarbon exports. In 2013 (the year before sanctions began), oil and natural gas sales constituted 68 percent of Russia’s total export revenue. Accordingly, for every one dollar decrease in the price of oil, Russia loses $2 billion in revenue. From March 3, 2014 to June 2, 2017, Brent Crude prices fell 54.69 percent, leading economists to refer to the combined effects of greater sanctions and cheaper oil as a “dual shock.” Additionally, structural flaws in the Russian economy are partly responsible for recent woes. Thus, while sanctions are certainly playing a role in depressing the Russian economy, other factors contribute to the country’s multi-year recession.

To learn more about best practices on economic sanctions, please read our newest Issue Brief, Economic Sanctions: Sharpening a Vital Foreign Policy Tool. The publication is part of the Global Business and Economics Program’s Economics Sanctions Initiative, which is made possible by generous support through Hogan Lovells US LLP, PricewaterhouseCoopers US LLP, and the Hon. David D. Aufhauser.