On Thursday, May 23, 2024, Senior Fellow Pepe Zhang of the Adrienne Arsht Latin America Center gave testimony before the US-China Economic and Security Review Commission in a hearing on key economic strategies for leveling the US-China playing field in trade, investment, and technology. Below is a written version of his testimony.

Summary

At the Commission’s request, this testimony evaluates US economic engagement with Latin America and the Caribbean (LAC)—taking into account competition and comparison with Chinese efforts, where applicable—and provides recommendations for improvement. Specifically:

- Section I: The testimony provides an overview of China’s rise in LAC’s economic context

- Section II: It then describes recent US economic engagement—with an emphasis on the Americas Partnership for Economic Prosperity (APEP)—as well as regional reception and needs across three areas:

- Greater US policy attention

- More US resources

- Enhanced policy continuity

- Section III: Based on the above, the testimony prescribes three policy tools and pathways to enhance US economic engagement with the region, related in particular to supply chains:

- Trade policy: tariff, nontariff, and complementary measures

- Industrial policy that induces self-sustaining and whole-of-ecosystem supply chain enhancements

- Development policy: financial and nonfinancial development assistance and cooperation

- Section IV: In conclusion, it distills the preceding analysis into nine recommendations to the Commission and congressional and other stakeholders across three levels:

- Policy level: Recommendations regarding trade policy, industrial policy, and development policy tools

- Resource level: Recommendations to unlock more resources for specific US government agencies and efforts and multilateral development organizations

- Strategic level: Strategic recommendations to ensure US policy attention, resources, and continuity towards LAC

I. The rise of China in regional economic context

The Latin American and Caribbean region (LAC) has registered on average a modest 2-2.5 percent annual growth rate over the past thirty years, among the slowest in the world. To varying degrees, most countries in the region saw considerable improvements in monetary and fiscal policymaking. But, they continue to face structural challenges such as limited productivity gains, socioeconomic inequality, and low levels of foreign investment. In the same period, the lack of significant new domestic growth drivers—coupled with waves of trade liberalization efforts around the world and several regional economies’ growing export success—prompted LAC efforts to enhance and diversify economic engagement with international partners.

Against this backdrop, China swiftly emerged as a key economic player in LAC, especially in South America, across four main areas: trade, foreign direct investment (FDI), official lending, and infrastructure development.1Much of the data in this section comes from: Pepe Zhang and Felipe Larraín’s America’s Quarterly article, “China Is Here to Stay in Latin America,” published in January 2023.

1. Trade

Trade represents the most significant area of Chinese economic engagement with LAC. The dramatic expansion in bilateral trade underscores the growing economic interdependence between these two regions. Over the past twenty-five years, trade between China and LAC has multiplied over twenty times to nearly $500 billion in 2023. China has become by far the largest trading partner for countries like Chile, Peru, and Brazil, accounting for over 30-40 percent of their total exports. By comparison, this is three to four times higher than China’s share of total US, German, or European Union (EU) exports (less than 10 percent).

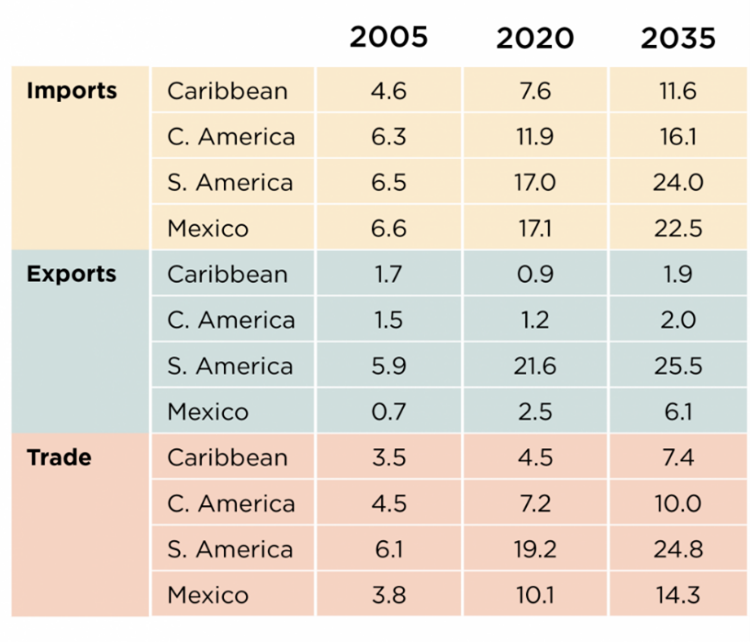

Trade flows remain robust in the other direction as well. LAC consumers increasingly favor Chinese goods and services, including high value-add technology products such as cell phones and automobiles or services like TikTok. One important caveat on China-LAC trade is that sizable differences exist across LAC subregions: South America (mostly commodity exporters) is much more dependent on trade with China than Central America, Mexico, and the Caribbean (Figure 1).

Figure 1: China’s participation in LAC subregions’ trade in 2005, 2020, and 2035 (projected, in percent) 2Tatiana Prazeres, David Bohl, and Pepe Zhang, “China-LAC Trade: Four Scenarios in 2035.” Atlantic Council, May 2021. https://www.atlanticcouncil.org/in-depth-research-reports/china-lac-trade-four-scenarios-in-2035/.

2. Investment

While Chinese investment cratered globally starting 2016, particularly in major markets like the EU and the United States, it has shown smaller decline and relative resilience in LAC. This is attributable to at least two regional factors: still-attractive assets and valuations and a friendlier regulatory environment for Chinese investors (compared to heightened scrutiny in advanced economies).

Brazil is the largest recipient of Chinese investment in LAC, and China is Brazil’s top investor. In 2021, Brazil received a record $5.9 billion in Chinese FDI, surpassing the $4.7 billion China invested in the United States in the same year—remarkable considering that the Brazilian economy is one tenth the size of the United States’. In terms of sectors, Chinese FDI and mergers and acquisitions in the region traditionally concentrated in energy, mineral, and utilities, but have been diversifying into new areas such as ICT and manufacturing.

3. Lending

Chinese official lending to LAC peaked between 2007 and 2016, averaging more than ten billion dollars annually. But it has since declined significantly as part of a global retrenchment in Chinese government lending overseas. As Beijing’s cautiousness continues, new activities in this space will likely involve renegotiations and restructurings of existing loans rather than new disbursements. Venezuela, which represents less than 5 percent of regional GDP, has been the top recipient (approximately 40 percent of stock) of Chinese official lending to LAC.

4. Infrastructure development

Chinese construction firms have actively participated in LAC’s infrastructure development through public tenders, winning numerous high-profile projects and at times outcompeting US and European firms. The visible, tangible nature of infrastructure projects (roads, ports, stadiums, hospitals, etc.) contributes to China’s growing economic presence in the region. As well, they help to alleviate excess capacity in China’s domestic industrial and construction sectors.

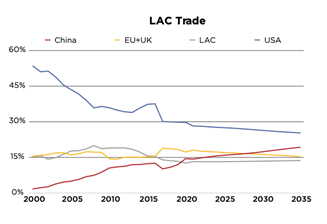

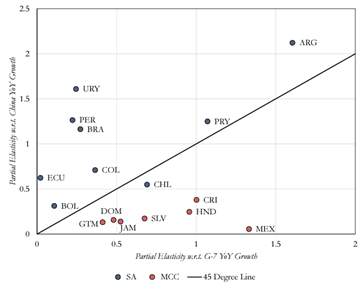

China’s economic engagement is generally seen as a growth driver and therefore well-received by regional stakeholders. For some South American nations, trade flows and business cycles have already become more aligned and synchronized with China’s than with traditional partners’ including the Group of Seven (G7) economies (Figures 2 & 3). Such strong economic linkages have potential implications for the effectiveness of US policy. For instance, the United States may find it increasingly challenging to leverage certain geoeconomic tools (e.g., US-led coordination of multilateral sanctions) against China in the region. In general, most LAC countries already avoid being caught up or publicly choosing sides in the US-China competition.

Figure 2: Major trading partners’ participation in LAC Trade from 2000 to 2035 (projected) 3Prazeres, Bohl, and Zhang, “China-LAC Trade: Four Scenarios in 2035.”

Figure 3: G7 vs. Chinese growth impact on and correlation with LAC economies 4World Bank. “Leaning Against the Wind: Fiscal Policy in Latin America and the Caribbean in a Historical Perspective.” LAC Semiannual Report (April). Washington, DC: World Bank, 2017. https://documents1.worldbank.org/curated/en/841401495661847413/pdf/P162832-05-24-2017-1495661844209.pdf

Note: Placement above the forty-five-degree line indicates a country’s growth is more responsive to China than to the G7.

SA stands for South America. MCC stands for Mexico, Central America, and the Caribbean.

II. Recent US economic engagement and regional reception

1. Recent US economic engagement including APEP

Despite China’s growing economic footprint in South America, the United States remains LAC’s most important economic partner in aggregate terms. LAC trades more with the United States than it does with any other country on the back of stronger-than-ever commercial ties between the United States and Mexico. In 2023, the size of US-Mexico trade alone (approximately $800 billion) far exceeded the size of China’s trade with the entire LAC region (approximately $500 billion). The United States also maintains an expansive, outsize network of existing trade agreements in the hemisphere, boasting twelve free trade agreement (FTA) partners in it (and only eight outside). Additionally, the United States is consistently the largest foreign investor in the region, followed by Spain. The potential for investment and collaboration in strategic and emerging sectors is significant: three out of the seven countries eligible for US government support through the International Technology Security and Innovation (ITSI) fund—created under the 2022 CHIPS Act to strengthen semiconductor and telecommunications supply chains—are located in LAC.

With a handful of ideological exceptions, countries in the region largely welcome pragmatic international economic engagement including with the United States. The latest flagship US regional economic policy initiative is APEP, announced by the Biden administration in June 2022 during the Ninth Summit of the Americas in Los Angeles. APEP’s four main priorities are to foster regional competitiveness, resilience, shared prosperity, and inclusive and sustainable investment in LAC. It currently has twelve members: Barbados, Canada, Chile, Colombia, Costa Rica, the Dominican Republic, Ecuador, Mexico, Panama, Peru, the United States, and Uruguay.

APEP is structured around three tracks (foreign affairs, finance, and trade), with respective working groups led by individual countries. The working groups cover a wide range of topics, with the initially established ones addressing eight: entrepreneurship, digital workforce development, clean hydrogen, rule of law, sustainable health infrastructure, sustainable food production, water and basic sanitation, and space. Notable announcements so far include a USAID Entrepreneurship Accelerator with initial support from Canada and Uruguay, digital technology workforce development including the first APEP Semiconductor Workforce Symposium held in Costa Rica, and innovative development finance cooperation with the Inter-American Development Bank on climate and migration issues. 5White House. “Fact Sheet: President Biden Hosts Inaugural Americas Partnership for Economic Prosperity Leaders’ Summit.” The White House, November 3, 2023. https://www.whitehouse.gov/briefing-room/statements-releases/2023/11/03/fact-sheet-president-biden-hosts-inaugural-americas-partnership-for-economic-prosperity-leaders-summit/.

A significant component of APEP is its focus on hemispheric trade and supply chain resilience. In particular, the first APEP trade ministers’ meeting in March 2024 emphasized three key priorities: trade facilitation and digitalization of customs procedures; conducting a gap analysis of critical value and supply chains; and trade for the benefit of small and medium-sized enterprises and underserved communities. Sector-wise, APEP has initially targeted energy, semiconductors, and medical supplies as priority sectors, largely consistent with the four product categories identified by the Biden administration’s Executive Order 14017, as well as broader US interagency efforts on friendshoring/nearshoring.

2. Regional reception

APEP and other efforts of US economic engagement are generally well received in LAC. But they can be improved in three ways from a regional perspective:

a. Policy attention

A main criticism of US foreign policy towards LAC over the past two decades is that Washington has overlooked the region to accommodate priorities elsewhere. More recently, the symbolism of hosting two highest-level hemispheric political events in the United States (the 2022 Summit of the Americas and the 2023 APEP Leaders’ Summit) helped to mitigate such perception to some extent. But systematically shoring up US commitment to the region will demand a strategic rethink of what is at stake.

The US economy has much to gain, buoyed by a more prosperous and stable neighboring region. And it has even more to lose in an economically unstable Western Hemisphere, with secondary effects such as migration challenges already impacting US domestic politics.

In terms of nearshoring/friendshoring, LAC offers several valuable advantages that the United States would do well to leverage and reinforce, in an era of global supply chain reshuffling and heightened geopolitical uncertainty:

- geographic proximity;

- competitive wages;

- an overwhelming majority of democratic, peaceful, and friendly states (albeit imperfect);

- a diverse group of governments and companies interested in working with the United States, from the manufacturing powerhouse in Mexico, to dynamic small open economies with proven macroeconomic and sectoral successes such as the Dominican Republic, and South American commodity exporters that are increasingly influencing global food security, energy, and climate transition agendas. 6Pepe Zhang and Otaviano Canuto. “Global Leadership for Latin America and the Caribbean.” Project Syndicate, September 2023. https://www.project-syndicate.org/commentary/latin-america-caribbean-global-leadership-food-climate-finance-by-pepe-zhang-and-otaviano-canuto-2023-09.

b. Resources

Another key regional observation regarding US economic engagement concerns the need for more concrete follow-up actions and adequate resource allocation. This is often considered a byproduct of insufficient US policy attention described above. For instance, APEP experienced a perceived hiatus between being announced during the 2022 Summit of the Americas and regaining momentum around the 2023 APEP Leaders’ Summit. Since the Leaders’ Summit, however, countries have quickly ramped up technical work and senior officials’ meetings, with a view to achieve tangible progress ahead of the second APEP Leaders’ Summit, to be held in Costa Rica in 2025.

With respect to resources, members have understandably expressed interest in accessing economic opportunities, US investment, and financial support through APEP. For the time being, a substantial part of such support will likely be mobilized through innovative partnerships, including with different US government agencies, extra-regional allies, APEP members themselves, the Inter-American Development Bank especially its private sector arm IDB Invest, and potential resources from the recently introduced Americas Trade and Investment Act (Americas Act). Going forward, a clearer definition of APEP’s governance structure, membership criteria, and pathways to resources can more effectively unleash opportunities for the benefit of APEP members.

c. Policy continuity

Economic and political relations between the United States and LAC risk becoming more unpredictable amidst electoral cycles across the Americas, including the upcoming 2024 US presidential election. Potential elections-induced policy shifts, if more drastic than normal, could undermine US interests. For instance, as regional partners grapple to navigate and reconcile different US administrations’ flagship LAC policy initiatives, they do not face similar struggles with China and its Belt & Road Initiative.

In this context, the Americas Act recently introduced by Senators Bill Cassidy (R-LA) and Michael Bennet (D-CO) alongside Representatives Maria Elvira Salazar (R-FL), Adriano Espaillat (D-NY), and Mike Gallagher (R-WI) brings about a remarkable opportunity to ensure long-term US policy continuity and coherence in LAC. This bipartisan and bicameral legislative effort proposes a comprehensive vision for US economic partnership with the region, underpinned by trade, investment, and supply chain integration, as well as significant new resources. Moreover, in a rare and much-needed display of legislative-executive coordination, the Americas Act built a bridge to the Biden administration’s efforts by fast-tracking APEP members’ eligibility for Americas Act resources. 7“S.3878 – Americas Act.” 118th Congress (2023-2024). Accessed November 16, 2023. https://www.congress.gov/bill/118th-congress/senate-bill/3878/text/is#toc-idbd7b93971b294b1fa02e3ad10158a324.

III. Tools and pathways for future enhancements

To bolster economic integration between the United States and LAC with a focus on supply chain integration, it is vital to better utilize, innovate, and explain specific US policy tools to regional partners. At a high level, such tools should play to the unique strengths—and take into account the limits—of the US economy, US government, and their hemispheric ties. Where possible, they should be complemented by targeted capacity building that fosters stronger, self-sustaining local economies in LAC, as well as a more symbiotic economic relationship with the United States. Specifically, such tools may span across three interconnected areas: (a) trade policy; (b) industrial policy; and (c) development policy.

1. Trade policy

Trade policy instruments include both tariff and nontariff measures.

- Tariff: The scope for using traditional trade agreement/tariff instruments is limited, due to ongoing domestic backlash against expanding foreign access to the US market. In the absence of new FTA negotiations, the United States and hemispheric partners are focusing recent efforts on making the most out of the existing US trade toolbox and network. Some examples are legislative measures that aim to surgically insert smaller economies (such as Uruguay, Ecuador, and Costa Rica) through existing preferential trade arrangements, while creating pathways towards eventual bilateral FTAs in some cases.

- Nontariff: More can and should be done in the realm of nontariff measures, such as harmonizing hemispheric regulatory and phytosanitary standards, streamlining customs procedures, and improving connectivity infrastructure. These measures help to reduce the cost and time of intraregional trade flows, thus boosting the efficiency and competitiveness of hemispheric production and exports. Here, the United States can play a leadership role, facilitated by its existing FTAs with twelve countries in the region.

Greater interoperability—tariff and nontariff—among US trade ties with hemispheric partners is a practical way to advance the regional economic integration agenda in LAC, which has stalled in recent decades due to political polarization within and across countries. With intra-regional trade representing only 20 percent of LAC’s total trade (the lowest and slowest-growing of all world regions), nearshoring—or regionalized supply chains—in the Americas cannot meet its full potential. 8International Monetary Fund. “How Latin America Can Use Trade to Boost Growth.” IMF Blog, November 16, 2023. https://www.imf.org/en/Blogs/Articles/2023/11/16/how-latin-america-can-use-trade-to-boost-growth.

- Complementary coordination measures and special considerations may include modernizing policies and regulations to better address digital trade, intellectual property, and labor standards concerns; accumulation of rules of origin for strategic sectors and products; an ambitious plan towards eventual interoperability with FTAs in the region currently not involving the United States; an inclusive focus on integrating smaller, dynamic economies (many of which are strong US allies) that may otherwise face hurdles to enter regional/global supply chains, due not only to price but scale competition vis-à-vis Asia, etc.

2. Industrial policy

Beyond conventional trade tools, enhanced industrial policy is needed to strengthen productive capabilities and integration within the Western Hemisphere. Well-designed tools (US policies, incentives, investments, and signaling) in this area should focus not on creating one-off success stories but inducing self-sustaining and whole-of-ecosystem supply chain enhancements.

- Whole-of-ecosystem: One of the main advantages of China/Asia-based manufacturing today is its complete, sophisticated supply ecosystems, where a wide range of specializations and suppliers are available along entire value chains upstream and downstream. If the ultimate US policy objective is to replicate these ecosystems in the Western Hemisphere, policymakers can extract helpful lessons from Asia’s flying-geese-paradigm industrialization. In this paradigm, Japan as a “leading goose” invested in, shared knowledge about, and induced industrial upgrading in the rest of Asia. By doing so, it made Japanese/Asian exports more cost-competitive, while creating positive spillover effects that led to self-sustaining regional supply chains and additional comparative advantages. The United States—and by extension, the North American free trade area—should serve as a similar leading goose in the Western Hemisphere.

However, the whole-of-ecosystem approach may prove challenging or take considerable time and investment to materialize in certain sectors/products, e.g., when regional partners or the United States itself does not possess the specializations or technologies needed. In these cases, collaboration with trusted extra-regional allies and surgical interventions to tackle skills gaps or supply chain chokeholds can help to accelerate the process.

- Self-sustaining: Public sector investment and assistance through the Inflation Reduction Act (IRA) and the CHIPS Act are a first step in the right direction to push supply chains into the region (“push factors”). Efficient coordination with regional partners is important for financial, capacity, and competitiveness reasons. Many regional governments, while interested, may have limited fiscal space to develop these supply chains independently or have limited technical/industrial capabilities to qualify for US support (or learn how to qualify).

Creating US interagency roadmaps for hemispheric supply chain development, with private sector input, will be vital to building such capabilities in LAC to pull/attract investments (a key “pull factor”) and ensuring long-lasting success. Importantly, the roadmaps must also introduce a healthy degree of domestic competition, possibly through a sunset provision. Some of LAC’s unsuccessful industrialization attempts in the last century—characterized by import-substitution industrialization as opposed to East Asia’s export-oriented industrialization—generated uncompetitive firms and resource misallocation, offering a cautionary tale.

A US strategy designed to advance supply chain push and pull factors should also include local workforce development (a key element of APEP) and infrastructure development (from logistical to energy conditions necessary to ensure export competitiveness); synergy with US-led sector-specific initiatives (such as the Minerals Security Partnership); bilateral high-level dialogue mechanisms (similar to the US-Mexico High-level Dialogue, the US-Guatemala High-Level Dialogue, etc.); US support of regional initiatives such as the Alliance for Development in Democracy (ADD) Business Council’s Supply Chain Working Group, etc.

3. Development policy

Development policy tools increase supply chain competitiveness and broader economic resilience in LAC by nurturing additional pull factors conducive to nearshoring, such as project bankability, macroeconomic stability, physical infrastructure, skills and productivity, and disaster preparedness and response. 9Other nearshoring pull factors include regulatory and legal certainty and simplicity, physical infrastructure, export promotion and facilitation, effective public institutions, innovation capacity, etc. The United States has several unique tools at its disposal, both financial and nonfinancial, to support regional economic development.

- Financial: The most direct financial instruments of the US development toolbox are provided by US agencies such as USAID, DFC, USTDA, and EXIM. With varied priorities and operations, they can offer financing to advance US commercial and foreign policy interests while supporting local development needs. A growing focus and challenge for some of these agencies is to mobilize the private sector. For instance, on the investment side, although US companies have successfully led the United States to overtake the EU as LAC’s number one foreign investor, opportunities exist to unlock additional private sector investment if the agencies are authorized to more easily and substantially mitigate certain country and project risks.

The Washington-based international financial institutions (IFIs) are another distinctive asset for US development and foreign policy in LAC. For example, the COVID-19 pandemic demonstrated once again that these organizations are more willing and capable—than their Chinese policy bank counterparts—to provide counter-cyclical support to LAC countries in need. Such support took place through the IMF’s liquidity or macro stabilization programs, as well as development operations from the IDB or the World Bank that directly boosted governments’ recovery and growth efforts, improved public infrastructure, health services, or skills training, or indirectly freed up additional fiscal resources for development. Though often underappreciated, the IFIs’ close coordination with the US Department of Treasury (their largest shareholder) contributes to hemispheric economic stability and development.

- Nonfinancial: Numerous US agencies drive development in LAC through a wide array of nonfinancial assistance and cooperation, including training programs organized or contracted by the Departments of Commerce, Treasury, State, Energy, and others. These programs build capacity among LAC public sector, private sector, and civil society beneficiaries, covering specific technical issues such as commercial laws, government procurement, independent journalism, illicit finance, etc.

Additional examples include the Department of Defense and US Southern Command (SOUTHCOM)’s security cooperation with countries affected by rising crime and violence, or their operational support for natural disaster preparedness and response in small, disaster-prone Caribbean Island states. While these efforts may not be economically focused by design, they generate immense economic value, by protecting lives, jobs, supply chains, the investment climate, and government balance sheets. They also foster goodwill. The fact that the US remains the region’s partner of choice in these noneconomic areas reflects the multi-dimensional, symbiotic nature of the US-LAC relationship. Hemispheric policymakers would do well to further explore these areas as complementary pathways toward greater economic integration.

IV. Recommendations

In summary, and with the Commission’s mandate in mind, I propose the following nine recommendations to advance US interest and leverage US strengths in topics covered by this testimony on three levels: The policy level, resource level, and strategy level.

Policy level

In coordination with the executive branch, Congress can help innovate and utilize US policy tools across three interconnected areas:

- Trade Policy: Use tariff, nontariff, and complementary measures to strengthen hemispheric trade and integration under US leadership, without resorting to politically thorny market access issues. A key element here is to leverage the United States’ existing preferential trade agreements with twelve regional partners, as well as their resulting economic linkages and technical interoperability.

- Industrial Policy: Nurture nearshoring push factors (US policies and incentives) and pull factors (regional competitiveness conditions) to build self-sustaining, whole-of-ecosystem productive capacity in LAC for certain sectors/products/supply chain segments. This includes formulating time-bound, US interagency roadmaps for hemispheric supply chain development, in coordination with regional partners and the private sector.

- Development Policy: Enhance financial and nonfinancial (technical/operational) assistance from various US government agencies and Washington-based international financial institutions to strengthen economic development, resilience, and nearshoring pull factors in LAC. The goal is to create more competitive regional economies as well as more symbiotic economic partnerships with the United States.

Resource level

Congress can unlock resources pivotal to implementing and supporting the policy-level recommendations above, for example: - Increase resources to deploy more foreign service, development, commercial officers in ways that (a) advance US foreign policy and commercial interests in LAC across the trade, industrial, and development policy areas outlined above, including through APEP-related initiatives; (b) supporting regional development needs and capacity building; (c) deepen regionalized China expertise and capability, particularly through the Department of State’s Regional China Officers program.

- Increase resources for public diplomacy efforts that better specify and highlight the value of positive US economic engagement in LAC. This includes measurable impact of US policy actions recommended above, as well as nongovernmental US accomplishments and facts, e.g., the United States consistently remains by far the region’s largest investor and trading partner in aggregate terms.

- Optimize budgetary or financing rules for organizations like DFC and EXIM so they can meet the growing and evolving needs of the beneficiaries, expanding progress made in the Better Utilization of Investments Leading to Development Act of 2018 (“BUILD Act”).

- Approve/Allocate resources to DC-headquartered international financial organizations—including the Inter-American Development Bank Group and the World Bank Group—for future capital increases and replenishments. These organizations are well-positioned to provide high-quality, impact-driven development assistance to LAC. Additionally, they can complement bilateral US efforts, as evidenced by the recently announced IDB Invest-DFC co-financing framework.

Strategic level

Through its legislative, policy, financial, and oversight authority, Congress can play a key role in guiding the strategic direction of US foreign policy towards LAC, in particular: - Draw more attention and resources to LAC. The US government including Congress must work to recalibrate regional perceptions of US neglect and advocate for a more active role for the United States in leading hemispheric economic integration. LAC has much to offer as a reliable partner in an evolving global context, and it is in US national interest that this neighboring region realizes its full potential. The recently introduced Americas Trade and Investment Act (“Americas Act”) is a promising endeavor in this regard.

- Ensure coherence of US economic engagement with LAC. At a time when domestic political polarization across the region and in the United States is making hemispheric relations less stable and effective, Congress can play a key role in informing a high-level, bipartisan, and coherent US strategy towards LAC that better transcends electoral cycles. Recent executive-legislative efforts to connect APEP and the Americas Act are an encouraging signal in this regard.

Image: People walk inside the upper floors of the rotunda of the U.S. Capitol building at sunset at the U.S. Capitol in Washington, U.S., January 4, 2023 REUTERS/Evelyn Hockstein/File Photo