Economic challenges are a barrier to Argentina’s prosperity

Table of contents

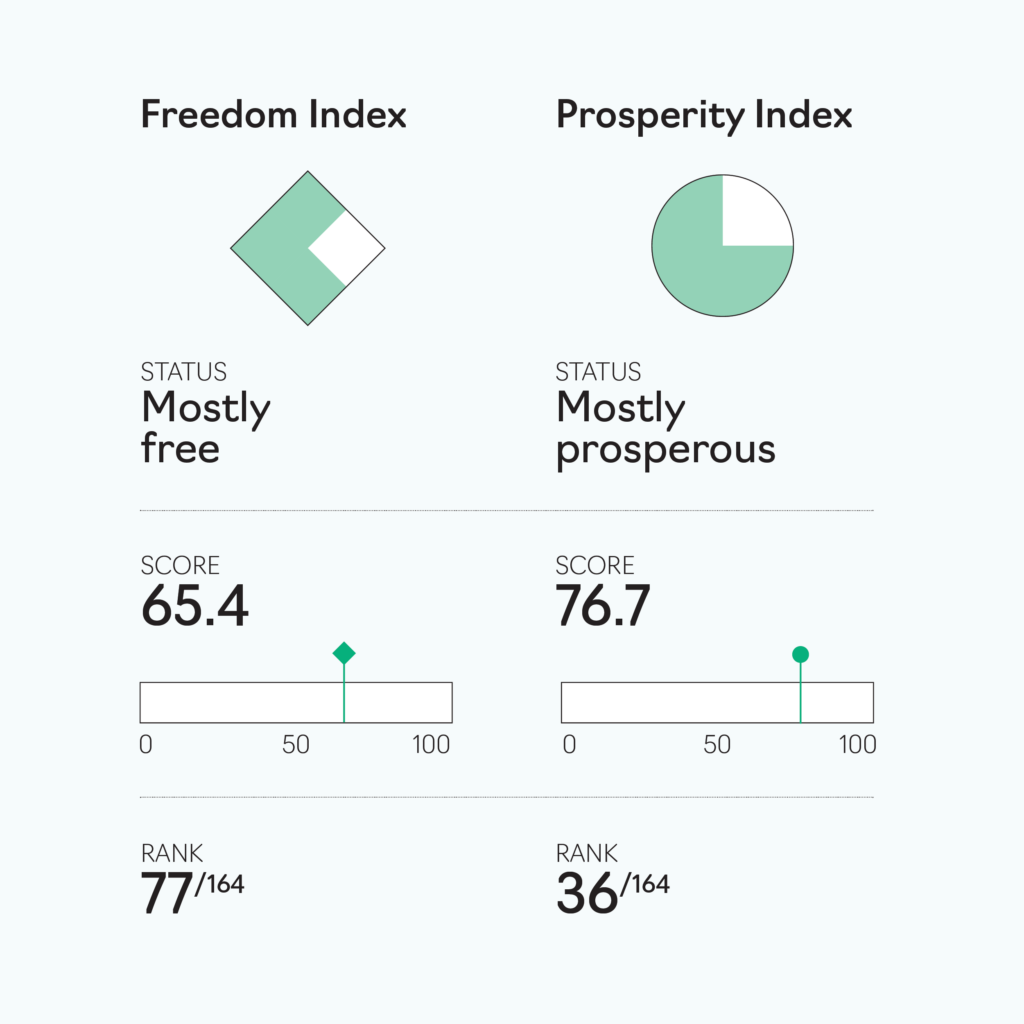

Evolution of freedom

The aggregate Freedom Index for Argentina correlates very well with the political events that have taken place in Argentina since the 1990s. Following the hyperinflation of 1989, Carlos Menem, from the right wing of the Peronist Party became president. He introduced significant market-friendly reforms embracing the Washington consensus and, in 1991, a currency board (known as the “convertibility regime”). This policy mix managed to lower inflation and generate almost a decade of growth. However, insufficient fiscal adjustment, the rigidities in the economy, and the overvaluation of the real exchange rate under the currency board pushed unemployment upward. The situation worsened following the Asian crisis in 1997 and the Brazilian Real devaluation in 1998. The convertibility regime, with its fixed exchange rate, made it difficult for Argentine exports to remain competitive. The economy fell into a recession and unemployment continued climbing. In 1999 the opposition, led by Fernando de la Rúa, won the elections but was unable to solve the economic puzzle created by the exchange rate overvaluation under the convertibility regime and an economy in stagnation. The recession turned into a deep crisis by 2001. The 2001–02 crisis was the equivalent of the Great Depression for Argentina, with output falling by around 20 percent. The crisis included a sovereign debt default, bank runs that forced the government to introduce a corralito (restrictions on the withdrawal of funds), and deep social unrest. These events led to the resignation of President Fernando de la Rúa in December 2001, and, after a few weeks of political upheaval, a more centrist Peronist government led by Eduardo Duhalde replaced him. The convertibility regime was abandoned and a backlash against the market-friendly reforms of the 1990s ensued.

The left wing of the Peronist party won the 2003 presidential elections under Néstor Kirchner. He governed from 2003 to 2007, and was succeeded as president by his wife Cristina Fernández de Kirchner who took office until 2015. Néstor Kirchner managed to reestablish the credibility of the political system, which had been severely affected by the 2001/02 crisis. However, he and his wife ran typical left-wing populist administrations that benefited from a very favorable international economic environment with high commodity prices (between 2002 and 2008 the price of soy, Argentina’s main commodity export, went from US$189 per ton to US$453 per ton) and low US interest rates. They used the commodity windfall to significantly increase public spending, from 22 percent of gross domestic product (GDP) in 2003 to 41 percent of GDP in 2015. Such a policy, though unsustainable, made Néstor Kirchner and Cristina Fernández’s governments popular, and allowed them to build a new political dynasty. However, in the process, the high public spending seriously damaged the ability of the economy to grow. Between 2012 and 2015, as the commodity boom ended and the effects of the imbalances of the previous years started to show up, the economy stagnated, the fiscal situation worsened, and inflation continued to increase. The government introduced a series of restrictions and distortions, in particular in terms of the ability of citizens and firms to access foreign exchange. We can clearly observe how the deteriorating economic environment is reflected in a decline in the overall economic freedom subindex during these years.

President Mauricio Macri, leader of the political coalition Cambiemos, took office in December 2015. He took the reins of an economy that was in default and with a large primary fiscal deficit (around 4 percent of GDP in 2015). In addition, there were a number of significant problems and distortions to address. The real exchange rate was overvalued and, in spite of the presence of import restrictions, the current-account deficit was significant. Exports had declined in the four previous years and net international reserves at the Central Bank were negative, despite the capital controls. Annual inflation was 30 percent and there was a large excess supply of pesos due to the monetary financing of the fiscal deficit in the previous years. And the prices paid for public utilities prices were severely distorted, covering only a quarter of their cost of production. However, the narrow runoff electoral victory (51 percent to 49 percent) did not provide President Macri with a mandate to overhaul the Argentine economy. Besides, the governing coalition was in the minority in Congress and had little territorial power. In spite of these political weaknesses, Macri’s government immediately implemented a number of market-friendly reforms: restrictions on capital flows were eliminated, policies that increased competition in several sectors of the economy were put in place, and the institutional framework was strengthened. At the same time, the government gradually began to balance the budget, which meant taking unpopular measures. The overall Freedom Index increases sharply over these years, capturing the impact of these reforms.

The slow pace at which the fiscal imbalance was corrected—together with the strict monetary/exchange rate regime adopted—implied that the government had to rely on international credit markets to finance the fiscal deficit. This strategy made the economy vulnerable if external financing were to dry up. This is precisely what happened in early 2018 when the US Federal Reserve increased its interest rates, causing a sudden stop in international lending to emerging economies. At the same time a severe drought hit the country. These external factors, together with the strong resistance of the opposition in Congress to the needed fiscal adjustment reforms, triggered a run on the currency in April 2018 and drove the economy into recession again.

Although Macri’s administration improved the macroeconomic fundamentals and corrected the imbalances and relative price distortions of the Argentine economy, the results were not felt by the average citizen by 2019. Inflation was still high, around 50 percent, and the economy had been in recession in three out of the four years Macri held office. In the 2019 elections Kirchnerism came back to power. This time former president Cristina Fernández de Kirchner was vice president and Alberto Fernández the president. The new government rolled back most of the economic reforms introduced to favor free and competitive markets, and attempted to curtail the independence of the judicial system. Strong opposition from Juntos por el Cambio (formerly Cambiemos) in Congress prevented this from happening. On the macroeconomic front the situation worsened significantly. Argentina’s response to the COVID-19 pandemic, like that of many other countries, included a sharp increase in the fiscal deficit and lax monetary policy. However, contrary to what happened in the rest of the world, this policy stance was reversed only very slowly once the pandemic ended. Besides, a new debt restructuring in 2020 meant that Argentina lost access to international credit markets, so the large fiscal deficit was financed with a combination of domestic debt and money creation. Capital controls and import restrictions were reintroduced, making access to Forex for firms and individuals a Kafkaesque experience. Both freedom and prosperity have suffered. After recovering from the pandemic, the economy fell back into a recession in the fourth quarter of 2022, and a new drought made things worse. The economy is expected to contract by 2 percent in 2023, the Central Bank has exhausted its international reserves, and inflation is expected to reach 210 percent in 2023. The overall Freedom Index again captures well the events of the last four years.

The sustained decrease in the political freedom subindex, starting in the early 2000s, can be explained by the fact that the Peronist governments of the Kirchners also benefited from a majority in Congress. Between 2002 and 2015, Congress imposed no real restrictions on the executive, hence the very low score on this indicator. Instead, congressional constraints became very relevant for President Macri, because with a minority in Congress, it was hard to pass the legal reforms that his government sought. The fall in civil liberties since 2014 is probably capturing the social unrest of the time, but it is somewhat erratic, so probably it is also influenced by perceptions generated by very extraordinary events, such as the murder of Alberto Nisman, an attorney who had been leading the prosecution of government officials.

Regarding legal freedom, it seems that the component of bureaucracy and corruption captured well the changes in government, and the different approaches to public service. The score worsens in the 2003–15 years, improves slightly during the President Macri years, and again falls with the current government. A similar pattern is clear in the judicial independence indicator.

Overall, the graph of the Freedom Index shows very clearly the changes in economic and institutional policies that the Macri administration tried to implement, but also shows that many of those policies have been short lived.

From freedom to prosperity

The overall trend of the Prosperity Index generally resembles the evolution of income in the country. In the first decade of the century, the country grew thanks to very favorable external conditions (low global interest rates and high commodity prices). The effect of these conditions on growth became stronger as government spending also increased and monetary policy was lax. However, this policy mix proved to be unsustainable and the economy has more or less stagnated since 2011. On the contrary, sustainable economic policies usually involve short-term costs, and require time to exert their positive effects on the economy, but their fruits last longer.

The inequality indicator improved during the first decade of this century as growth and higher public spending reduced poverty. Of course, as argued above, the problem was the unsustainability of the policy mix. As expected, the situation has worsened since 2018, with the economic crisis and then the pandemic. Since 2021, the significant increase in inflation has increased poverty markedly.

The evolution of the health and education indicators clearly reflects the overall economic performance of the country. In emerging economies, growth tends to correlate very highly with other social outcomes. Among all Latin American countries for the last thirty years, the worst economic performer has been Venezuela, but Argentina follows closely behind. This poor evolution of GDP affects other measures, such as health. Moreover, while other countries in the region used the windfall of resources of the early 2000s to build a more resilient and sustainable economy, balance the budget, and control inflation, Argentina did just the opposite. The populist government increased government spending significantly, and did not invest in projects with high long-term social or economic returns in the areas of health or education. This is why Argentina now has the same GDP per capita that it had fifteen years ago.

Aside from a small increase in 2016, the environment indicator has remained virtually flat for the past twenty years. Around 2016 the government attempted to alter the country’s energy mix in favor of renewable energies, but the effect was negligible.

Finally, although the education indicator shows that Argentina has improved more rapidly than the regional average, PISA1PISA is the OECD’s Programme for International Student Assessment. PISA measures 15-year-olds’ ability to use their reading, mathematics, and science knowledge and skills to meet real-life challenge scores for Argentina actually show a deterioration of the country’s educational system. This contradiction might be the result of the methodology used to build the Index. The indicator included in the Prosperity Index only measures average years of education, and this trend may have improved. But the quality of the educational system is most likely worsening, which again may hamper future economic growth.

The future ahead

At the time of writing this commentary, Argentina has just held the runoff of the 2023 presidential elections. In a surprising outcome, Javier Milei, a libertarian economist turned politician just four years ago, has been elected with a clear 11 percentage point gap over Sergio Massa, current finance minister of the incumbent Peronist government.

Milei’s election largely reflects the frustration that Argentines feel with the state of the economy. Kirchnerism dominated Argentine politics for sixteen of the last twenty years and the economic results have been disastrous for the country. The Macri administration (2015–19) corrected the fundamental macroeconomic imbalances, but could not generate positive results in terms of growth and inflation. Furthermore, the economic situation has worsened in the last four years. Monthly inflation in November 2023 was 12.8 percent, which implies an annualized rate of more than 300 percent, and in December monthly inflation was expected to be well above 20 percent. To put this in context, Argentina is experiencing each week the level of inflation that most countries would see in a year. Hand in hand with inflation, the poverty rate is now close to 42 percent of the population and the economy is in a recession.

Milei’s campaign slogans can be basically summarized in four words: freedom, caste, chainsaw, and dollarization. The reference to freedom seems a reaction to the restrictions imposed during the COVID-19 pandemic, which were particularly stringent in Argentina. The calls to remove the political “caste” are similar to those made by populist leaders in other countries, as a generalized way of blaming the country’s problems on the political elites. The metaphor of the chainsaw was used by Milei to illustrate his aim to severely cut public spending. And finally, he proposed dollarization and the closure of the Central Bank of Argentina as a solution to the unbearable levels of inflation. This strategy allowed Milei to channel people’s anger with the economic situation.

Like other political outsiders around the world, Milei has accurately identified many of the country’s real problems (inflation, high and inefficient public spending, political capture, corruption, and so on), and has suggested who should be blamed and a series of easy solutions. And the Argentinian people have voted for this project. Nonetheless, just ten days after the elections, it was obvious that the solution is not going to be that easy, and Milei had already walked back on some of his positions. Dollarization was the first to go, as there are just not enough dollars in the Argentinian Central Bank to dollarize the economy, at least in the short run. To some degree, he is also walking back on the issue of the political caste, as he lacks an effective team of his own, forcing him to rely heavily on former officials of Juntos por el Cambio (Macri’s coalition) and the moderate wing of the Peronist party to advise and form his government. Moreover, Milei’s party, La Libertad Avanza, is in a weak position in Congress so he will need to build consensus with the traditional parties in order to pass legislation. Overall, it seems that Milei will be forced by the internal and external situation to moderate his plans.

The litmus test of Milei’s administration in the coming months will be the macroeconomic situation, which is extremely delicate. Argentina is on the verge of hyperinflation. To make things even worse, some of the reforms needed to rebuild the international reserves of the Central Bank and correct the fiscal imbalances, like a devaluation of the official exchange rate and an increase in utility prices, will actually generate a rise in prices in the short run. Milei will only be successful if he can swiftly reduce the fiscal deficit, make a credible commitment that the Central Bank will stop printing money to finance the Treasury, and reset people’s inflation expectations. A stabilization plan will be needed to achieve these difficult tasks.

If Milei manages to stabilize the macroeconomic situation without going through a major crisis and introduce some market-friendly reforms in Argentina’s overregulated economy, he could be a very successful president. This is because some fundamental positive forces and opportunities still exist for Argentina, giving hope that the sustained economic growth of the past can be recovered. The country is rich in some natural resources that have become increasingly valued in world markets and that are yet to be exploited: The Vaca Muerta region contains one of the largest nonconventional reserves of oil and gas in the world. There are large amounts of lithium in the north of the country. And there are mining opportunities in the mountains, to name a few. If Milei manages to handle the macroeconomic situation, the potential for growth is significant.

Besides the economic front, it seems unlikely that Milei’s more extreme positions on social issues and civil liberties will ever be approved by Congress. Although some people have voiced concerns regarding a potential authoritarian vein among Milei and his followers, so far he has been respectful of the democratic process and institutions. It is worth noting that, unlike Jair Bolsonaro and other populist leaders who have been elected elsewhere, Milei does not have a military background. In addition, his weakness in Congress makes it extremely unlikely that he could pass any measures that may weaken the democratic order. Although he may try to govern by issuing executive orders, there is an established process to be followed and Congress can always reject the orders. The initially painful effects of the necessary economic policy changes may encourage Milei to move the political focus to social and cultural issues, and it is not clear how the Argentinian people would respond to such a shift. But, right now, the crucial challenge that he faces is fundamentally economic.

Guido Sandleris is a professor of international economics at Johns Hopkins University School of Advanced International Studies (Europe) and at Universidad Torcuato Di Tella (Argentina). Between September 2018 and December 2019, he was governor of the Central Bank of Argentina. In 2017 he became chief economic adviser and in 2018 secretary of economic policy at the Ministry of the Treasury of Argentina.

EXPLORE THE DATA

Image: Commuters walk trough ticket machines at Constitucion train station, amid a rise in cases of the coronavirus disease (COVID-19), in Buenos Aires, Argentina April 8, 2021. REUTERS/Agustin Marcarian