The Greater Caspian region: A new Silk Road, with or without a new belt

With the signing of a US-Taliban peace agreement, now might be a good time to look ahead to how Afghanistan might strengthen its economic connectivity with both its neighbors and more distant markets. Now, there will be a 135-day period of de-escalation of violence. If there are no major attacks, then the path will be clear to negotiate to add the Afghan Government to the agreement structure. This will be tricky, as today’s agreement also commits the Afghan Government to release 5,000 Taliban prisoners, and the Taliban to release 1,000 captured Afghan Army soldiers.

As a potential permanent peace inches closer in Afghanistan, US policy for the “Greater Caspian region,” the area stretching from India to the Black and Mediterranean Seas with the Caspian Sea at the center, needs to come into sharper focus. A key facet of this policy is the potential for new energy, cargo, and data logistics lines to help stabilize a post-peace Afghanistan and generate new patterns of cooperation that could either complement or compete with China’s Belt and Road Initiative (BRI) and Russia’s Eurasian Economic Union.

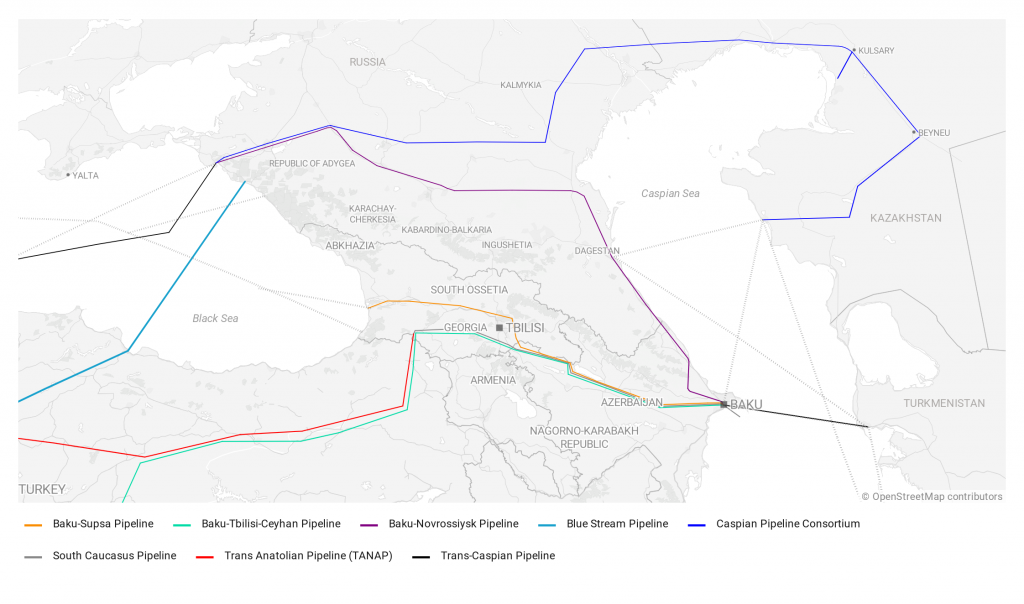

This vision of an economic cooperation corridor from Central Asia to Europe via the Caspian Sea is not new. I spent more than half of my twenty-three-year diplomatic career at the center of US government efforts to establish a network of oil and natural gas pipelines from the Caspian Sea to the Black Sea and Mediterranean, working together with Azerbaijan, Georgia, and Turkey, as well as BP, the State Oil Company of the Azerbaijan Republic (SOCAR), and other oil companies. These pipelines were:

- Baku-Supsa for oil from Azerbaijan to Georgia’s Black Sea coast;

- Baku-Tbilisi-Ceyhan (BTC) for oil from Azerbaijan to Turkey’s Mediterranean coast;

- Baku-Novorossiysk for oil from Azerbaijan to Russia’s Black Sea coast;

- Caspian Pipeline Consortium (CPC) for oil from Kazakhstan also to Russia’s port of Novorossiysk; and

- South Caucasus Pipeline (SCP) for natural gas from Azerbaijan to Turkey, (which is expanding today into the European Union’s (EU) Southern Corridor).

These pipelines on the western side of the Caspian, however, represent only half of the strategic vision shared by Washington, Ankara, and eventually the EU: cross-Caspian export routes for Central Asian oil and gas, independent of Russian monopoly power, have been the second key element, but they have yet to materialize. Indeed, the CPC pipeline perpetuates Russia’s near-monopoly on oil exports from Central Asia, while Chevron and ExxonMobil have exported only modest oil volumes from Kazakhstan via tankers to Azerbaijan and BTC. And no Caspian natural gas has ever been exported westward other than via pipelines operated by Gazprom, which is controlled by the Russian government.

Despite Washington’s inclusion of two oil pipelines transiting Russia in its regional energy security strategy, Moscow has consistently opposed any pipeline that might weaken the monopoly power of either Gazprom or Transneft, (Russia’s state-owned oil pipeline monopoly). As a Russian deputy foreign minister told me privately in 2001, “The core of our Caspian energy policy is to maximize the flow of oil and gas through Russian pipelines.”

Moscow has proven adept at stifling a key project strongly supported by Washington and Ankara beginning since the mid-1990s, the Trans-Caspian Pipeline (TCP), intended to deliver natural gas from Turkmenistan to Azerbaijan. The Kremlin has used both spurious environmental and legal arguments and brutal intimidation of Turkmenistan’s leaders to oppose TPC.1In the autumn of 2000, then-President of Turkmenistan Sapamurat Niyazov told a US diplomatic colleague and me in his presidential office that Russian officials suggested they would destabilize Turkmenistan and perhaps threaten his life were he to proceed with TCP. Moscow has also created facts on the ground. Gazprom’s Blue Stream Pipeline, proposed to Ankara at the end of 1997 and completed in 2002, delivers same volumes of gas delivered to Turkey that could have come from TPC, but via Russia and under the Black Sea.

These Russian efforts to thwart TCP received a boost from a purely economic source, BP’s 1998 discovery of the mammoth Shah Deniz natural gas (and condensate) field in Azerbaijan’s Caspian waters. This discovery eliminated Baku’s economic incentive to cooperate with Ashgabat on shipments of Turkmenistan’s gas, as Turkey became the main market for Shah Deniz as well.

TCP has therefore languished on strategic drawing boards for over twenty years. However, new glimmers of hope for the project may have emerged. Several participants cited renewed US political support for TCP by US President Donald J. Trump in his Novruz holiday letters last spring to President Ilham Aliyev of Azerbaijan and President Gurbanguly Berdymukhamedov of Turkmenistan. More recently and during his early February visits to Kazakhstan and Uzbekistan, US Secretary of State Mike Pompeo stressed the United States’ desire to help Central Asian countries develop alternatives to China’s BRI and Russia’s Eurasian Economic Union for building inter-regional economic cooperation. TCP could be one of those alternatives.

Moreover, Azerbaijan may now have an economic incentive to welcome TCP. Despite significant natural gas production at Shah Deniz and other fields, Azerbaijan is unable to meet industrial demand from domestic supplies alone, thanks to the country’s burgeoning petrochemical sector. Additional gas supplies from Turkmenistan could provide an answer.

There is hope that Russia might be softening its opposition to TCP in the wake of the August 2018 Convention on the Legal Status of the Caspian Sea. That agreement, signed by Russia, Turkmenistan, Azerbaijan, Kazakhstan, and Iran, resolved some of the territorial disagreements among the Caspian Sea’s littoral states that Moscow previously cited in opposing TCP. Unfortunately, this is not the case. On the contrary, Russia, together with Iran, continues to oppose TCP for political reasons, citing supposed concerns about the endangered Caspian seal and sturgeon, (ignoring the legacy of environmental degradation of Caspian waters from Soviet-era oil pipelines).

Beyond words, Moscow is also taking concrete action to maximize the flow of Central Asian crude through Russian pipelines rather than the Azerbaijan-Georgia corridor. Working with their state oil pipeline monopoly Transneft and state oil company Rosneft, Russian authorities have been investing heavily in the Caspian Sea port of Makhachkala, the capital of the Russian Republic of Dagestan. Oil imports into Makhachkala, thus increased by 200 percent in 2018 over the previous year, and then another 100 percent in 2019. Part of this latter increase resulted when oil shipments from Turkmenistan and Kazakhstan to Baku were diverted to Makhachkala in January 2019 due to a dispute between SOCAR and the Swiss-Dutch oil trading giant, Vitol.

US sanctions could conceivably threaten the reliability of this new Makhachkala oil export route. The Russian owners of one Caspian tanker, VEB-Leasing OJSC, were already under US sanctions when Vitol chartered it in early 2019 to transport crude from Turkmenistan to Makhachkala. Then on February 17, 2020, the United States applied new sanctions against Rosneft, a key buyer of crude at Makhachkala, for supporting the Maduro regime in Venezuela.

Additionally, there is growing evidence of Russian intent to use Makhachkala to help circumvent US sanctions against Iranian oil exports. As reported in early 2019 in Dagjournal, an official publication of Russia’s Republic of Dagestan, Iranian oil could be shipped to Makhachkala and blended with crude from other suppliers, which would then be sold in Europe; in exchange, Iran would receive food, medicine, and other basic commodities. Although such a barter arrangement involving Iranian oil would violate US sanctions, the Financial Times reported in July 2019 that Moscow had signaled it would explore “ways to facilitate or finance Iranian oil exports.”

Subscribe for the latest on Central Asia

Receive updates for events, news, and publications on Central Asia from the Atlantic Council.

Given US sanctions against Russia’s and Iran’s oil sectors, the Azerbaijan-Georgia corridor to the Black Sea and Turkey would appear more reliable than the Makhachkala route. Indeed, for nearly twenty years, the US military has resupplied its forces in Afghanistan via this route, which parallels the BTC and SCP pipelines, then extends across the Caspian Sea into Kazakhstan, Uzbekistan, and Turkmenistan and onward to Afghanistan. Launched by then-President of Azerbaijan Heydar Aliyev in a phone call to then-US President George W. Bush a day after the terror attacks of September 11, 2001, this route grew to deliver one-third of all fuel and materiel destined for US and Coalition forces in Afghanistan.

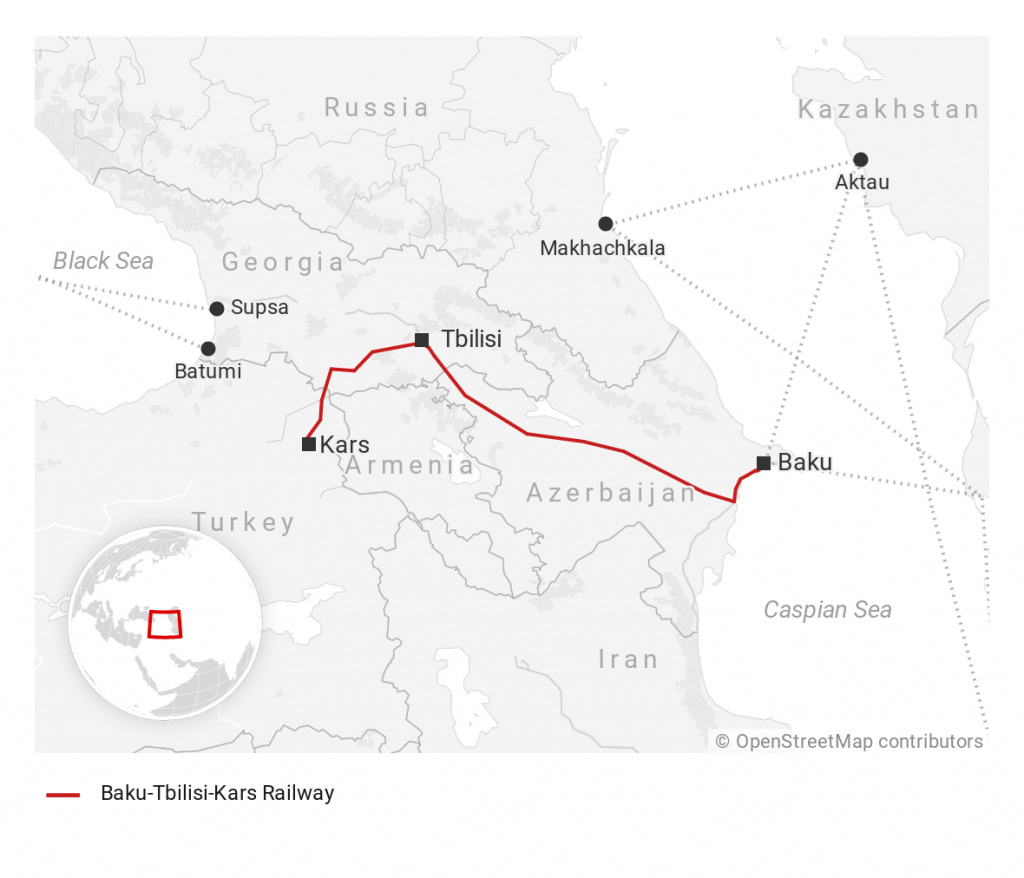

Today, this corridor is expanding, with a full range of cargo now complementing military logistics routes. The Baku-Tbilisi-Kars rail connection, inaugurated in October 2017, is the shortest rail link between Europe and Asia. Data transport is also becoming part of the Greater Caspian Region’s transport corridors. Azerbaijani telecom company Azertelecom is establishing a fiber-optic link between southeast Europe and China that will traverse the Georgia-Azerbaijan corridor, travel under the Caspian Sea, and extend throughout Central Asia (a project that I am a strategic consultant for).

Afghanistan, however, remains on the periphery of these new trade flows. Afghanistan urgently needs new logistical connections to help catalyze economic stability and growth with the new peace agreement.

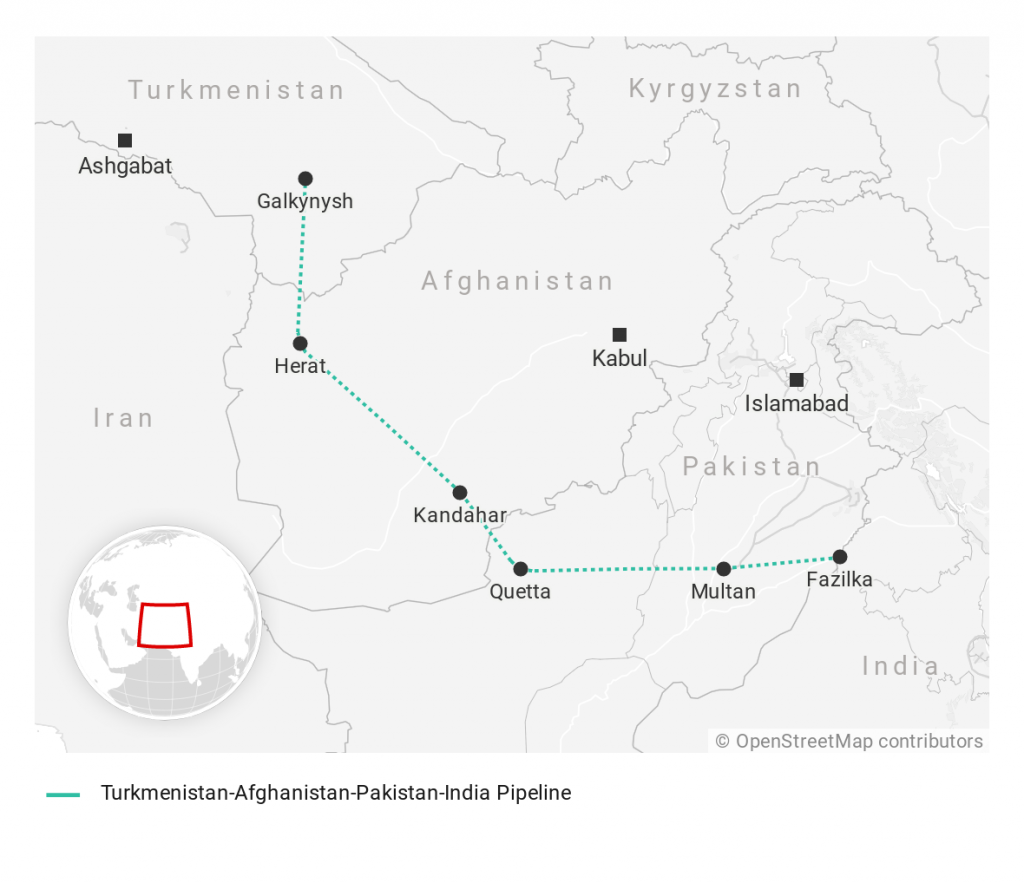

Turkmenistan can play a key role in providing these connections. To the northwest, Turkmenistan physically links Afghanistan to the Caspian Sea and transit links to Europe via the Black Sea and Turkey. To the southeast, Turkmenistan’s natural gas reserves (the world’s fourth-largest), can enable Afghanistan to become part of a regional energy trading network via the notional Turkmenistan-Afghanistan-Pakistan-India (TAPI).

Like TCP, TAPI has enjoyed periodic support from Washington since the early 1990s, when private oil company Unocal and the US government began drawing strategic lines on the map. TAPI would deliver Turkmenistani natural gas to energy-starved markets in Pakistan and India, with Afghanistan gaining transit revenues.

Despite several declarations that construction has begun, TAPI has never really gotten off the ground. The $8 to $10 billion project faces serious financing hurdles stemming from daunting political risks, especially its need to transit Taliban-controlled territory in Afghanistan’s Herat Province. Moreover, TAPI’s revenues would flow to the corruption-plagued Afghan government rather than directly benefiting local citizens of Afghanistan. As a result, TAPI is unlikely to generate the requisite local popular support required to deter attacks on the pipeline by militants who seek ransom payments from Kabul. Meanwhile, Russia and China are maneuvering to participate in TAPI, given the project’s high political profile, and thereby circumscribe the TAPI countries’ options for geo-economic influence independence.

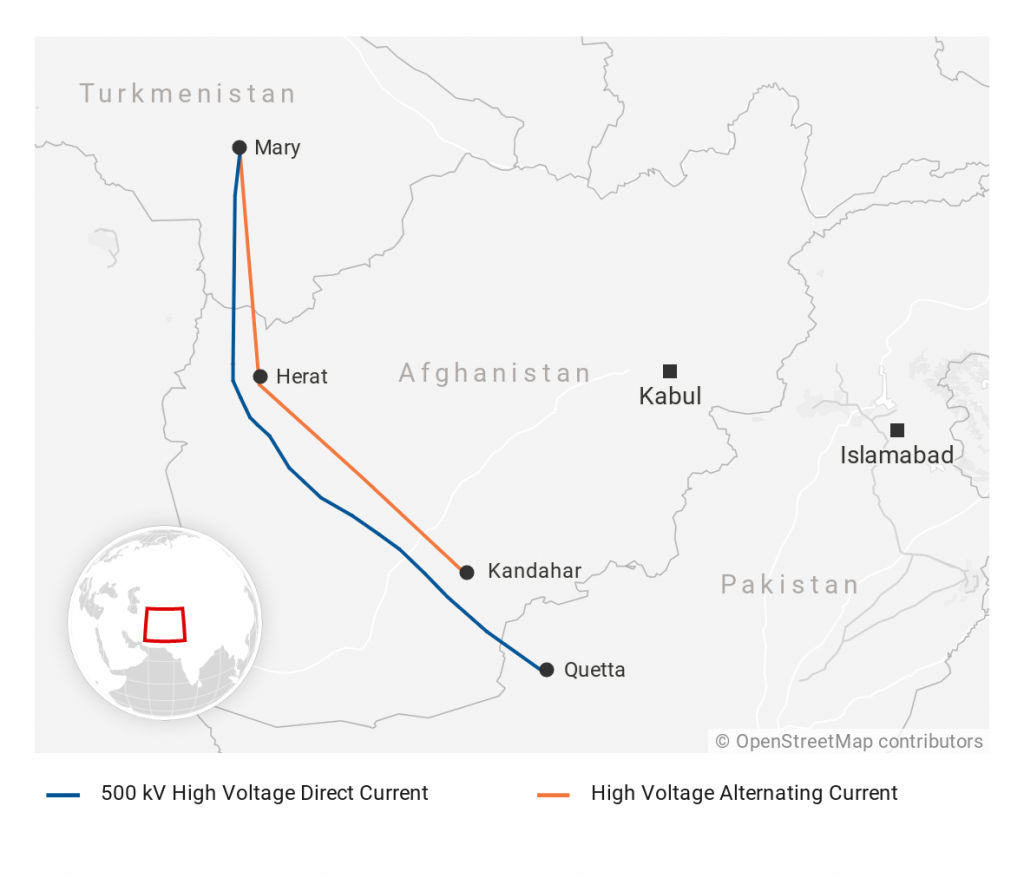

There are plans for future projects that could mitigate these obstacles to TAPI, and maybe even generate geo-economic benefits for Afghanistan that far outweigh those of TAPI. TAPP, which is being developed by the private Turkish company Calik Enerji, aims to export electricity generated from locally produced gas in a power plant in Turkmenistan to Afghanistan, Pakistan, and India in two phases.

TAPP’s first phase is crucial: it would comprise a modest transmission line to deliver electricity to Afghan people in Herat and other provinces who have never had access to electricity. Unlike a gas pipeline, whose transit fees would disappear into the Kabul bureaucracy, TAPP’s initial power line would provide tangible and life-changing benefits to individual citizens of Afghanistan, namely, their first-ever supplies of electricity. It can be assumed that Afghans would become supporters of a Turkmenistan-Afghanistan electricity corridor. And, because the Taliban’s ultimate goal is to win the hearts and minds of the Afghan people, the militants would be loath to destroy the power line.

Building on the positive political momentum of Phase 1, TAPP’s second phase would be a significantly larger transmission line to carry electricity from Turkmenistan across Afghanistan to Pakistan’s Balochistan, another region whose residents historically have never enjoyed sufficient access to electricity. If the project is successful in Pakistan, an extension to India could eventually be contemplated. Planning for TAPP is moving forward. While it will need political and regulatory support from the countries along its route, as well as possible security support from the United States, it is a commercial project. It, therefore, offers a free-market alternative to the state-centric approaches of Russia’s Eurasian Economic Union and China’s BRI. And, if TAPP succeeds, it can help cement a hoped-for Afghan peace agreement, while accelerating the development of the other logistics corridors throughout the Greater Caspian Region that can provide optionality for the countries of South and Central Asia as they navigate their way through BRI and the Eurasian Economic Union.

Matthew Bryza is a senior fellow with the Atlantic Council Global Energy Center. He served as a US diplomat for over two decades, including as US ambassador to Azerbaijan and deputy assistant secretary of European and Eurasian affairs. You can follow him on Twitter @BryzaMatthew

Further reading:

The Global Energy Center develops and promotes pragmatic and nonpartisan policy solutions designed to advance global energy security, enhance economic opportunity, and accelerate pathways to net-zero emissions.

The Eurasia Center’s mission is to enhance transatlantic cooperation in promoting stability, democratic values, and prosperity in Eurasia, from Eastern Europe and Turkey in the West to the Caucasus, Russia, and Central Asia in the East.

Image: An aerial view of the Caspian Sea near the city of Baku is pictured through the window of Turkish Airlines airplane, ahead of Europa League Final, in Baku Azerbaijan May 27, 2019. REUTERS/Amr Abdallah Dalsh