On January 16, a US Senate resolution to maintain US sanctions on the Russian aluminum giant RUSAL and its holding company EN+ failed to garner the necessary 60 votes to pass. As a result, the Trump administration lifted its economic sanctions on RUSAL and EN+ on January 27.

Russian oligarch Oleg Deripaska, who previously controlled both RUSAL and EN+ via his majority stake in the latter, remains subject to US sanctions. The Trump administration’s decision to lift the sanctions on EN+ has attracted significant political criticism in Washington. Our team of sanctions experts at the Atlantic Council assesses that this criticism is largely politically driven, rather than based on the technical aspects of the divesture deal that underlies the administration’s decision to lift the sanctions. For a deeper dive into the specifics of the deal between the US Treasury Department and EN+, read this piece by our senior fellows Brian O’Toole and Samantha Sultoon. This edition of the EconoGraphic outlines EN+’s new ownership structure, board composition, and distribution of voting rights. In addition, we are highlighting key risks that could trigger a re-imposition of US sanctions against EN+ and RUSAL.

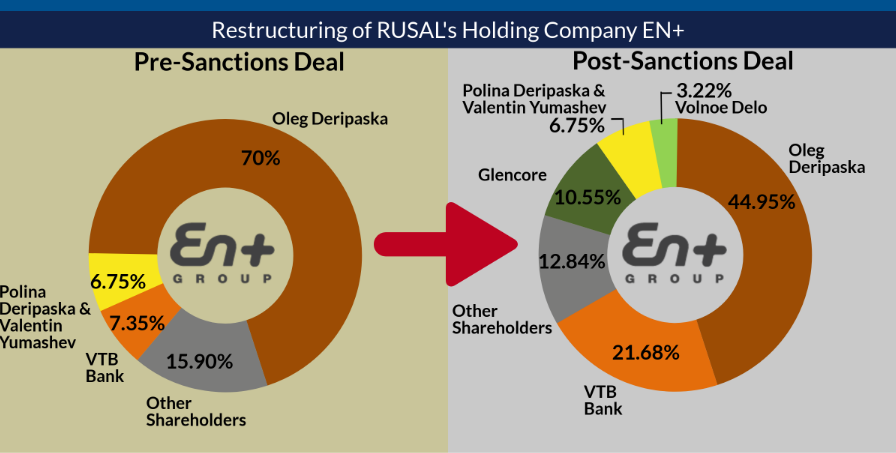

To understand the underlying logic of EN+’s restructuring agreement with the US Treasury Department, here is a quick primer on the Office of Foreign Assets Control’s (OFAC) 50 percent rule. This rule applies across sanctions programs and “dictates that entities owned 50 percent or more by sanctioned persons are themselves automatically sanctioned.” To address the 50 percent rule, Deripaska agreed to reduce his ownership stake in EN+ from 70 to 44.95 percent. This step alone, however, was insufficient to warrant delisting. Since EN+ was itself designated pursuant to two different executive orders (E.O. 13661 and 13662) for being owned or controlled, directly or indirectly, by Deripaska, additional steps were taken to lessen Deripaska’s opportunities to exert control over EN+ and RUSAL

This brings us to EN+’s other shareholders. VTB Bank OAO is a state-owned Russian bank that was sanctioned by the Obama administration in 2014 for Russia’s role in the conflict in eastern Ukraine. Through the divestiture deal, VTB received an increased stake in EN+ as collateral for existing debt Deripaska owes the bank. Glencore, an Anglo-Swiss multinational commodity trader known for its high-risk tolerance in dealing with autocrats and business magnates, acquired a share in EN+ in exchange for its existing minority stake in RUSAL. Volnoe Delo is a charitable foundation, owned by Deripaska, that took on a small portion of Deripaska’s shares. Deripaska’s former wife and father in law, Polina Deripaska and Valentin Yumashev, and other smaller shareholders own the remainder of EN+’s stock.

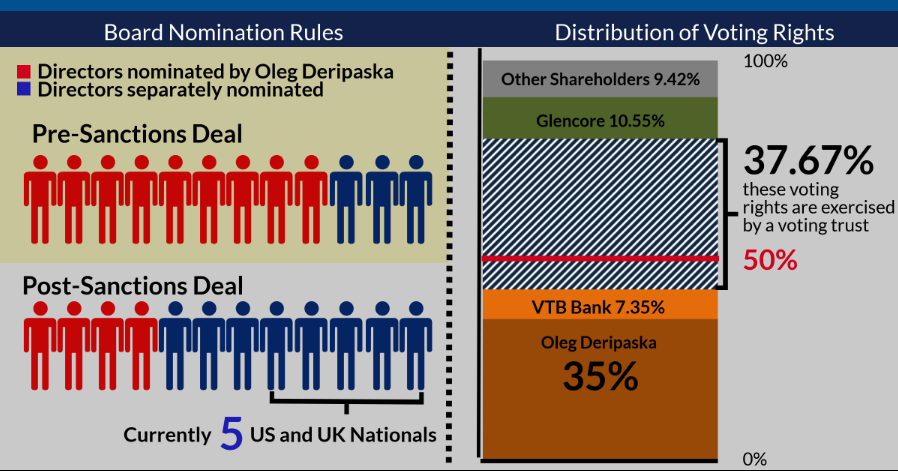

To counter the threat of Deripaska gaining indirect control, OFAC negotiated a redistribution of EN+’s voting rights. Deripaska’s voting rights are capped at 35 percent of EN+’s shares. His remaining 9.95 percent in voting rights will be exercised by a third-party trustee. Three US citizens, D.J Baker, formerly a partner at the law firm Latham & Watkins LLP, David Crane, a senior operating executive at Pegasus Capital Advisors, and Arthur Dodge as well as the international law firm Ogier Global Nominee, which is based in Jersey, will represent the voting trust. The trustee must vote “in the same manner as the majority of shares held by shareholders other than Deripaska.” In addition to reducing Deripaska’s own voting power, the third-party trustee will also exercise the voting rights for Deripaska’s former wife and father in-law, his foundation, and other shareholders with “family or professional ties” to Deripaska. VTB’s voting rights will not increase in accordance with its greater share in EN+. Instead, the trustee will step-in again to control VTB’s additional 14.33 percent of votes. By exercising 37.67 percent of EN+’s total voting rights, we believe the third-party trustee is in a good position to ensure that Deripaska does not maintain indirect control of the company. The divestiture agreement with Deripaska also mandates a reorganization of EN+’s board. Of the new board’s twelve directors, eight will have no “business, professional, or family ties” to Deripaska. OFAC reportedly vetted the eight board members to ensure that they are independent of Deripaska. To minimize the influence of the four directors nominated by Deripaska on EN+’s corporate governance, they will be excluded from the company’s important audit and nominations committees.

There are of course risks that could undermine the efficacy of the divestiture agreement. Deripaska could attempt to build a coalition of influence through his ties with former family members, his foundation, and other smaller shareholders. As explained above, however, the redistribution of voting rights ensures that such a coalition would not have the necessary votes to control EN+. Deripaska would need to cooperate with VTB, which has a 7.35 percent voting share, Glencore, and/or some of the smaller shareholders to gain control of EN+. It is of course credible that the Russian government might intervene to push VTB to collaborate with Deripaska. By contrast, it seems unlikely that Glencore would be able to work with Deripaska, since the company is already under the lens for its questionable business practices with OFAC-sanctioned Israeli businessman Dan Gertler. OFAC vetted all the smaller shareholders to make sure that they have no ties to Deripaska to minimize the risk of collaboration between the parties. In short, the divestiture agreement shifts control of EN+ out of Deripaska’s hand and puts up high barriers to ensure the Russian oligarch will not be able to establish indirect control as long as he is subject to US sanctions.

Ole Moehr is an Associate Director at the Atlantic Council’s Global Business & Economics Program.