Addressing African debt burdens

In the first two months of 2020, before COVID-19 struck the global economy, emerging markets experts warned of a growing “wall” of sovereign debt repayments threatening many African nations. Obligations to official ( i.e., national) creditors comprised a large share of the burden, but of equal concern was the growth of indebtedness to private (i.e., individual) creditors, fueled by recent years’ increases in foreign bond issuance.

By the start of 2021, concern has become crisis. Across the world, COVID-19 has ravaged economies and government revenues. For many sub-Saharan African (SSA) nations, that has tipped the delicate balance of debt. Zambia was the first affected, defaulting on debt obligations in November. Many more must take action to avoid the same fate, including Angola, Gabon, Ghana, and Kenya, among others.

The crisis

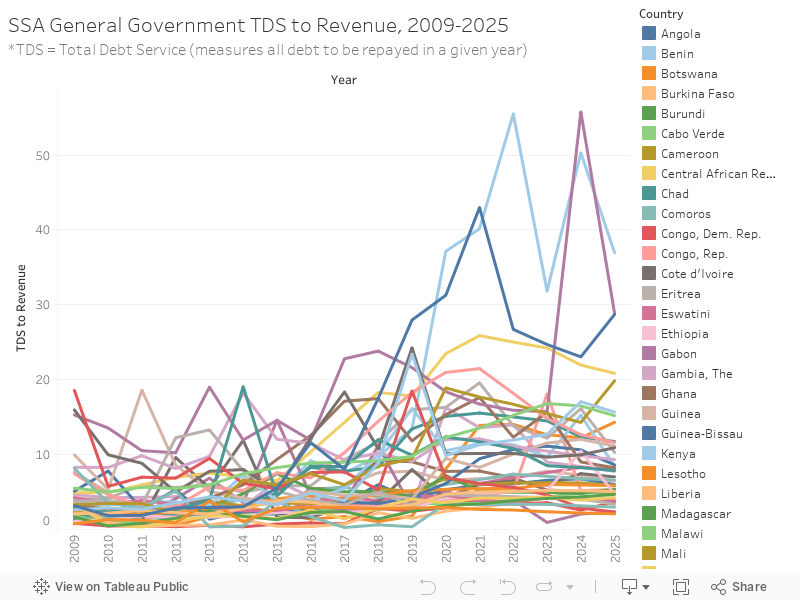

Data from the World Bank’s October 2020 International Debt Statistics report and the IMF’s World Economic Outlook from the same month reveals problematic repayment schedules across the region in the next decade. Below, yearly total debt service is given as a percentage of expected revenue for SSA 43 nations between 2009 and 2027.

Hover over data points to learn more. Click on a specific country (right) or line graph to highlight it.

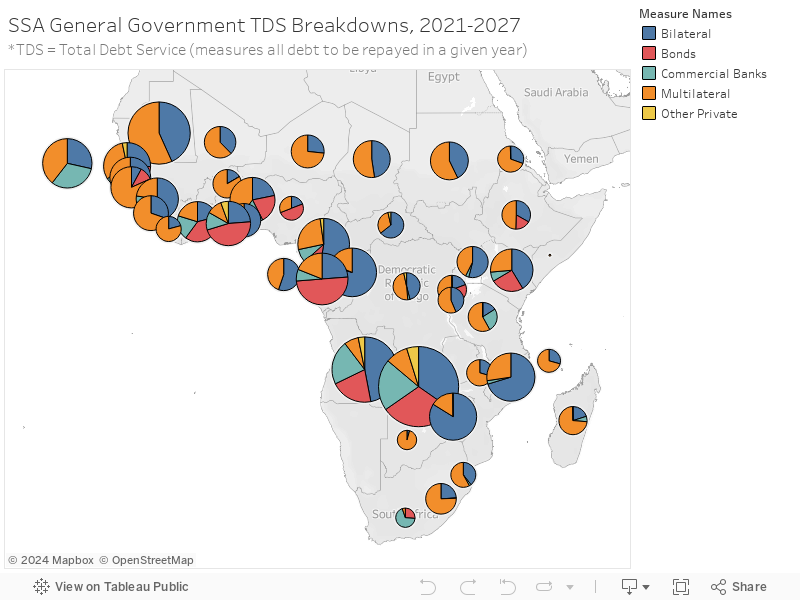

Further analysis reveals the estimated makeup of SSA nations’ debt totals. Pie charts below are sized by the yearly debt repayment to government revenue percentages given above.

Hover over pie charts to learn more. Zoom in to view charts otherwise obstructed.

International organizations recognized the need for support in the face of this crisis. Earlier in the year, the IMF and World Bank worked with G20 nations to establish the Debt Service Suspension Initiative (DSSI), making 73 low- to middle-income countries eligible for a suspension of bilateral debt service obligations through June 2021. More recently, the G20 has focused on long-term solutions to this debt crisis, developing a proposal (the “Common Framework”) for debt restructuring for the same nations targeted by the DSSI.

Crucially, the DSSI attempted to but was unsuccessful in engaging private sector creditors in a suspension agreement. Also hurting the initiative’s efficacy was that 40% (as of early December) of eligible countries refused relief out of concern at tanking national credit ratings.

On the whole, therefore, international support has been insufficient. Even where bilateral service suspensions were granted, the failure to properly address private sector debt obligations like outstanding bonds ensured that the looming problem was only partially solved. Thus, solving the private sector aspect of the African debt crisis must presently be a priority.

Addressing bond debt

Three major issues must be addressed to ensure that SSA nations can both weather the debt crisis and ensure future debt sustainability.

First, centralization (or the consolidation of debts through an intermediary) is essential for emergency relief of private sector debt burdens. For many SSA nations with significant bond debt, a large and diverse corps of bond creditors forces debt treatment negotiations to take place on a case by case basis, making broad repayment suspensions in the region nearly impossible and preventing effective action in the short-run.

To combat this issue, separate proposals by the UN Economic Commission for Africa and the UK-based Centre for Economic Policy Research (CEPR) advocate for the exchange of debt into concessional paper or its consolidation into “central credit facilities”, respectively. In its new form, the debt would be guaranteed by a trusted intermediary (the World Bank given as an example by the CEPR) in an attempt to assuage investor concerns about receiving returns in a timely manner. Such centralization, if successful, would provide a workable solution for several burdened nations at once.

Second, transparency in debt obligations is key to both managing current debts and improving sustainability. In the short term, bondholders are resistant to granting debt holidays before they understand the full picture of a country’s debt makeup. This was clear in Zambia, where a lack of transparency in the nation’s obligations to Chinese creditors was one of the hurdlesto successful suspension negotiations, thus contributing to the nation’s default. Additionally, in the long term, higher transparency may reduce the risk of investing in SSA nations, eliminating the possibility of hidden debts that affect nations’ capacities to repay other creditors (as seen in Mozambique in 2016).

State-sponsored Chinese lending to SSA nations is often highly opaque, but recent data suggests that the volume of such lending is winding down. However, pressure from the international community should still be employed to ensure that secretive lending from any sovereign creditor is largely eliminated, ensuring a more open investment environment.

Finally, acknowledging that centralization and transparency are useful in the short-term mainly to encourage debt moratoriums, restructuring is an important step in the next stage of crisis response. Simply pushing back repayments means that SSA nations will suffer again at a later date. Outstanding debt obligations between these nations and their private creditors must be renegotiated and reduced.

Here, the G20 Common Framework for Debt Treatments, announced in November, is pertinent. With regards to the private sector, the framework encourages restructuring discussions with private creditors that will likely be contingent on SSA nations negotiating IMF programs. Such discussions must begin soon, as any delay means further distress.

–

An adequate response to this debt crisis does not end with solutions for the short time horizon. When the immediate debt threat in Sub-Saharan Africa is reduced, focus must shift to reforming the system at play (fairer credit ratings, cheaper borrowing terms) to prevent similar crises in the future.

But the crisis rages presently, and focus cannot turn toward the distant future yet. As solutions to official sector obligations begin to emerge, private sector debt must be addressed with equal intensity, employing pragmatic solutions suited to all parties involved.

Stefan de Villiers is a former intern at the Atlantic Council’s GeoEconomics Center and currently studies economics and data science at the University of Washington.

At the intersection of economics, finance, and foreign policy, the GeoEconomics Center is a translation hub with the goal of helping shape a better global economic future.