China Pathfinder: Q1 2024 update

In March 2024, China’s Premier Li Qiang capped off a bumpy first quarter by cancelling a traditional annual press conference to talk about the government’s plans for the coming year. But in many ways, China’s policy measures spoke for themselves. The year-to-date story has been one of harried effort to support a faltering stock market, ramp up exports to make up for domestic demand, and double-down on high-tech sectors with subsidies and other innovation funding. The most important policy document of China’s economic year, the Government Work Report, promised state guidance and fiscal expansion but did not address the structural problems that have impaired Beijing from doing that in the past several years.

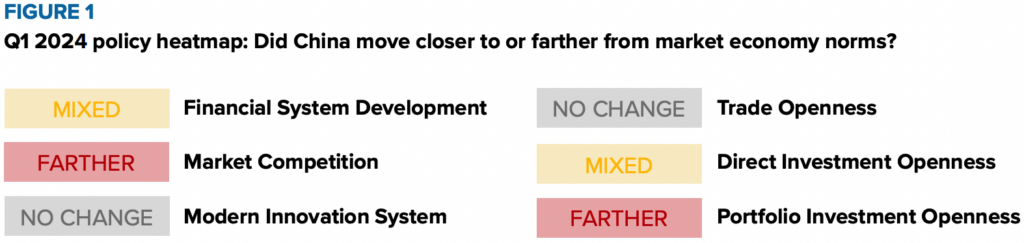

We identify some positive policy developments compatible with global market norms this quarter, including in financial system development and direct investment openness. New data security guidelines provided some reassurance to skittish foreign investors after years of uncertainty on the scope of data rules. Beijing pledged once again to ease the business environment and level the competitive playing field for foreign firms, this time through twenty-four measures and a charm offensive with foreign CEOs at the China Development Forum. And despite uncertainty, foreign portfolio investors took advantage of premium China bond returns, even as direct investment stalled.

These policy strategies were mostly familiar. In most of the areas monitored under the Pathfinder framework, there was either no market convergence or active backsliding. There was little to no public discussion of the structural and systemic factors weighing on the economic outlook, low productivity, foreign concerns over overcapacity or exchange rate risks. This paucity of needed debate fanned the flame of discussions in G7 capitals about the need to coordinate collective trade defense. While a few signs of the end of the property correction are showing up, suggesting a cyclical stabilization with the next several quarters, the longer-term headwinds to sustainable growth will mount until meaningful market reforms are implemented.

Source: China Pathfinder. A “mixed” evaluation means the cluster has seen significant policies that indicate movement closer to and farther from market economy norms. A “no change” evaluation means the cluster has not seen any policies that significantly impact China’s overall movement with respect to market economy norms. For a closer breakdown of each cluster, visit https://chinapathfinder.org/

Read the full issue brief below

Presented by

At the intersection of economics, finance, and foreign policy, the GeoEconomics Center is a translation hub with the goal of helping shape a better global economic future.