An energy and sustainability road map for the Middle East

table of contents

- Introduction

- Executive summary and policy recommendations

- An energy-driven foreign policy

- Specific initiatives, projects, and proposals

- COP28, COP29, and beyond

- Conclusion

An extended edition of this report, including additional resources and background information, was released in February 2025 and is available via PDF.

Introduction

Global warming is impacting the Middle East at more than twice the global average. In a region already beset by territorial and religious conflicts, this is alarming: Beyond the immediate human suffering from war, the region’s people face severe consequences of global warming. While it is uncertain if humanity can entirely avert this crisis, it is clear that mitigation and adaptation measures are essential to address its worst effects. Climate change respects no borders; for instance, nature does not distinguish between Areas A, B, and C in the West Bank, nor does it differentiate between the rising sea levels along the shores of Tel Aviv and Beirut. Cross-border cooperation will be critical to implementing effective mitigation and adaptation measures. As temperatures rise and extreme weather events, such as intense but infrequent rainfall, become more common, countries in the region must work together to optimize and expand sustainable energy and water resources.

This report was partially written prior to the October 7, 2023, attack by Hamas on Israel, which triggered the ongoing Gaza war. Beyond the physical reconstruction required in Israel and the Gaza Strip, the traumas on both sides of the border could take decades to heal. Now, with the death of Hamas leader Yahya Sinwar and Hezbollah leader Hassan Nasrallah, the region has a rare opportunity for rebuilding and peace. On the Israeli side, it is clear that new Israeli leadership will be critical for rebuilding and unifying the country, as well as for mending relations with the Palestinians and the wider region. Saudi Arabia has indicated it would need to see a clear path for an independent Palestinian state for normalization of its relationship with Israel to proceed. Other regional powers, such as the United Arab Emirates, Egypt, Jordan, and Bahrain, have cooled relations with Israeli Prime Minister Benjamin Netanyahu’s government.

For there to be a realistic possibility of building on the Abraham Accords—or even taking small steps to increase cooperation in the region—a “New Middle Eastern Order” will need to be established. A comprehensive new US plan could shape this new order.

The United States, seen by some in the region as disengaging, now has an opportunity to counter that perception by helping to establish a “New Middle Eastern Order” based on a tangible plan for strong intra-regional energy and climate-related cooperation, alongside efforts to facilitate a permanent solution to the Israeli-Palestinian conflict. For example, the energy and climate component could form a cornerstone of the US strategy for the region. The alternative is a region increasingly mired in conflict due to dwindling resources in the face of a worsening climate crisis and a deepening of existing conflicts fueled by a destructive Iranian agenda. Furthermore, this alternative risks exacerbating global conflict-driven emissions and environmental disasters, as seen recently with the Houthi attacks in the Red Sea.

Although tangible cooperation on energy- and climate-related issues has so far been limited, this can—and indeed must—change. The purpose of this piece is to highlight some specific areas where cooperation can be undertaken and advanced under the task force platform outlined below.1The piece focuses on five countries—Egypt, Israel, Jordan, Lebanon, and Saudi Arabia—and the Palestinian territories. More countries and water resources, for example, can be analyzed in the future.

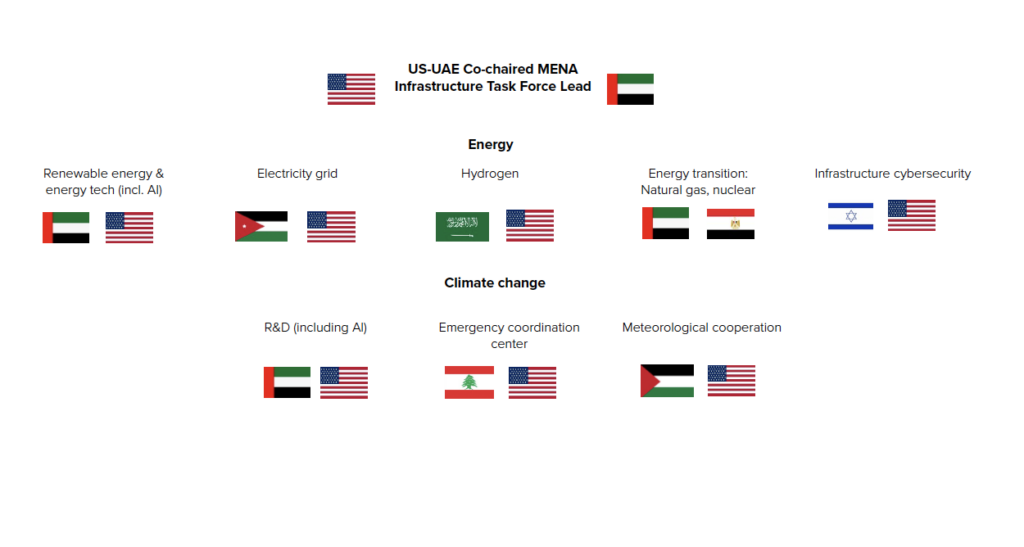

Figure 1: Proposed structure of the task force platform

This piece was written following meetings and interviews conducted in the region to gather input from public and some private sector stakeholders on the proposals being suggested.

Executive summary and policy recommendations

The Middle East and North Africa (MENA) region is facing a severe crisis due to climate change.

A “New Middle Eastern Order” can and should be shaped by the United States and its regional allies to enable the critical cooperation mentioned below. This approach could build on the energy diplomacy seen in the region before October 7, 2023, while recognizing the need for a viable path toward resolving the Israeli-Palestinian conflict. Similarly, the United States should continue to make an effort to address the Israel-Lebanon conflict, and, though less urgent, should work on the Turkey-Greece-Cyprus issue to reduce Eastern Mediterranean tensions and foster stronger energy cooperation, including with Turkey. This is a tall order, but the alternatives are bleak.

- The MENA region will face increasing climate-derived conflicts unless countries in the region work together to adapt and mitigate the impacts. There are “low-hanging fruit” opportunities where such cooperation can begin immediately, such as direct meteorological collaboration.

- Regional groupings, both new and old (e.g., the East Mediterranean Gas Forum or the proposed reformed East Mediterranean + Energy Forum), can play a helpful role in this regard and become part of the formal mechanisms noted below if beneficial.

- Climate change is increasingly becoming a national security issue. States need to consider infrastructure and climate change security at the same level as traditional security alliances, assessing which alliances best serve their climate and energy security concerns.

- To this end, it is proposed to establish formal mechanisms to ensure cooperation across borders in combating climate change and supplying energy throughout the region.3Similar task forces could be established for water, telecommunications, and other sectors. Such a mechanism must be resilient against internal chaos (as we are seeing in Israel and Lebanon) as well as cross-border conflicts and political tensions. Moreover, it should withstand changes in government, including in the United States. Specifically, it is proposed that the United States and the United Arab Emirates (UAE) launch a set of formal energy and climate task forces, ideally structured in a manner that can endure governmental changes in the United States or the Middle East.

- The overall task force platform could be co-chaired by the United States and the UAE, as proposed. The UAE would be an ideal choice for this role, should it be interested, considering its leadership in energy transition matters both regionally and globally, as well as its universal acceptability as an important broker in the region.

- The overall task force platform is proposed to include specific topic task forces co-chaired by relevant countries and the United States. An alternative would be for the United States and the UAE to split co-chairing responsibilities among various topic task forces or to involve other players, such as the European Union.

- For example, the UAE and the United States could co-chair the renewable energy/energy tech task force (including carbon capture, utilization, and storage and battery storage), while Saudi Arabia and the United States could co-chair the hydrogen task force, Jordan and the United States could co-chair the electricity grid task force, and Egypt and the UAE could co-chair the energy transition task force. Members should include energy and climate experts from the region, as well as representatives from the private sector and financial institutions, both private and governmental.

- The task force would be a nonpolitical gathering aimed solely at cross-border initiation planning and implementation of projects and initiatives, with key examples outlined in this paper.4See Figures 2 and 3 for details. Task force members would regularly report to the lead (e.g., US-UAE) on the status of cross-border projects and cooperation. The United States could also involve other countries, financial institutions, and the private sector to finance these initiatives. New projects and initiatives could build on existing projects as well as on existing agreements and initiatives. The task forces would not be the end goal; rather, the underlying projects and initiatives would be. Moreover, it is essential that the vision for this setup does not distract from or interfere with ongoing projects, initiatives, or institutions but instead seeks to build and expand upon them to encourage and facilitate additional successful endeavors.

An energy-driven foreign policy

In today’s policy landscape, countries increasingly use energy as a key tool in diplomacy to achieve specific goals, such as boosting energy independence or strengthening regional influence. When channeled effectively, this approach can help address shared energy and climate change challenges.

A notable example of this approach can be seen in the Arab Gulf countries, which are seeking to diversify gradually from hydrocarbons and exploring cleaner energy alternatives. In the United Arab Emirates, the state-owned renewable energy company Masdar is leading this transition, as will be further elaborated below. Saudi Arabia’s Vision 2030, with Neom—a futuristic, high-tech, and sustainable megacity project—as its centerpiece, further exemplifies this shift.5It is worth noting, however, that the project has been scaled back somewhat due to the Public Investment Fund being more cash-strapped than before, and timeline extensions are now seen as more realistic. For more on this, see Zainab Fattah and Matthew Martin, “Saudis Scale Back Ambition for $1.5 Trillion Desert Project Neom,” Bloomberg, April 5, 2024, https://www.bloomberg.com/news/articles/2024-04-05/saudis-scale-back-ambition-for-1-5-trillion-desert-project-neom.These moves are reshaping the intra-regional political landscape as hydrocarbon-importing Middle East and North Africa (MENA) countries such as Morocco diversify their energy sources with the goal of generating 50 percent of their electricity from renewables by 2030. This reduces their reliance on hydrocarbon-exporting neighbors and positions them as clean energy exporters.

Other examples include Egypt, which aspires to become a hydrogen hub through Port Said, and Jordan, which is planning for small modular nuclear reactors (SMRs) and expanding renewable energy such as solar power to reduce liquefied natural gas (LNG) imports from Qatar and oil from Saudi Arabia.

We are witnessing a surge in energy diplomacy at the forefront of state diplomacy in the wider region. Masdar City, in the UAE, has long been viewed as a model for future green cities. For instance, its architecture includes wind-directional buildings that help reduce the city’s temperature. According to Masdar:

“Each building in Masdar City is constructed with low-carbon cement, utilizes aluminum that is 90 percent drawn from recycled sources, and is designed to reduce energy and water consumption by at least 40 percent than that of the average building in Abu Dhabi.”

The temperature in the streets of Masdar City is generally up to 20 degrees Celsius cooler than in the surrounding desert. This temperature difference was achieved through a design that includes a wind tower, which captures air from above and circulates a cool breeze through the streets. Additionally, the city’s elevated site creates a cooling effect. According to Foster & Partners:

“The [Masdar] Institute’s residences and laboratories are oriented to shade both the adjacent buildings and the pedestrian streets below and the facades are also self-shading.”

Masdar City is also powered by a nearby solar photovoltaic (PV) plant and hosts the headquarters of the International Renewable Energy Agency (IRENA). Initially known for Masdar City and its local solar PV projects, Masdar has since grown into a key player in the global renewable energy market, acquiring technologies—such as its recent acquisition of storage technology—and undertaking projects worldwide, from the UAE to North America and Australia. Recent projects include a Masdar-led consortium to develop 4 GW of hydrogen in Egypt. Masdar has become a key diplomatic tool for the UAE government.

Recently, we have seen how Russia has used energy—specifically natural gas—as a diplomatic weapon against Europe. The Russian state-owned energy giant Gazprom also attempted to gain a foothold in Israel’s largest gas field but failed—due to Israeli national security concerns—despite the traditionally warm relations between Israeli Prime Minister Benjamin Netanyahu and Russian President Vladimir Putin. Nevertheless, Russia succeeded in investing in gas fields in both Lebanon and Egypt.6Although, as Robin Mills, a nonresident fellow at the Center on Global Energy Policy at Columbia University’s School of International and Public Affairs, points out, Russia eventually withdrew from the Lebanese fields.

Qatar has also added energy to its arsenal of diplomatic ambitions. Having committed to funding the Gas for Gaza (G4G) project, Qatar is increasingly active in gas geopolitics, with interests in the Qana gas field in Lebanon—following the 2022 Lebanese-Israeli maritime agreement—and Cyprus.

Meanwhile, the UAE’s Mubadala has invested in gas fields in Israel and Egypt. However, the increased instability in Israel and the ongoing Gaza conflict appear to have influenced Abu Dhabi National Oil Company (ADNOC), another major UAE entity, to freeze further negotiations on acquiring a stake in the Leviathan gas field.

Saudi Arabia has positioned Neom, as outlined in Vision 2030, as a central feature of its foreign policy, aiming to transform the country into a clean energy hub, including hydrogen and electricity generated from renewable sources (see more below). This would enable Saudi Arabia to export clean energy to the region and beyond.

Beyond the region, it is important to consider the role China is playing in the realm of energy diplomacy.

According to a November 2022 Credit Suisse report seen by the author:

“While the ongoing energy crisis may eventually accelerate the transition to renewables, renewable supply chains will have to be diversified to reduce dependencies (e.g., China’s share in key manufacturing stages of solar panels exceeds 80%) . . .”

China, while a massive consumer of Middle Eastern hydrocarbons (nearly half of its imports are from the region), is continuing to make inroads into the MENA region as it seeks to expand its energy and other infrastructure foothold. In addition to its critical role in the renewable energy sector—especially the solar PV supply chain—China has been a major investor in nuclear energy projects in the region. This increased engagement has been evident through the Belt and Road Initiative, which aims to improve connectivity between China and other countries on a transcontinental scale. Similarly, the Sino-Arab Summit held in Riyadh at the end of 2022 underscored this commitment. Major themes of the summit included:

“Energy security, nuclear and new energy [which] were the top issues of the meeting. The summit also underlined the food crisis and climate change.”

According to the US House Foreign Affairs Committee:

“From 2005 and 2022, the PRC invested over $126 billion in the MENAT [MENA plus Turkey] energy sector.

“Energy accounts for 46% of PRC investment in the region.”

Whether China and the United States will clash over increasingly dominant energy policies in the region remains to be seen. One thing is for sure: we will have a greater chance of mitigating the impacts of climate change by working together, and the Middle East is no exception in that regard.

Regional groupings

There have also been attempts to address regional energy- and climate-related issues through regional groupings. Countries in the region are not waiting for external powers; instead, they are forming alliances and regrouping—see the new BRICS membership and the Saudi-Iran rapprochement, for example. It is important to consider the merits of institutional cross-border cooperation by examining existing or proposed platforms for dealing with energy supply (e.g., a reformed East Mediterranean Gas Forum (EMGF) that includes more members and clean energy—see more below).

Additionally, forums for tackling climate change (such as the author’s proposed regional Levant-North African Environmental Forum, the Cypriot initiative, etc.) should be considered and/or strengthened. The Negev Forum working group platforms could be resumed to help address both energy supply challenges and the potential for environmental cooperation in light of climate change, especially if relations between the N7 countries—Bahrain, Egypt, Israel, Jordan, Morocco, Sudan, and the UAE—improve following an eventual change in Israel’s government and its policies in the region.

Israeli President Isaac Herzog introduced a “renewable Middle East” plan for countries of the region to cooperate on climate change. Additional initiatives include MENA2050, which established the Climate Action Committee to tackle shared climate change challenges in the region. The committee includes experts such as former ministers of environment and former United Nations Conference of the Parties (COP) secretaries-general. Organizations like EcoPeace have made impressive strides in recent years by capturing the attention of senior decision-makers and demonstrating their ability to implement projects on the ground.

Before the attack by Hamas on Israel on October 7, 2023, which triggered the ongoing conflict, Israel and various Arab states, including Lebanon, Iraq, and the Palestinian territories, attended a regional climate change meeting organized by the Egyptian government at the COP27 summit in November 2022 to promote cooperation in addressing climate change. Every such initiative can play an important role in fostering enhanced cross-border cooperation on mitigation and adaptation measures, and projects aimed at tackling climate change and promoting clean energy in the region.

The EMGF was established to convene the Eastern Mediterranean’s main gas producers and consumers. The forum consists of Egypt, Cyprus, Israel, Jordan, and the Palestinian territories, as well as France, Greece, and Italy, with the United States, the European Union (EU), and the World Bank as observers, and its secretariat is based in Cairo. The EMGF has proven successful in bringing together some regional actors that are in conflict, such as Israel and the Palestinian territories, to discuss gas cooperation in the region constructively.

It is worth noting that the Palestinians possess the Gaza Marine gas field, with plans to develop and export gas to Egypt as well as consume it locally. There are also projects to connect Gaza and the West Bank to Israel’s natural gas system. However, for the EMGF to survive and flourish, it will need to adapt. It must focus on how the MENA region can work together on the energy transition. While natural gas is undoubtedly part of this, it is necessary to broaden the mandate to include clean energy and consider how the interconnecting gas pipelines in the region can eventually transport hydrogen. This author and others have called for a name change from EMGF to East Mediterranean + Energy Forum (EMEF+) to account for other forms of energy besides gas. Additionally, it will be necessary to consider adding more members, such as Turkey and Lebanon. With the Lebanese-Israeli maritime deal having been reached, it makes sense for Lebanon to join, not least to foster energy cooperation across conflictual borders. However, this can only happen once further escalation in the wake of the wars in Gaza and Lebanon is avoided.

Future issues that arise between Israel and Lebanon concerning the Qana field may require a unitization agreement in general. While the Lebanese-Israeli maritime deal includes assurances and a role for the United States in settling issues between the countries that do not have diplomatic relations, it is important for the parties to meet in a larger forum. Similarly, finding a way to integrate Turkey into the EMEF+ would be an important step in resolving outstanding disputes between Turkey, Greece, and Cyprus in the Eastern Mediterranean.

The settlement of these disputes will be critical for fruitful cooperation in the Eastern Mediterranean. Just as the US government successfully mediated the Lebanese-Israeli maritime border (and hopefully will succeed in efforts for a permanent land border agreement), it will be crucial for the US government to now focus on resolving these issues. Discussions on additional gas pipelines from the Levant to Europe or enhanced electricity connectivity should include Turkey. Ultimately, the Euro-Asia connector may proceed as planned, connecting the Levant to Europe via Cyprus and Greece, but it is important to include Turkey to avoid it becoming a spoiler.

The EMEF+ could also play a significant role in driving forward and coordinating mitigation and adaptation efforts regarding climate change, with similar impacts for the Eastern Mediterranean countries.

Landon Derentz, senior director of the Atlantic Council’s Global Energy Center and a former US executive board member to the EMGF, notes that some senior Western officials are already promoting this concept within their own governments. “There is an appreciation in many EMGF capitals that replicating the level of coordination realized through cooperation on gas markets will elevate the ability of Eastern Mediterranean countries to accelerate aspects of the energy transition while safeguarding regional energy and economic security,” said Derentz.

The role of the UAE in the reformed EMGF, or the EMEF+, should also be considered. At the very least, the UAE could join as an observer alongside the US government, the EU, and the World Bank. Ideally, the UAE would join as a full member. With the UAE positioning itself as a regional, indeed global, leader in the energy transition, with Masdar and Abu Dhabi-based IRENA spearheading these efforts—especially with the UAE presidency of COP28—it is important to consider how the UAE can play a central role in the EMEF+. This could take the form of a joint secretariat, with alternating meetings between Cairo and Abu Dhabi, for instance, where gas meetings take place in Cairo, and renewable energy meetings occur in Abu Dhabi—or some other form of collaboration.

“Efforts by the United States, India, the UAE, and Europe to establish an economic corridor from Mumbai to Berlin are anchored in a strategy to connect the Arabian Gulf to the Mediterranean, including through the UAE, Israel, and the Palestinian territories,” said Derentz. The UAE’s membership in the EMGF could build upon these diplomatic efforts launched during the Group of Twenty meeting in India in September 2023 and further facilitate shared economic opportunity for all parties in the region. This argument contends that such a corridor has increased urgency to mitigate the risk of reliance solely on export via the Suez Canal following the Houthi attacks in the Red Sea.

Specific initiatives, projects, and proposals

It is worth turning now to specific proposals in various realms. This section will examine projects—planned, underway, or proposed—in the energy sphere. In this regard, the role of the private sector will also be discussed, focusing on specific initiatives and projects in which it plays a role, both present and future.

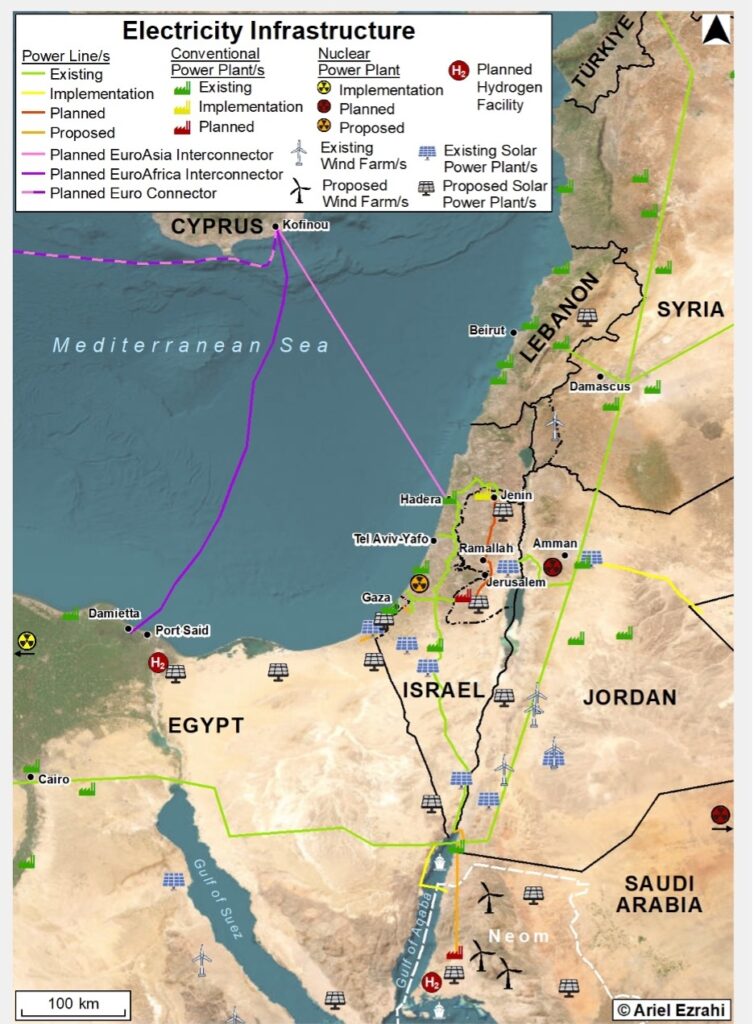

Figure 2. Electricity infrastructure in the Middle East

Figure 3. Gas infrastructure in the Middle East

Hydrogen

Saudi Arabia is planning the world’s largest utility-scale green hydrogen project, with commissioning planned for 2026. The initial production will include 600 tons of clean hydrogen daily and 1.2 million tons of green ammonia per year. According to senior Neom officials, the hydrogen produced in Neom is primarily intended to be transported as ammonia by ship to global markets. This transport will likely occur via ships traveling from the Red Sea through the Suez Canal, reaching the rest of the world, or via pipeline to Egypt and then to global markets via Egyptian ports. According to Neom’s website, the project will mitigate the impact of 5 million metric tons of carbon emissions per year.

Ammonia could also be exported from Neom to Jordan by land in trucks, then transported northward from Jordan to Lebanon, Syria, Iraq, and Turkey. From Jordan, it could also be transported overland to Israel, reaching the Mediterranean coast, Europe, and the rest of the world. Saudi Arabia could also export ammonia directly by ship to the southern Israeli port city of Eilat, from where it could be transported to the Mediterranean coast (see Figure 3).

Saudi Arabia could also export to neighboring countries via rail and pipelines if there is a domestic market for hydrogen or ammonia in the MENA region. For example, hydrogen pipelines could run from Saudi Arabia westward to Jordan and from there to Syria, Lebanon, and Israel. Given the recent Houthi attacks from Yemen, this additional export route has gained relevance due to risks associated with relying solely on the Red Sea. Pipelines could also be routed eastward from Saudi Arabia to the Arab Gulf countries.

For a viable market for hydrogen, the price would need to be competitive with other fuels, either through production cost reductions or government incentives (as is currently the case in the EU and the United States, for example). If a rail system throughout the Middle East were to be reestablished—potentially building on the old Ottoman railway network—ammonia could also be transported by rail.

The case for a hydrogen pipeline network will depend on the development of a MENA hydrogen market. According to a senior businessman from the region, until incentives are introduced in the region to make hydrogen competitive, much of the production will be deemed for export to Europe and elsewhere, where incentives are already in place. That said, national governments in the region do have plans for domestic consumption, so it will be important to monitor the implementation of these planned incentives.

At COP27, Egypt took meaningful steps to address some of the abovementioned challenges. A Regional Center for Renewable Energy and Energy Efficiency (RECREE) official emphasized that at COP27, eight hydrogen memorandums of understanding (MoUs) were signed with Egypt alone, reflecting Egypt’s aim to become a regional hydrogen hub. These MoUs included plans for an eight billion dollar hydrogen plant in the Suez Economic Zone (SCEZ). Masdar is also planning a mega hydrogen project in the SCEZ.

According to the Moroccan national road map on green hydrogen:

“By 2030, [Morocco] envisages a local hydrogen market of 4 terawatt hours (TWh) and an export market of 10 TWh, which, taken together, would require the construction of 6 GW of new renewable capacity.”

Further east in the region, Oman is set to become a major hydrogen producer by 2030 and the UAE has its own major plans as well in this regard. Israel and Jordan also have their own, more modest plans for producing hydrogen, which—considering their relatively small markets, geographic proximity, and existing pipeline infrastructure—could likely form the basis of cooperation in this field between the two countries.

Renewable energy

The Middle East has been blessed with many advantages, one of which is optimal solar irradiance for generating clean electricity. In some parts of the region, land is abundant for hosting large-scale solar farms. In Neom, for example, Saudi Arabia plans to generate around 4 GW of electricity from renewable energy (wind and solar PV), with 3 GW allocated to meet the energy needs of the hydrogen plant.

In other parts of the region where land is less abundant, resource swaps are being considered. For instance, at COP27, the UAE, Jordan, and Israel signed a water-energy swap deal. Project Prosperity involves building a 600 MW solar PV plant in Jordan, with the generated electricity transmitted to Israel in exchange for desalinated water. Masdar is developing this project. Project Prosperity is a significant example of the importance of cross-border cooperation in the region, providing clear benefits to all participants. The project has a climate rationale, as well as energy, water security, and economic motivations.

Jordan will need to continue implementing major utility projects within the kingdom to reach its target of 3 GW by 2030. Although the war that followed the attacks on Israel by Hamas on October 7, 2023, and the heightened regional tensions have put this and other important cross-border projects involving Israel on hold, once the conflict subsides, it will be critical to resume such initiatives.

Much more can and should be done to advance renewable energy in the region. In Egypt, for example, there are multiple plans for utility-scale solar PV projects. At COP27, renewable energy deals for projects throughout Egypt, including solar PV, were signed, amounting to investments valued at billions of dollars. While these efforts are a step in the right direction, one area repeatedly discussed but still lagging is solar development in the Sinai Peninsula (see Figure 2). Such projects would not only serve Egyptian communities but could also provide electricity to Gaza and beyond.

Egyptian officials, however, have cited security concerns in the Sinai as a barrier, explaining that these issues need to be resolved before major economic initiatives can proceed. With Egypt now leading international efforts to develop the Gaza Marine gas field, this could be an opportune moment to establish Sinai as a solar PV hub. As the region and the world begin to consider a “day after” plan for Gaza, there is a growing need to support reconstruction and meet urgent energy needs. The potential is enormous, and the electricity generated could benefit both Egyptians and neighboring communities. Egypt could leverage international political and financial support for renewable energy projects to transform Sinai fundamentally. Perhaps, with such significant economic and international interest, Egypt’s security concerns might be alleviated. A small but meaningful step in this direction was the 25 MW of renewable energy made available by new local projects to COP27 hosted in Sharm el-Sheikh, in 2022.

In Gaza, while the potential for solar PV is limited, the analysis undertaken by the international community has shown that some utility-scale solar PV projects could be feasible in the buffer zone (also known as the Access Restricted Area) and other locations, which could help alleviate the electricity shortage in the area to some extent. In the West Bank, however, the potential for solar PV is much greater; the World Bank has estimated some 3,000 MW of installed capacity is feasible.

Due to political challenges, especially concerning projects in Area C in the West Bank, major utility-scale projects have stalled. This author has in the past suggested to various international governments a potential solution to overcome some of these political obstacles: the creation of Designated Renewable Energy Zones (see Figure 2). These zones would consist of several locations throughout the West Bank where a fast-track permitting system would be implemented. Within these zones, coordination among Palestinians, Israelis, and international developers would be streamlined to enable rapid project implementation. Keeping politics out of these zones (i.e., avoiding any political designations) while focusing on the practicality and bankability of such projects would be key to success.

US leadership would be essential for such an initiative to succeed. An international developer would also be required to work closely with the Americans, Palestinians, and Israelis. Other financial institutions, such as the European Investment Bank (EIB) and the European Bank for Reconstruction and Development (EBRD), have expressed interest in developing solar PV in the West Bank and have local representatives actively promoting such initiatives.

Of course, to realize such projects in Gaza and the West Bank, it will be necessary to have in place the right local leaderships coupled with support and initiative from external actors, particularly following the Israel-Hamas war and its aftermath.

Egypt aims for 42 percent of its energy to come from renewable sources by 2035. It has already achieved impressive progress, with no less than 6,100 MW of installed renewable energy electricity capacity, comprising 50 percent hydropower and 50 percent solar and wind. Additionally, Egypt is working to incentivize private investment in renewable energy. A RECREE official cited the Benban Solar Park in Aswan as an example, which has a capacity of 1,650 MW.

Lebanon has made significant strides in constructing solar PV facilities, particularly since the reliability of its electricity grid has been questioned due to the ongoing electricity crisis.

Israel will also need to ramp up its solar PV utility-scale initiatives if it is to meet its renewable energy targets. The main potential lies in the Negev Desert (see Figure 2), which could also serve Palestinian energy needs, especially in Gaza (as the West Bank has its own untapped potential).

Electricity grids

The MENA region has three separate electricity grid blocks:

- The Gulf Cooperation Council (GCC) block

- The Mashreq block (Egypt, Iraq, Jordan, Lebanon, Libya, the Palestinian territories, Syria, and Turkey)

- The Maghreb block (Algeria, Libya, Mauritania, Morocco, and Tunisia)

The three grids are not connected, although some members of the Mashreq block overlap with certain Maghreb block countries. The GCC grid has proven reliable, albeit primarily for emergency and peak scenarios. The Maghreb grid has been a relatively effective means of transferring electricity between member countries. In contrast, the Mashreq block has been the least successful, though certain elements have proven useful (e.g., the upgrade between Jordan and the West Bank a couple of years ago).

It is critical to prioritize the interconnection of these grids for the following reasons:

- As the countries in the region increase their renewable energy capacity, upgrading and interconnecting electricity grids is necessary to achieve better stability in electricity networks.

- As climate change impacts the region, stress on energy resources is increasing. The ability to transmit electricity surpluses to areas with deficits will enhance energy security and, in turn, national security in the region.

- In addition to the significant advantages of regional interconnection, an interconnected grid offers a stronger incentive for Europe to connect to a region that is itself interconnected. In this regard, note the planned electricity connection to Europe via Cyprus (see further details below).

In addition, as the Atlantic Council’s Derentz has stated: “Load shifting could be a powerful incentive for such electricity connections as well, as grid operators balance demand heavily influenced by weather patterns.”

Some countries are not waiting for formal connections to be established between the MENA electricity blocks. For example, Egypt and Saudi Arabia have launched the Egypt-Saudi electricity interconnection project. Egypt has constructed several energy interconnectors as part of its plan to become an energy hub. One interconnector with Jordan has a capacity of 250 MW, which is expected to increase to 450–500 MW. A smaller interconnector with Sudan has a capacity of 80 MW, with plans to expand it to 300 MW. The third interconnector, with Libya, currently has a capacity of 200 MW.

In 2019, a MoU was signed to establish an interconnector with Cyprus and Greece, to be built in two phases of 1,000 MW each, providing a total capacity of 2,000 MW; the agreement is currently under technical study. Another interconnector, which is under study, would connect Egypt with Iraq via Jordan, transferring around 100–150 MW in the first phase and reaching 500–600 MW capacity in the second phase.

The Israelis seek to have their grid connect to the Mashreq grid. If this is not politically feasible, then at the very least, the Israeli grid should initially connect to neighboring countries, specifically Egypt and Jordan (and eventually Lebanon and Syria). As mentioned above, this can only occur realistically once certain political conditions are met following the October 7, 2023, war and its aftermath.

Project Prosperity is already envisioning an Israel-Jordan grid connection, as Jordan will be transporting electricity generated from its solar PV plant to Israel. This will necessitate a proper grid connection, which could serve as a foundation for additional grid connections with Israel. As Israel is positioned at a critical geographical location and at one of the possible gateways for exporting electricity to Europe, it will be crucial for its neighboring Arab countries to be able to transit electricity through Israel as an export option. For Israel and its neighbors, such a move would be an important step toward greater energy security. For European and US stakeholders, it would represent a significant de-escalation step in a troubled region.

Increased grid connectivity, however, could introduce greater vulnerability to cyberattacks on the network. Safeguarding the grids from such attacks and protecting the underlying energy production facilities—whether from renewable sources, conventional power stations, or nuclear power plants—will be crucial. At an Atlantic Council event in May 2023, Robert Silvers, under secretary for policy in the US Department of Homeland Security, highlighted the importance of cybersecurity for US energy infrastructure, emphasizing that all energy-exporting countries must prioritize these defenses.

Natural gas and nuclear energy

Natural gas

Natural gas plays a crucial role in the energy transition in the MENA region. As discussed above, energy remains at the forefront of regional diplomacy and beyond. Many countries rely almost entirely on natural gas for electricity generation. As a transitional fuel, this reliance is practical, especially compared to alternatives like diesel or coal, which are far more carbon-intensive. Currently, 60 percent of Israel’s electricity is generated from natural gas, and the country has been gradually closing down and preventing the establishment of new high-polluting coal and oil power stations. It is important to ensure that the current government implements these policies, which previous Israeli administrations set.

Jordan, as does Egypt, heavily relies on natural gas imports, primarily from Israel and Egypt, to meet most of its energy needs. Lebanon plans to gain access to natural gas via the Arab Gas Pipeline, and a potential gas discovery at the Qana field in the eastern Mediterranean Sea could allow Lebanon to meet some or all of its electricity needs through domestic natural gas. Similarly, Saudi Arabia, in addition to oil, relies on natural gas for power generation and plans to continue to do so for the foreseeable future. The Palestinians discovered gas offshore Gaza in the Gaza Marine field over twenty years ago but this has not as yet been developed; however, recent developments are encouraging as they suggest Egypt’s EGAS will develop the field with Palestinian partners, with a pipeline planned from the Gaza Marine field to Al Arish (see Figure 3).

The G4G project, briefly mentioned earlier, of which this author was the architect, was in the beginning of the implementation phase before the October 7, 2023, war, aiming to connect Gaza to natural gas. Understandably, this project, like any involving Gaza, will likely resume only as part of broader international efforts to rebuild Gaza after the war and a withdrawal of Israeli presence from the Strip. Initially, the gas would be supplied from Israeli fields, with the potential for sourcing from Gaza Marine through swaps in the future.

Countries in the region are already connected or in the process of establishing additional cross-border natural gas connections. The G4G project exemplifies how energy necessity and pragmatism can prevail over narrow political considerations. This principle was further demonstrated in the Lebanese-Israeli maritime agreement. The most challenging part of the G4G project that this author faced was securing formal approvals from both the Palestinian and Israeli prime ministers, as both needed to endorse the project. However, once political approval was obtained (as far back as 20167At the Qatari request, the Israel Defense Forces restated in 2023 the original political approval for the project granted in 2016.), the parties convened to work, and progress began in earnest.

After forming a G4G Task Force, international support was soon secured and funding naturally followed—initially critical funding from the Dutch and subsequently from the EU and Qatar with continuous political support from the United States (see Figure 3).8It will be interesting to see whether Qatar remains the project’s main funder or if others, such as the UAE, Saudi Arabia, or even the United States, step in. As mentioned, prior to the Israel-Hamas war, this project was in the implementation phase. Its continuation now depends on the commercial parties finalizing the necessary agreements and the Palestinians meeting the financial grant conditions set by the funders, once the conflict is over and political conditions allow for the project to resume.

The G4G project is likely the best example of a “plug-and-play” initiative that could be implemented as part of Gaza’s reconstruction. It is hoped that Palestinians, in cooperation with Israelis supported by international funders such as the EU and Qatar, along with ongoing support from the Netherlands and political support from the United States, will see this project to completion.

The cooperation paradigms demonstrated in the G4G project and other regional initiatives can serve as a foundation to deepen the energy ties that bolster energy security and, importantly, extend cooperation to tackling climate change. However, one of the clear lessons of the October 7, 2023, massacre and the ensuing bloody war is that any projects for Gaza requiring Israeli cooperation and international financial as well as political support will not be viable under Hamas’s rule in Gaza. The longstanding Netanyahu policy of strengthening Hamas in Gaza and enabling billions of dollars of funding go to it in exchange for “quiet” to weaken the Palestinian Authority has proven misguided.

Therefore, it is evident that projects such as G4G or any other major transformative infrastructure projects can only proceed once a moderate Palestinian regime controls Gaza. The practice of working on such projects through intermediaries, knowing Hamas was in control, is no longer tenable. Moreover, it is clear that international financing (especially Arab) or cooperation with Israel on such Palestinian projects will not be forthcoming as long as the extremist Netanyahu government remains in power.

While natural gas has proven to be a basis for cooperation between even longstanding adversaries (as demonstrated for years by the G4G project and the Lebanese-Israeli maritime agreement), the parties must also work together to jointly address global warming as the region transitions away from natural gas to cleaner fuels. Neom presents a promising starting point.

One proposal could involve building a spur pipeline from Neom to Jordan and from there to the Mediterranean via Israel. This would also allow for adaptation of the existing natural gas pipeline networks for hydrogen transport. In Israel, the natural gas network, according to the Israel Natural Gas Lines Co. (INGL), is expected to have the capacity to transport at least 30 percent hydrogen. The same would apply to the G4G pipeline, as INGL ensured it could eventually transport hydrogen, with carbon capture, utilization, and storage technology considered for the Gaza Power Plant.

International stakeholders, especially the EU and the Dutch government, welcomed and even stipulated these provisions to align with their own decarbonization policies, particularly regarding development aid.

In terms of other regional gas pipeline projects or initiatives, Israel is planning a new pipeline from Israel to Port Said near Damietta to increase the supply of Israeli gas to Egypt, as Egypt will be reliant on increased imports of Israeli gas in the coming years (see Figure 3). Furthermore, on the eve of the Israel-Hamas war, the Palestinians were advancing a project in cooperation with Israel to supply natural gas to the West Bank at Jenin. This project will provide an important source of fuel to the West Bank, as it is tied to the planned combined cycle gas turbine plant in Jenin.

There are plans for an eventual extension of the Arab Gas Pipeline to Iraq, although no tangible progress has been made in that regard. Additionally, Israel has plans on the drawing board for another gas connection to Egypt, running onshore from Ashalim in the Negev Desert to the Egyptian border, but no significant progress has been made regarding this project either.

It is also worth mentioning the East Med Gas Pipeline, which is designed to transport natural gas from offshore Israel and Egypt through Cyprus (and potentially Lebanese gas, should sufficient quantities be discovered) to Europe. The $6 billion–$7 billion initiative, apart from providing an export market for Eastern Mediterranean gas, was welcomed in Europe, especially in the wake of the Russian war in Ukraine, as Europe sought to diversify away from Russian gas. However, the withdrawal of US support for the project, coupled with unresolved political issues involving Cyprus and high costs, has all but rendered this initiative defunct. Instead, the United States and others have opted to support electricity connections from the Eastern Mediterranean to Europe, particularly in support of renewable energy-generated electricity.

Shangyou Nie and Robin Mills, nonresident fellows at the Center on Global Energy Policy at Columbia University’s School of International and Public Affairs, argue in their report that although a “New Eastern Mediterranean gas exploration that could enter production around 2030 would find a ready market in Egypt . . . gas producers in Israel and Cyprus would likely not want to be completely dependent on the Egyptian market given that Egypt would have large commercial leverage and (as in the post-2011 period) may not pay promptly, may divert gas from LNG re-exports to the domestic market, and/or may seek to pay well below LNG parity.”

In 2030, Nie and Mills may be correct, but as the EU seeks to transition away from natural gas post-2030 to cleaner sources of energy, Israel may begin to struggle to find markets for its gas beyond the Middle East.

The Egyptian Constitution, meanwhile, mentions renewable energy as a key part of the country’s energy mix.

Nuclear

Israel

According to one senior Israeli security analyst, who spoke on the condition of anonymity citing security concerns, the reason Israel doesn’t have nuclear energy is that, despite having nuclear technology capabilities, it has not invested in the necessary research and development for the country to develop its own nuclear energy capabilities. Furthermore, as Israel is not a signatory to the Nuclear Non-Proliferation Treaty (NPT), importing the technology from the United States, South Korea, and other countries is not currently a feasible option. However, as nuclear energy remains a clean alternative to hydrocarbons as part of the energy transition, it would be prudent for the country to explore ways to incorporate this into its energy mix. This won’t be straightforward, but at the very least, a serious road map should commence in this regard in consultation with Israel’s allies.

Saudi Arabia

As part of its energy vision, Saudi Arabia is exploring nuclear technology to add to its energy mix. The kingdom is seeking US support while also considering offers from France, China, and Russia. Recently, this issue has become linked to normalization talks with Israel, which, according to a recent report, has agreed to Saudi Arabia having the capability of enriching uranium on its own territory for civilian nuclear energy purposes. As a signatory to the NPT, Saudi Arabia is entitled to import nuclear technology for peaceful uses.

Nuclear energy possibilities for both Israel and Saudi Arabia will likely be shaped by the regional outcomes following the Israel-Hamas war. For example, if Hamas and the Netanyahu government were to leave the scene, and Israelis and Palestinians were to resume efforts toward a permanent solution, this would likely be accompanied by a deepening of the normalization process, potentially including a security defense pact. This, in turn, could open new possibilities for nuclear energy in the region.

Jordan

Jordan, too, seeks to diversify its energy mix and as it is highly dependent on imports, it is seeking to include nuclear energy. More specifically, Jordan has been considering SMRs. Jordan has significant uranium deposits. As Jordan is keen to increase its energy independence, nuclear energy would clearly contribute to that goal.

Egypt

Egypt is planning nuclear energy production of 1.2 GW at the El Dabaa site, initially with Russian developers and financing, as well as South Korean subcontracting.

There are concerns that a proliferation of nuclear programs, even if for civilian purposes, could trigger a new nuclear race in the region. Statements by Saudi Arabia regarding the Iranian nuclear program add further support to this contention. However, countries globally, including those in the MENA region, should consider nuclear energy. Although expensive and requiring strict supervision, regulation, and compliance—including adherence to the NPT—it remains an important part of the energy mix. Nuclear facilities should ideally be housed in stable countries (unfortunately, this not always a guarantee in the region). Achieving this will depend on favorable political conditions.

COP28, COP29, and beyond

The UAE hosted COP28 in 2023. Ahead of the summit, ADNOC, the oil major led by the UAE’s Sultan Al Jaber (who also served as COP28 president), announced that it had awarded the world’s first carbon-neutral gas project, valued at seventeen billion dollars. If successful, this project could set a new standard for the industry during the energy transition. In 2023, ADNOC announced it would become net zero by 2045, five years ahead of the commonly targeted date of 2050, and committed to achieving zero methane emissions by 2030. These are welcome announcements from one of the leading global oil companies.

It was crucial for the UAE to bring the oil majors to the table at COP28 in Dubai to secure meaningful carbon emissions reduction commitments from them. Equally important was mobilizing substantial public and private financing for the energy transition and encouraging and rewarding innovation in the climate space.

Governments and development finance institutions such as the EBRD, EIB, World Bank, the US International Development Finance Corporation, and others have a critical role to play here—especially in the Global South—as does the private sector. The International Energy Agency stated:

“[T]o avoid the worst impacts of climate change, we’ll need to spend a lot more. About $4.5 trillion a year by the early 2030s . . .”

The majority of this funding will need to come from private finance.

Among COP28’s key achievements were ten pledges by countries around the world, including:

- Global Renewables and Energy Efficiency Pledge: Accelerating deployment of renewables (to triple global installed capacity by 2030) and energy efficiency (to double the global average annual rate of energy efficiency improvement through 2030) through domestic action.

- Coalition for High-Ambition Multilevel Partnerships Pledge: Enhancing cooperation with subnational governments in the planning, financing, implementing, and monitoring of climate strategies to maximize climate action and increase adaptation and resilience.

- Declaration of Intent on the Mutual Recognition of Certification Schemes for Renewable and Low-Carbon Hydrogen and Hydrogen Derivatives: Establishing mutual recognition of certification schemes for renewable and low-carbon hydrogen and hydrogen derivatives.

- Declaration on Climate Finance: Bolstering investment to green the global economy, especially in support of emerging and developing economies, via increased concessional and private finance, more effective multilateral development banks, and robust carbon markets.

- Critically, for the first time ever, fossil fuel transition was included in the final COP text. Specifically, the final Global Stocktake focused on “transitioning away from fossil fuels in energy systems in a just, orderly and equitable manner.”

In the realm of climate finance, a few important milestones were reached, including:

- Commitments of just under $800 million to the Loss and Damage Fund.

- The establishment of Altérra, a climate investment fund launched to mobilize large-scale investment for a new climate economy, with an initial capitalization of $30 billion and a target of $250 billion.

Bain and Company summarized that a total of $85 billion was mobilized at COP28. Bain also projected a 2.1 degree Celsius temperature rise by the end of the century based on the pledges and targets made at COP28. Although this is an improvement from COP25’s projection of 2.8 degrees Celsius, much more remains to be done in upcoming COPs to ensure we do not exceed 2.1 degrees Celsius—and, ideally, to lower this target even further.

Given the accelerated rate of warming in the MENA region, it is especially urgent to fulfill the commitments and pledges made at COP28. This urgency underscores the need for a realistic yet rapid and genuine transition away from fossil fuels.

What remains to be seen is whether the next COPs—the aftermath of COP29 in Baku, COP30 in Brazil, and beyond—will sustain the momentum needed to reach agreement on key milestones to tackle climate change. Specifically, at COP29, it was important to build on the climate finance momentum and pledges made at COP28. In addition to mobilizing private capital, states must also mobilize public funding for developing countries, as outlined in the New Collective Quantified Goal. Moreover, the challenges facing carbon markets must be addressed comprehensively. The Loss and Damage Fund will need to be strengthened and expanded to achieve tangible success. The standards adopted at COP29 under the Paris Agreement should unlock $250 billion annually for streamlining carbon credits projects.

Finally, as the World Economic Forum rightly states, it is crucial to refocus efforts on adaptation to climate change, not just mitigation.9At time of writing, the full outcomes of COP29 were still being assessed. The fact that Azerbaijan hosted COP29 presented an opportunity, as seen at COP28, for a major hydrocarbon-producing nation to take the lead in brokering agreements on a phased, measured, and accountable reduction of fossil fuels as part of the energy transition.

COP30 in Brazil will provide another opportunity to focus on measures that support and incentivize Global South countries in tackling climate change. As Brazil begins preparations for COP30, there will likely be a renewed emphasis on the rainforest and the shared global responsibility—from north to south, east to west—to protect the “earth’s lungs.”

Conclusion

The MENA region is facing an impending catastrophe as a result of climate change. Without collaborative efforts to adapt and mitigate its impacts, the region will likely face increasing climate-driven conflicts. However, as evidenced by the Israel-Hamas war, conflict remains an ever-present reality, making cross-border cooperation—however necessary—an ongoing challenge.

The ongoing conflict began with a massacre by Hamas, which included kidnappings and assaults in southern Israel, leading to Israeli retaliatory strikes in Gaza that have caused significant destruction and numerous casualties. The situation further escalated when Hezbollah in Lebanon and the Houthis in Yemen and Iraqi and Syrian militias joined in attacking Israel and its allies (in the case of the Houthis) as well as direct attacks from Iran against Israel. The region now stands at a pivotal crossroads. If the United States initiates a process to solve the Israeli-Palestinian conflict permanently, it could, in parallel, support both existing and new initiatives that promote cooperation on energy and climate issues across political boundaries, as demonstrated in this paper.

Two preconditions are critical for this cooperation. First, the complete removal of Hamas’s military and political capabilities in the Palestinian territories. Second, the departure of Netanyahu and his government to pave the way for genuine peace talks toward Palestinian statehood. Meeting these conditions could lead to real cross-border collaboration, as well as the resumption and expansion of the Abraham Accords. The projects, initiatives and platforms proposed in this paper could pose, should this be useful, an energy component of a US comprehensive plan for the region which can be a cornerstone of a new US administration.

Regional groupings, both new and reformed (e.g., EMGF/EMEF+), can play a helpful role in this regard. We are witnessing new—or at least reinvigorated—energy diplomacy from both regional and external actors. While such diplomacy has the potential to lead to conflict, if conducted correctly, it can instead be harnessed for cooperation among the countries in the region regarding energy and climate change. States need to consider infrastructure and climate change security at similar levels as they have considered traditional security alliances, evaluating which alliances best serve their climate and energy security concerns. Climate change is increasingly becoming a national security issue.

The United States should prioritize resolving the Israeli-Palestinian conflict, followed by the demarcation of the Israel-Lebanon land border and addressing the Turkey-Greece-Cyprus issue, to ease tensions in the Eastern Mediterranean and the Middle East, thereby providing a basis for stronger energy cooperation. Given the instability in the region, especially in the Levant, it will be essential for key external actors, such as the United States, to lead these efforts. It is proposed that the United States work with its allies, particularly in the region, to establish formal mechanisms that ensure cooperation across borders on combating climate change and supplying energy throughout the area. Such a mechanism will need to withstand internal chaos (as we are currently witnessing in Israel and Lebanon, for example) as well as cross-border conflict and political tensions.

Specifically, it is proposed that the United States—ideally with its ally, the UAE—launch a set of formal energy and climate task forces, ideally with a non-partisan structure that can endure a change of government in the United States or the Middle East, for each area, such as on Middle East electricity grid connections, Middle East gas pipeline networks, hydrogen, renewable energy (such as solar PV), and cybersecurity. These task forces should be represented by Middle Eastern countries and chaired by the United States (and/or its allies, such as the UAE). Their members should include energy and climate experts from the region and representatives from both the private sector and governmental finance.

The task forces would be a nonpolitical gathering with the sole aim of cross-border planning and implementation of projects. Task force members would report to the lead (United States/UAE) on a regular basis regarding the status of cross-border projects and cooperation. The United States could bring in other countries, financial institutions, and the private sector to provide financing for these initiatives. The projects and initiatives could build on existing efforts, agreements, and initiatives. While these projects alone will not bring peace to the region, they can play a critical role in fostering much-needed cooperation if the peoples of the region are to have a fighting chance against the ultimate threat to which they are all vulnerable: climate change.

About the author

Ariel Ezrahi is a nonresident senior fellow with the Atlantic Council’s Middle East Programs. Ezrahi was the architect of the Gas for Gaza project and chaired its task force since inception. He worked closely with the Netherlands, the European Union, and Qatar, the project’s key international actors, on this cornerstone Palestinian project, in close cooperation with Israel and with support from the US government.

Related content

About our work

The Scowcroft Middle East Security Initiative (SMESI) provides policymakers fresh insights into core US national security interests by leveraging its expertise, networks, and on-the-ground programs to develop unique and holistic assessments on the future of the most pressing strategic, political, and security challenges and opportunities in the Middle East.

Image: Saudi man looks at the solar plant in Uyayna, north of Riyadh, Saudi Arabia April 10, 2018. Picture taken April 10, 2018. REUTERS/Faisal Al Nasser