China’s stock market collapse is the end of the road for many foreign investors

The long-running collapse of Chinese stocks has wiped out trillions of investment dollars and delivered another blow to an economy beset by property crisis, slow growth, and deflation, and has added uncertainty about Beijing’s very support for money-making. It may be the last straw for foreign institutional investors who once saw China as an essential destination.

The hit to share prices in Shanghai, Shenzhen, Hong Kong, and New York has reached some $7 trillion since early 2021 (over $6 trillion on the Chinese markets and hundreds of billions more from Chinese companies listed on Wall Street). While share prices have bounced back a bit in recent days as Beijing has taken steps to put a floor under the market, investors’ deep disenchantment remains.

The market downturn comes on top of the real estate debacle that caused developers to default on bonds and saddled China’s local governments with $13 trillion of debts. The stock downturn has specifically shaken technology companies that Beijing regulators had favored with fast-track access to initial public offerings of shares. While China led the world in IPOs during the first eight months of 2023, those issues subsequently dried up, and many startups are starving for cash.

All of this adds up to ever-deepening disenchantment for foreign institutional investors, many of whom made big bets on China a year ago in expectation of a post-COVID economic boom. As last year’s rally evaporated, an estimated 90 percent of those once-bullish foreign investors headed for the exits; some of them were also nursing their wounds from the property companies’ defaults on high-yielding, dollar-denominated bonds. The reversal of capital flows was amplified by foreign manufacturers moving factories away from China, producing an unprecedented decline in foreign direct investment last year.

The institutional exodus from China’s markets has been dominated by “passive funds” who buy stock index contracts and their component stocks, and long-term growth funds who buy and hold shares. While some money continues to come in—especially investors targeting China’s government bond market—net foreign inflows to China’s stock markets last year—at $6.1 billion— were the lowest they’ve been in recent years.

Every index tracking China share prices had a terrible 2023, with the declines continuing through last month. That includes indexes in China’s markets, Hong Kong, and those tracking Chinese companies on Wall Street. At the same time, markets from Tokyo to Mumbai to New York enjoyed solid gains, with the Asian markets especially benefiting from money pulled out of China.

A January 2024 Bloomberg analysis of 271 US pension funds with assets larger than $500 million showed only fourteen held in Chinese shares listed on Wall Street. Institutional investors are now favoring other emerging markets with better economic prospects and less political risk than China, as reflected in the performance of two Morgan Stanley Capital Index (MSCI) benchmarks.

The roots of the market’s downturn rest with government policies that have undermined consumer confidence and drained private sector dynamism. The authorities sought to deflate a property market bubble in 2020, but were slow to react when developers collapsed. Meanwhile leading e-commerce conglomerates had their wings clipped by an ideologically charged regulatory assault on what Beijing regards as corporate excesses—at the cost of lost job opportunities for millions of college graduates and anemic business investment.

US-China tensions also have loomed over the market and made many foreign investors more cautious about Chinese shares. Washington has declared various listed Chinese companies— largely technology and state-owned firms—off limits to US investors, and some of those firms have been forced to delist from American exchanges. In addition, US threats to impose wholesale delisting on all Chinese firms listed on Wall Street in a dispute over Securities and Exchange Commission access to their books contributed to the early stage of Chinese shares’ decline in 2021. But that threat receded after a bilateral agreement was reached in 2022.

Beijing recently has taken steps to support the stock market and address the underlying economic issues. It has sought to put a floor under the share prices by pushing state-controlled funds to buy stocks, restricting short-selling, and talking up the market. It also has promised more fiscal stimulus, which some analysts see boosting growth this year. But a stock market recovery will require evidence of a more forceful response to the property crisis and a sustained effort to stimulate the economy, especially household demand. (The market collapse also has hit China’s 220 million stock investors, many of whom also are homeowners.)

In Xi Jinping’s China there is always a need to keep a weather eye on the political winds. Even if the economy and property market bottom out in 2024, there are worrying signals about the government’s intentions for stock investors. Over the past few months, there have been various pronouncements directed at financial markets that suggest less tolerance for business as usual. For example, at a Chinese Communist Party Central Committee “study session” last month, Xi called for “the combination of the rule of law and the rule of virtue to cultivate a financial culture with Chinese characteristics” that would avoid “a single-minded focus on profit.”

It is worth recalling that the first shot in the campaign to rein in online companies was fired at the stock market in 2020, when regulators sank Alibaba Group’s plans to launch an IPO for its Ant Financial subsidiary after Alibaba founder Jack Ma publicly criticized regulators. What followed was a campaign under the banner of Xi’s 2021 call for “common prosperity”—a slogan associated with wealth redistribution that ultimately was directed at various unwelcome capitalist practices. The campaign was muted after it was seen to be undermining business confidence, but the latest broadsides from Beijing may prove unsettling to the markets.

Foreign investors tend to avoid commenting on Chinese political developments. But Lazard Asset Management offered a glimpse of their thinking last year when it wrote, “Factoring political risk into investment decisions will likely also be critical in the months and years ahead, given the scale of uncertainties—including the potential consequences of Common Prosperity.”

Nonetheless, some fund managers inevitably will return to China if the economy and markets show signs of a sustained recovery. But investing in China likely will become the domain of foreign bargain hunters and hedge funds, some of whom already are actively trading in the market (though apparently making more money in commodities-related securities). China’s markets will be a destination where investors will be able to make fast profits, but also risk losing their shirts—as occurred last month when the Singapore-based hedge fund Asia Genesis was forced to close after losing a bet that Chinese equities would rally.

All of which must be considered ironic since one of the original purposes of China’s policy of opening its markets to foreigners was to attract stable, long-term institutional investment. Instead, most of those coveted investors will be elsewhere, and the fund managers who remain could end up contributing to the volatile swings in fortune that are everyday life in China’s markets. That will hardly be an outcome conducive to Xi’s “rule of virtue.”

Jeremy Mark is a senior fellow with the Atlantic Council’s Geoeconomics Center. He previously worked for the IMF and the Asian Wall Street Journal. Follow him on Twitter: @JedMark888.

At the intersection of economics, finance, and foreign policy, the GeoEconomics Center is a translation hub with the goal of helping shape a better global economic future.

Further reading

Wed, Jan 10, 2024

China’s local government debts are coming due

Econographics By Jeremy Mark

China's economic slowdown brings local government debts into sharp focus, threatening infrastructure and social services.

Mon, Feb 5, 2024

China Pathfinder update: Lack of policy solutions in second half of 2023 belies official data

Issue Brief By

Through the second half of 2023, the gap between China’s impressive official data and visibly underwhelming consumer demand, unresolved local government debt problems and an unprecedented drop in foreign direct investment was stark.

Mon, Jan 22, 2024

Dedollarization is not just geopolitics, economic fundamentals matter

Econographics By Niels Graham, Hung Tran

Geopolitical explanations have dominated recent analysis on dedollorization. While it is certainly a key factor, macroeconomics matter as well. US interest rates and a rising dollar are encouraging other countries to search for alternatives.

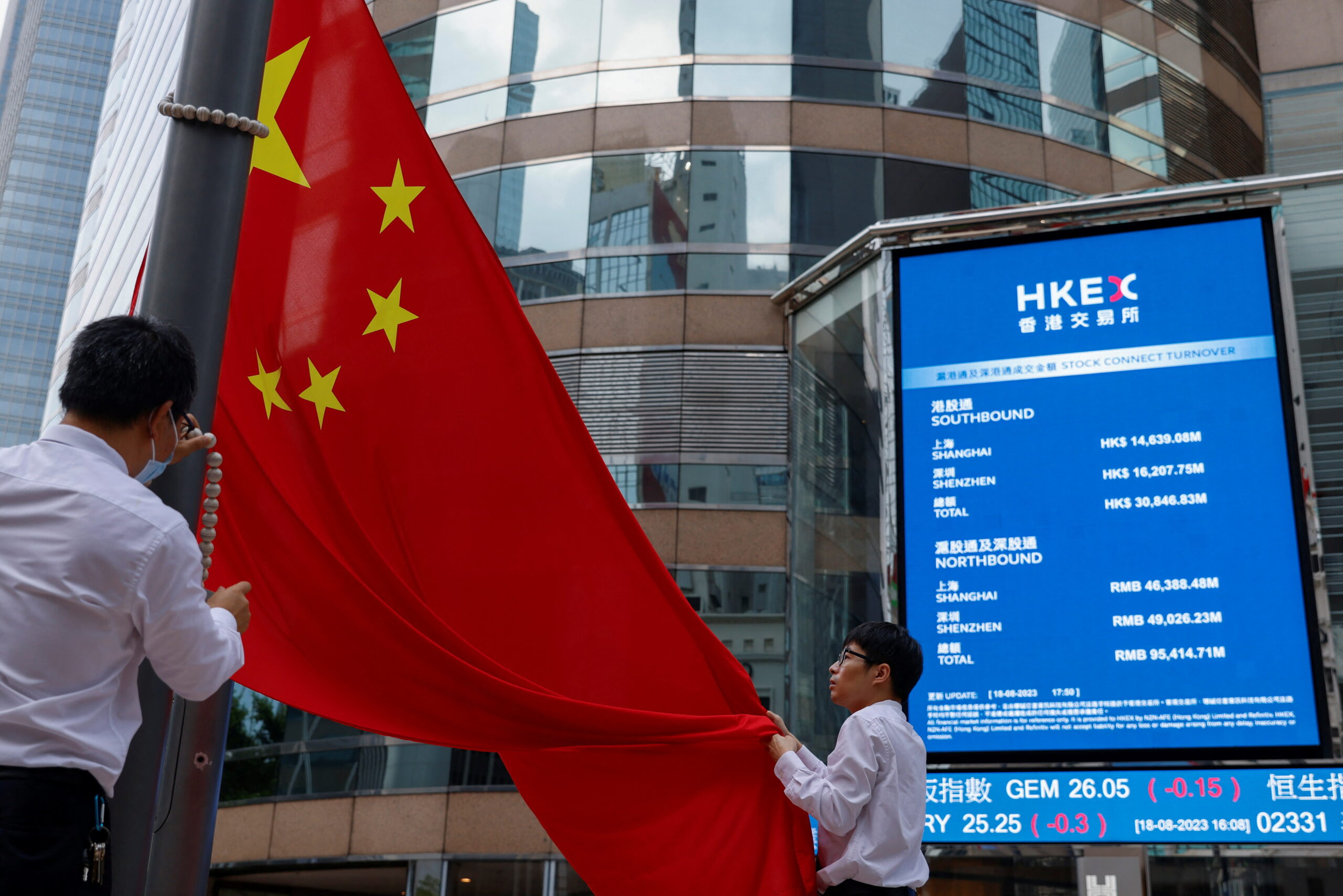

Image: Staff lower Chinese national flag in front of screens showing the index and stock prices outside Exchange Square, in Hong Kong, China, August 18, 2023. REUTERS/Tyrone Siu