It is abundantly clear that achieving net-zero carbon emissions by mid-century is necessary to avoid the worst climate outcomes. However, the path to decarbonizing the energy sector is not “one-size-fits-all” between developed and developing markets. Given the historical tensions between developed economies, which modernized with fossil fuels, and developing economies, now being asked to forgo this route, it is evident that sustainable, long-term global cooperation will require addressing the ”energy trilemma”—the need for the people to have access to sustainable, reliable, and affordable energy.

Sustainability is more urgent for countries hardest hit by climate change and often exposed to greater environmental risks. Reliability remains an elusive goal in many countries still working to bring basic electricity to its citizens in a secure and dependable way. Many of these developing economies also face roadblocks to electricity affordability due to weak government finances and credit, and corresponding higher cost of capital for infrastructure development.

Looking at the future energy mix globally, new renewables capacity will dominate with developing countries representing more than half of new capacity investment, driven primarily by China and India. Going forward, natural gas power generation will continue to serve as an important source of baseload generation, especially for countries in the early stages of the energy transition. Examples of this include South Africa, where coal accounts for the majority of the country’s electricity generation, and Nigeria, where replacing diesel fuel with natural gas along with improvements in the power grid will contribute to major reductions in carbon emissions in sub-Saharan Africa.

Public capital plays an essential role in accelerating energy infrastructure projects in both developed and developing markets. Governmental organizations such as export credit agencies (ECAs) and development finance institutions (DFIs) provide essential liquidity tools, risk management expertise, and credit support that enables meaningful private sector investment.

Energy transition case study: South Africa

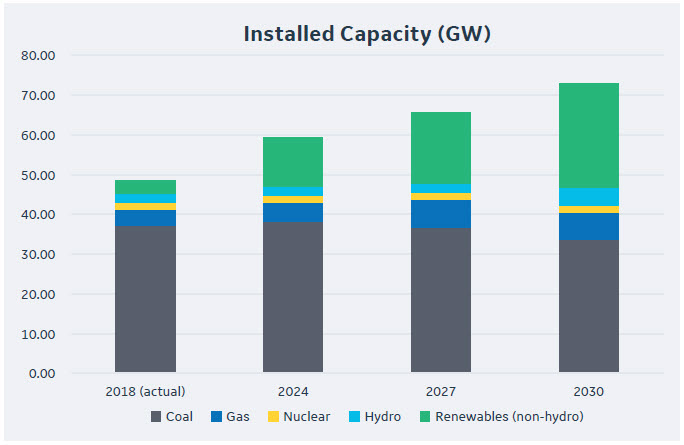

Coal-fired generation currently accounts for more than 70 percent of installed capacity in South Africa. With rising energy demand in the country, coal is expected to remain the primary power generation source through 2030. While total installed coal capacity will decrease due to retirements, approximately 1.5 gigawatts (GW) of new supercritical and modernized coal plant replacements are expected to come online between 2023 and 2027. South Africa’s Integrated Resource Plan aims to install 3 GW and 9.6 GW of solar and wind capacity respectively between 2023 and 2028. Gas capacity will remain somewhat limited in South Africa due to infrastructure challenges and dependence on price-volatile liquefied natural gas (LNG) imports.

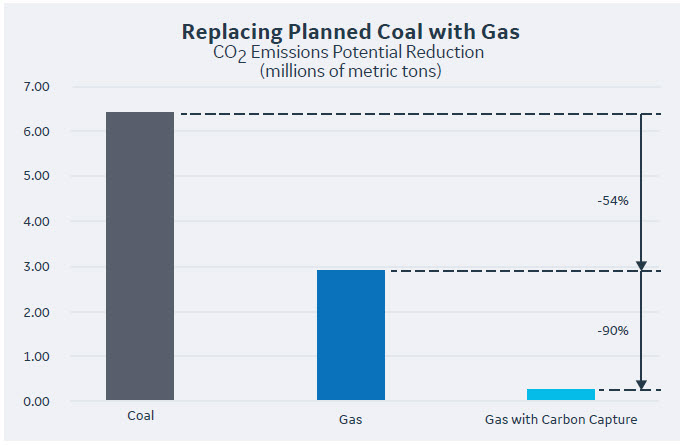

US government financing support for natural gas-fired power generation projects could support switching of the planned new coal additions to cleaner natural gas. The result would be an approximate 50 percent decrease (3.5 million metric tons) in carbon emissions by 2030 and would deliver cleaner, more sustainable, and reliable power. Adding carbon capture could further reduce emissions by up to 90 percent. Achieving these results requires a drastic shift in policy that supports gas infrastructure and LNG supply.

The role of public capital

Now more than ever, developing markets need continued government-supported financing for renewables and gas power generation to support an equitable energy transition. Despite significant global liquidity for financing energy transition projects, private sector capital requires credit support to mitigate the fundamental developing market risks: poor underlying credit and commercial structures, regulatory challenges, political uncertainty, and long-term underinvestment in infrastructure.

ECAs and DFIs have traditionally played an important role in catalyzing private sector investment in long-cycle energy and infrastructure projects globally. To meet net-zero goals, these institutions must continue to maintain central roles in the financing ecosystem. They can support sustainable infrastructure buildout through several channels:

- Access to liquidity. ECAs can counterbalance cyclical liquidity challenges through tools such as direct lending and by providing optimal indemnity to unlock longer-term, competitive commercial bank funding. Continued innovation on financing structures is needed in areas such as blended concessional finance instruments, local currency financing, and bridge solutions.

- Risk allocation. DFIs can deploy a wide range of instruments that can address risk and risk allocation factors not adequately addressed in, for example, a power purchase agreement, or in other supply, transmission, or interconnection agreements. These risk mitigants include political risk insurance, export credit, partial loan guarantees, and credit enhancements.

- Project execution. Due to inherent risk factors, there are often financing gaps at early stages of development of energy infrastructure projects. DFI involvement at this stage, for example, can incentivize large institutional investors and draw local financing participation early on. Such involvement can increase the probability of project success and potentially yield substantial economic development benefits. Further, projects with larger capex requirements, such as mega-offshore wind projects, require ECA support; often more than one ECA is required to fill financing gaps. Overall, public capital institutions can bring rigor and discipline to underwriting, structuring, and negotiation of projects and loan documentation that can increase the credibility and execution of an opportunity.

- Technology innovation. ECAs play a leading role in support of new technology advancements, providing financial institutions comfort in financing new technologies. ECA willingness address technology risk is key to facilitating commercialization of decarbonization technology and projects. ECAs have room to be more forward-leaning in their approach to risk assessment and underwriting.

- A just energy transition. To meet global decarbonization goals while continuing to drive electrification and raise the standard of living in developing markets, ECAs and DFIs should strive to become even more engaged to support a broad range of decarbonization technologies, including for example, support of new natural gas power generation projects to replace existing or planned coal assets—a baseload power solution that ultimately helps to bring more renewable energy online.

With the 27th Conference of the Parties (COP27) now convened in Egypt, there is no time to waste. To drive global decarbonization and increase electrification in developing countries, policymakers and financial institutions must partner with project sponsors to tailor capital solutions that best fit each region and country. ECAs and DFIs, along with banks and other multilaterals, play a critical role in enabling access to the capital required to deliver a more just and equitable energy transition today and for future generations.

Susan Flanagan is the president and chief executive officer of GE Energy Financial Services. GE is a presenting partner of GEC at COP27: Ambitions for All.

Related content

Learn more about the Global Energy Center

The Global Energy Center develops and promotes pragmatic and nonpartisan policy solutions designed to advance global energy security, enhance economic opportunity, and accelerate pathways to net-zero emissions.

Image: Wind turbines in a field. (Arteum.ro, Unsplash, Unsplash License) https://unsplash.com/license