Sub-Saharan Africa grapples with development imperatives

Table of contents

Evolution of freedom

The evolution of the Freedom Index for Sub-Saharan Africa closely resembles that of the global average since 1995, with a very mild convergence. The same is also true for the subindexes of economic, political, and legal freedom. This is already good news for the region, as the trends are positive, but this does not capture the full story of freedom development in Africa. This is because the big movement towards liberalization, especially in terms of economic freedom, took place during the 1980–2000 period, so largely before the starting point of the Freedom and Prosperity Indexes data set.

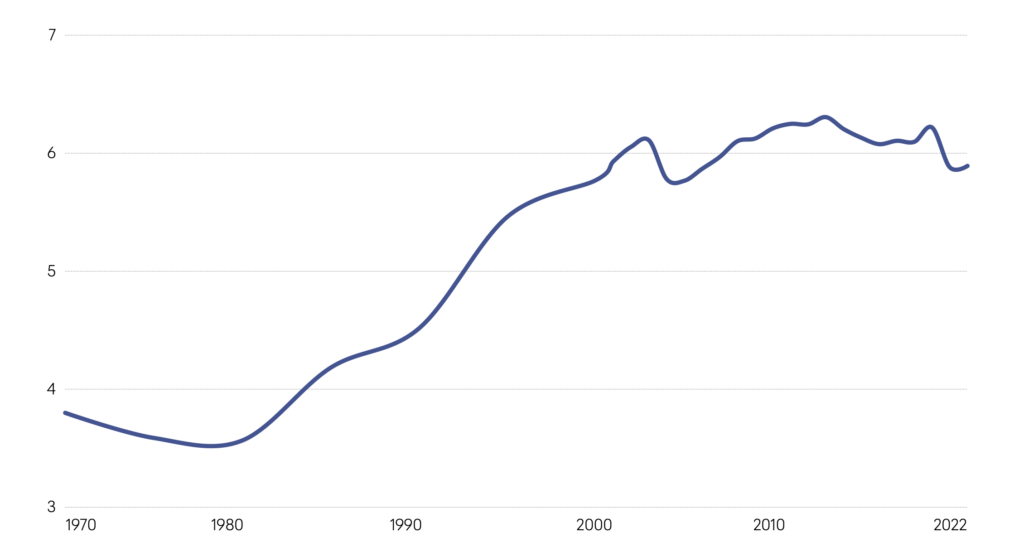

In 1970, all dimensions of economic freedom were extremely low in most of the countries of Sub-Saharan Africa. Figure 1 below shows the evolution of trade freedom back to 1970, obtained from the same source used in the Freedom and Prosperity Indexes (the Fraser Institute’s Economic Freedom of the World index). The average score for the region at the beginning of the period was around 3.8 out of 10, significantly lower than the rest of the world (5.5). In the 1970s, governments were following counterproductive policies such as overvalued exchange rates or quantitative restrictions on trade. These policies were destroying any possibilities to develop an exporting sector because, with an overvalued exchange rate, exports were simply uncompetitive. Exporters would have to turn in their dollar earnings at an artificially low rate and, in many cases, they would have to resort to the black market to buy their imports. The number of countries in Sub-Saharan Africa with a black market premium above 40 percent was very substantial.

A big wave of economic liberalization took place in the 1980–2000 period, with governments correcting the artificial distortions in their exchange rates and opening trade and financial flows. So, this first dramatic movement towards a more economically free environment is not captured by the economic freedom subindex, which mainly shows what we could call a second wave of liberalization after the year 2000. This has been mainly driven by increasing women’s economic rights, which have clearly improved in some countries of the region, but certainly not all. Investment freedom has also improved in the last ten years, making capital movements more efficient. This is evident when you observe that there are no countries today in Sub-Saharan Africa with black market premiums above 20 percent.

Figure 1. Trade freedom in Sub-Saharan Africa, 1970–2022

Property rights also show a mild improvement in recent decades, but the weak institutional environment portrayed by the legal freedom subindex probably represents the biggest constraint to further improvement nowadays. The very low and stagnant levels of all indicators of legal freedom, especially that of bureaucracy and corruption, impose a significant drag on Sub-Saharan Africa’s development. A critical aspect of legal freedom is security, a very unstable area in Africa. Religious and ethnic conflicts are always a risk in the region, and this generates a high level of uncertainty, which can have negative effects on investment and economic development.

The development of political freedom in Sub-Saharan Africa was not so great as economic liberalization, and the democratic institutional framework is rather weak in those places that transitioned to more inclusive political regimes. This is well captured by the fact that legislative constraints on the executive are significantly lower than the rest of the indicators of the political freedom subindex, and judicial independence is also low, suggesting that proper systems of democratic checks and balances are still not fully developed in most countries.

Overall, the story of the development of freedom in Sub-Saharan Africa has so far been very uneven, in two senses: First, there is large variability across countries in the region. Second, there is large variability among dimensions of freedom. Economic freedom really took off after 1980, but legal and political institutions have not really improved. And this situation imposes a constraint on development because there is complementarity among different areas, so reforms in one aspect need supporting reform in others if they are to be successful in the long run. Moreover, further progress in legal and political freedoms are not just means to achieving higher levels of material prosperity, but are in themselves a measure of well-being, which emphasizes the need for continuing liberalization in these areas.

From freedom to prosperity

The Prosperity Index shows a parallel evolution of the Sub-Saharan African region and the global average. Even if we would hope to see a stronger process of convergence, so that Sub-Saharan Africa would catch up with the rest of the world, parallel trends are already good news for the region. Compared to the situation before the 1980s, where Africa was significantly falling behind the global average, the fact that, in the last three decades, the region has been able to develop at a similar pace to other regions is a clear sign that the economic liberalization of the 1980–2000 period has paid off.

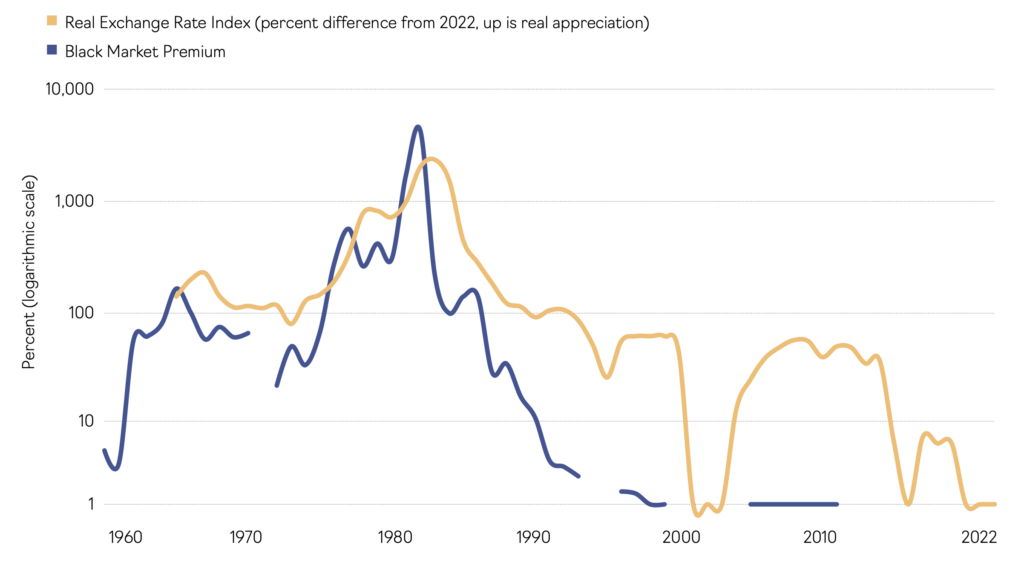

An extreme example of the trends of both freedom and prosperity is Ghana. Figure 2 shows what was happening with exchange rates and black market premiums over the last sixty-two years. By 1982, the real exchange rate had appreciated to a level that was more than one thousand percent higher than it is today. The black market premium on foreign exchange was also above a thousand percent. The consequences were disastrous. Ghana used to dominate the world market for cocoa. By 1982, Ghanaian cocoa growers were receiving only 6 percent of the world price, and cocoa exports had collapsed. Facing famine, Ghanaian leader Jerry Rawlins began reforms in 1984. The government devalued sharply the nominal exchange rate and thereby reduced the black market premium.

Figure 2. Black market premium and real exchange rate index in Ghana, 1960–2022

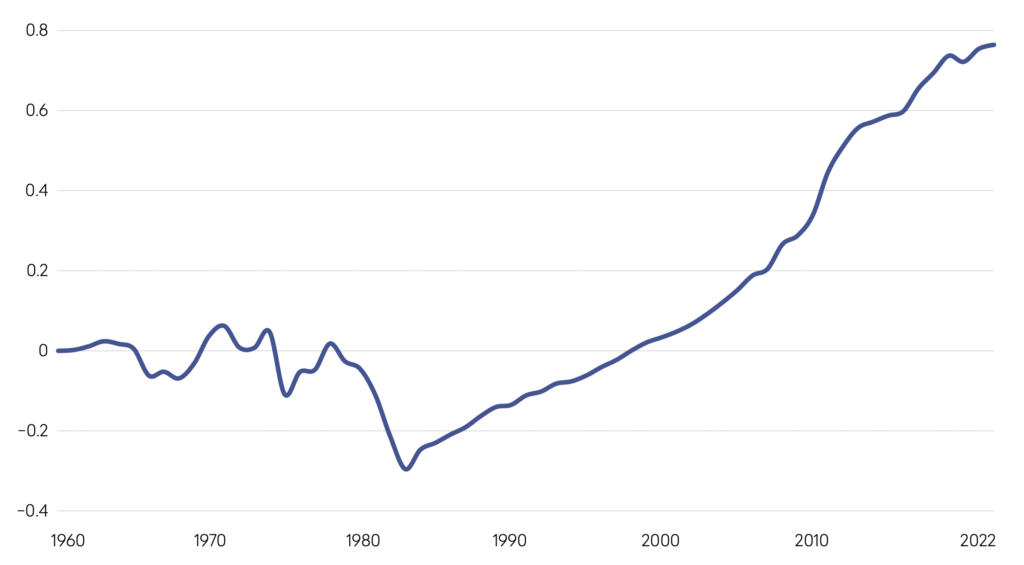

The economic liberalization coincided with a turning point for Ghana’s economy. As shown in Figure 3, Ghana experienced a sharp decline in per capita income from 1960 to 1983. After the reforms, Ghana registered a steady rate of economic growth that has continued ever since.

Ghana also undertook some political liberalization in 2000, and since then Ghana has had an unbroken series of competitive elections. This may also have contributed to Ghana’s steady growth in the new millennium.

Getting back to Sub-Saharan Africa as a whole, indicators like health and environment show a very rapid improvement throughout the period of analysis. It is true that the starting point was really low, and thus there remains ample room for improvement in the future. Foreign aid, which has clearly been ineffective in other areas, may have helped improve health and sanitation conditions, especially in rural areas. For example, early life mortality has significantly decreased in recent times, which accounts for an important share of the progress in overall life expectancy.

Figure 3. Cumulative logarithmic growth in per capital income in Ghana since 1960

Some progress has also been occurring in education, in terms of convergence with global averages in primary and secondary school enrollment. However, the education indicator of the Prosperity Index, which measures average years of education, does not fully show the region’s convergence towards the rest of the world. This may be due to faster expansions in college enrollment in other regions like Asia and Latin America compared to Sub-Saharan Africa. But the growth in the number of people enrolled in early levels of education in Africa is substantial. Nonetheless, another aspect of education not captured by the Prosperity Index is quality, and this is obviously an issue in Sub-Saharan Africa. When you consider quantity and quality, it is clear that there is still a lot of progress to be made.

The future ahead

The different dimensions of the Freedom Index very well identify the constraints and challenges of Sub-Saharan Africa’s development in the medium and long term. Economic liberalization has borne fruit lately, although further financial and trade integration of the region with the rest of the world should continue. But today the big challenge is to strengthen the process of democratization and institution building, and the necessary reforms in these areas are much harder to accomplish. The recent wave of military coups is not a promising sign, and there is ongoing conflict associated with Islamic movements in some areas. So, the situation regarding security and the maintenance of peace is a necessary condition for Sub-Saharan African development.

I think there is probably not going to be as much support for African development from international institutions and foreign countries as there was in the past (particularly in the 2000s), because there is a shift of focus towards other regions, like Ukraine and Eastern Europe. Also, I assume that the Israel-Hamas War will continue to focus attention towards the Middle East. Usually, things tend to go in cycles. I do not think that foreign support was all that successful in achieving economic growth, but aid probably deserves some of the credit for the progress on health and education, especially.

In relation to foreign influences in the region, I do not think that China’s Belt and Road Initiative will have very different results than the significant amounts of funds received by Sub-Saharan African countries from Western nations during the 1980–2010 period. Moreover, I think the same problems of debt repayment and default are likely to be repeated, this time with China’s investments. At the end of the day, for foreign investment and aid to successfully affect Africa’s economic development, it has to be directed to some productive uses. And this is not usually the case with this kind of heavily politicized financing.

Finally, the efforts to deepen economic and financial integration within the region are probably a good idea, as within-region trade is unusually low for neighboring countries in Sub-Saharan Africa. But it is certainly not an easy task, as the several unsuccessful attempts to promote free trade areas or common currencies in the region in the last several decades prove. This failure may be due to Africa’s burden of having too many countries, some of them very small states. This generates great difficulties in reaching agreements because there are multiple strong political interests. Institutional development and democratic reform may help in this sense, as deeper integration among African nations would probably benefit the majority of the population.

William Easterly is professor of economics at New York University. He is the author of The Tyranny of Experts: Economists, Dictators, and the Forgotten Rights of the Poor (2014), The White Man’s Burden: Why the West’s Efforts to Aid the Rest Have Done So Much Ill and So Little Good (2006), and The Elusive Quest for Growth (2001). He has published more than 70 peer-reviewed academic articles.

EXPLORE THE DATA

Image: A poll worker puts ink on the finger of a voter during the parliamentary election in Cotonou, Benin, January 8, 2023. REUTERS/Charles Placide Tossou