The global economy in 2020, by the numbers

The pandemic has made this a historic year for the global economy, now beset by a recession the likes of which we haven’t seen since the Great Depression. To make sense of it all, our GeoEconomics staff and senior fellows have selected the numbers behind the headlines, organized around our three pillars of work, that best capture the global economy’s journey in 2020—and what lies in store for 2021.

Future of Capitalism

Learn moreFrom lockdowns that crippled small businesses and supply chains and put millions out of work, to worsening inequality in the United States and abroad, the pandemic has tested the ability of local, national, and multilateral institutions—alongside the capacity of the private sector—to respond, mitigate catastrophic impact, and stimulate an inclusive recovery: one that “builds back better.”

These are the rates of unemployment, respectively, of Black, Latino, Asian, and White Americans in November. The differences highlight the persistent, structural racial inequality that has been accelerated by the pandemic and worsened long-standing educational, employment, and financial inequities.

And in the bigger picture in the U.S.…

This is the number of long-term unemployed people (out of work for twenty-seven weeks or longer) in the United States in November 2020. They comprise about 37 percent of the total unemployed population, nearly approaching the record high ratio of more than 40 percent reached after the Great Financial Crisis.

The share of long-term unemployed people is likely to rise further and cause hardships for many working people, regardless of the outcome of the new round of stimulus. The longer a person is unemployed, the more difficult it is for that person to get a job. As a result, the employment situation will take longer to come back to normal—a dynamic we witnessed in the labor market after the Great Financial Crisis. This will act as a headwind against economic recovery in the year ahead, unless it is addressed through resolute policy actions by the incoming administration of President-elect Joe Biden.

Meanwhile, around the world, no country or demographic group has been spared—except China:

This represents the number of people who could fall back into extreme poverty in 2020 as a result of the pandemic. This estimate, in a report by the World Bank, highlights the pandemic’s damage to inclusive growth, especially in middle-income countries.

Eradicating poverty is the first of the seventeen United Nations Sustainable Development Goals (SDGs), but these estimates suggest a setback to the goal. International commitment to reaching the SDGs by 2030 remains intact. If placed at the heart of decision-making, these seventeen objectives can serve as goalposts for the policies that will be needed to rebuild sustainable economies in the aftermath of the pandemic.

That’s the amount of money middle-income countries stand to lose, with estimated earnings losses for individuals amounting to $6,777, due to this year’s COVID-19 school closures. That loss of income may result in as much as a 15- to 22-percent drop in gross domestic product (GDP). To minimize these losses, governments—with multilateral funders and corporate partners—need to move quickly to shore up digital access and quality online and blended learning, while ramping up testing and investing in hygienic educational infrastructure to safely reopen schools as vaccines become more available. This year, COVID-19 has disrupted education and created childcare crises.

Around the world, women’s jobs are estimated to be 1.8 times more vulnerable to the pandemic than men’s jobs. While overall unemployment rates in the United States skyrocketed due to the pandemic (with an over-the-month increase of 10.3 percentage points in April 2020), women have been affected by the crisis much more severely–often due to increased demand for unpaid caregiving, which is disproportionately performed by women. There ae also other factors at play, such as a more fragile employment environment, a lack of access to labor and social protections, and the fact that female-dominated sectors have been more heavily impacted by COVID-19. If this trend were to persist, it could mean a decrease of $1 trillion in global GDP growth in 2030. For the incoming Biden administration, “Building Back Better” has to focus on gender-responsive recovery, including investments in the childcare sector and progressive work policies for caregivers, to avoid long-term effects on women’s job prospects and global growth.

That’s China’s projected GDP growth in 2020. This small but positive number means China is one of the few countries in the world—and the largest by far—to experience economic growth during the year of the pandemic. It is an amazing feat that Beijing produced by quickly containing COVID-19, restarting the manufacturing sector, and deepening regional trade partnerships with countries like Vietnam. It also means that the world will experience “fractured growth”—where one major economy grows while all the others contract—for the first time in decades. What kind of strains will this put on our global economic recovery and how will it all spill over into our geopolitics? That’s the question we’ll be asking—and trying to answer—in 2021.

Related reading:

Here’s how the world is coordinating its economic response:

During the 2020 pandemic, the International Monetary Fund (IMF) provided some sort of emergency financial aid or relief to eighty-three of its member countries, adding up to just over $100 billion of assistance. Most emergency programs amount to 1 percent of a country’s GDP and, as such, only relieve the most immediate budgetary or balance-of-payment pressures. As the Group of Twenty (G20) and others have pointed out, countries with debt and budgetary problems will need a longer-term strategy. The seventy-five poorest countries in the world comprise about 3 percent of global GDP and their aggregate debt is a bit over $1 trillion. A combined effort by the multilateral investment banks, the Group of Seven (G7), the G20, and others like the Paris Club should be able to set the recovery path for these countries on a sustainable financial basis.

The future of money

Learn moreDebt took center stage as governments struggled to finance their emergency relief, reopen schools and the economy, and plan for vaccines and more inclusive growth. At the same time, the use of digital currencies surged and new tools were deployed to help those hit hardest by the crisis.

Speaking of debt:

JP Morgan Chase Bank reports that it is clearing $2.8 trillion in wire payments each day globally in 2020, the equivalent of moving America’s GDP on a weekly basis. For all the talk of sanctions overuse possibly undermining the US dollar, any actions by the United States would have to be so drastic as to displace the financial gravity that the US financial system exerts. The US market is defined by the deepest and most liquid pool of government debt in the world, unfettered movement of capital, and strong property rights. Foreign holdings of US public debt increased during the pandemic-related financial crisis despite a major economic slowdown in the United States. Could sanctions, if used so carelessly that confidence in US markets is undermined, cause such a displacement of the US financial system’s gravity? Absolutely, which is why the Biden administration’s pledge to be vigilant in protecting US financial hegemony while using sanctions is critical.

This is the increase in global central-bank assets during the initial response to simultaneous supply and demand shocks associated with this year’s pandemic, as estimated by the Financial Stability Board. This is more than double the increase in central-bank assets during the Great Financial Crisis, which happened over a longer period (2008-2009). Central banks are now large—and, in many cases, the largest single—purchasers of private-sector and public-sector securities in all advanced economies. These purchases deliver financial stability, but they raise serious questions about monetary policy and the risks of a potential post-quantitative easing “taper tantrum” when the pandemic wanes.

The size of the bubbles corresponds to the size of a country’s GDP. The position (left or right) shows how much quantitative easing they’ve done relative to their size.

Related reading:

This is the astonishing debt-to-GDP ratio forecasted for the United States at the end of 2025. Historically, US public debt has been contained between 40 and 60 percent of GDP in the post-World War II era. Only recently, after the Great Financial Crisis, has it started to rise. Are US citizens ready to coexist with such a high public debt for a long time? Will Congress manage to raise the debt ceiling smoothly over time? Will the world continue to consider Treasury notes a safe asset?

Related reading:

Meanwhile, in the cyber world:

The US Department of Justice announced plans to seize 280 cryptocurrency accounts held by North Korean hackers. In March, the US Treasury Department imposed sanctions on two Chinese nationals for laundering $100 million on behalf of the hackers. Pyongyang’s cyber capabilities have advanced dramatically since the 2014 Sony Pictures hack. Today, its cybercrimes include ransomware, bank theft, and hacking into companies working in defense, intelligence, and COVID-19 vaccine development. Sanctions have done little to counter the crimes. Even if Washington and Pyongyang engage in nuclear talks again, it will be impossible to reverse Pyongyang’s cyber capabilities unless action is taken now to slow it down. Improved coordination between the private sector and governments will help reduce cybercrime, and proactive private-industry measures will help protect the integrity of the global financial system. Banks and facilitators wittingly helping North Korea and its front companies should be named, shamed, and penalized.

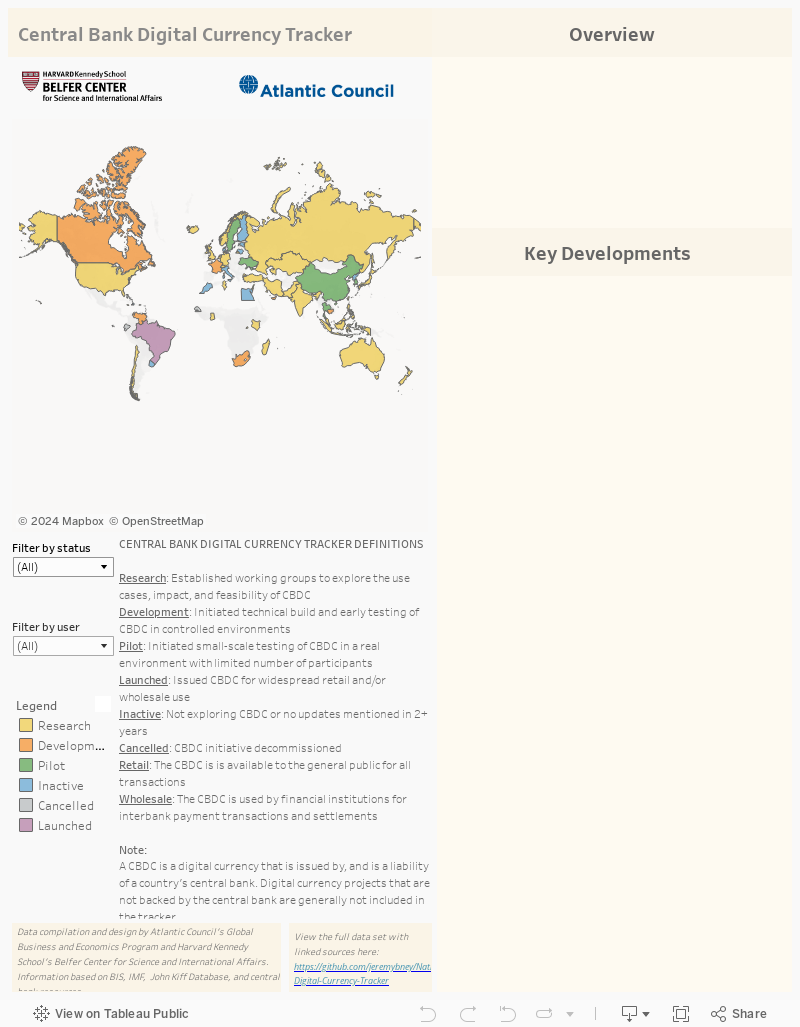

This was the year of the Central Bank Digital Currency (CBDC). One hundred is the maximum value for the Google Search Index, which measures the twelve-week moving average of worldwide search interest for specific search terms in relation to the average peak that the search terms experienced. In a search index run on the terms “Central Bank Digital Currency,” “Facebook Libra,” and “Bitcoin,” each term experienced its own peak over the past three years: Bitcoin reached a peak in the first quarter of 2018, Facebook Libra in the third quarter of 2019, and Central Bank Digital Currency in the third quarter of 2020. CBDC’s rapid gains came at the expense of Bitcoin and Libra this year, whose searches both slumped.

European Union (EU) leaders agreed in July to a €1.1 trillion budget plan for 2021-2027 and a one-off €750 billion COVID-19 recovery fund, marking the first instance of a pan-EU stabilization instrument and the first EU joint debt issuance to finance grants to member states. This wasn’t just about solidarity; enlightened self-interest drove Germany, France, and other northern member states. Their support will pay off later through cross-border demand for their exports and sounder financial and political stability in the region. If countries that receive support gain credibility by putting together sound, forward-looking investment plans and undertaking overdue domestic reforms, that may lead to a more permanent stabilization mechanism—a key missing piece in the EU’s architecture.

On a more optimistic note, social-impact instruments are having a moment:

This is the latest size of the global impact-investment market as reported this year. These are investments that strive to create positive social outcomes along with a competitive financial return for investors. While the amount appears to be substantial, it is only about 0.75 percent of total global assets under management. Impact investing must expand dramatically to fund sustainable and inclusive development at the levels required by underserved communities around the world (and as outlined by the UN’s Sustainable Development Goals). Governments should adopt impact investing (including labeled bonds) as a central strategy to achieve their development and global human-security goals, and governments should work in partnership with financial firms, development finance institutions, and foundations to remove the barriers that are keeping impact investments to a trivial share of global equity and bonds markets.

The future of economic statecraft

Learn moreIt was overshadowed by the pandemic, but this year also witnessed significant trade shakeups, regulatory actions, and sanctions activity, underscoring the need for the Biden administration to rethink how the United States deploys the potent tools of economic diplomacy.

Heading into 2020, nearly 39 million US jobs were supported by international trade while 95 percent of global consumers were located outside the United States. These global consumers provide great opportunities for US companies and workers. The Trump administration heavily favored a defensive strategy to protect the US market rather than the offense required to open and expand overseas markets for US products. As the Biden administration invests in making America’s economy, workers, and innovation environment more competitive and productive, it must simultaneously revisit the use of economic tools and the United States’ international networks and partnerships to create new opportunities for American goods and services. This should include a revitalized strategy for commercial and economic diplomacy backed by a whole-of-government effort and a careful review of the tools and partnerships available, including sanctions and export controls, to protect and promote America’s global competitiveness.

That’s how many US federal regulations proposed in 2020 mentioned “retrospective review,” representing about 1 percent of all regulations issued this year. Retrospective review, which refers to analyzing how past regulations actually performed, provides real-world support for agencies to decide whether to repeal, expand, or redesign regulations going forward. Although every president has advocated for such reviews, no president has succeeded in successfully prioritizing their implementation. Hopefully, the Biden administration will bolster its commitment to a regulatory policy that benefits society by building a robust practice of retrospective review.

This is the Organization for Economic Cooperation and Development’s (OECD) estimate of foregone revenue for national treasuries as a result of multinational corporations avoiding taxes. A 137-country initiative steered by the OECD may nearly halve that figure. As part of the initiative, countries in which multinational corporations operate would receive some taxing powers in a similar manner to how the United States apportions the tax bases of companies operating across states. The initiative would also ensure that large multinational corporations pay a minimum level of tax. The US Tax Cuts and Jobs Act contains such clauses. Transatlantic leadership in these negotiations may prevent a spiral of protectionism, boost the capacity of countries involved in the initiative to recover from pandemic-fueled economic crises, and improve the perception of their legitimacy and inclusiveness.

This is the latest number of specially designated nationals (SDNs) identified by the US Office of Foreign Assets Control (OFAC) as of mid-December, according to the sanctions-intelligence start-up Castellum.AI. It reflects the Trump administration’s steady march of sanctions escalation: From Iran, to Venezuela, to Russia, and now to China, “maximum pressure” became the policy of first resort under a new executive order, with mixed results. But setting aside a likely reversal of the Trump administration’s widely criticized sanctioning of the International Criminal Court, any effort by the Biden administration to relieve Trump-era sanctions will cede US leverage, however ineffective the Trump administration’s efforts may have been. And the new administration will face no shortage of sanctionable behavior.

Stay with us in 2021 as we track and analyze the economic recovery from COVID-19 and all other developments related to trade, sanctions, diplomacy, monetary policy, and inclusive growth. We’ll continue to offer rapid responses, candid and incisive insights, and data visualizations regarding geoeconomic events and trends, along with the responses of the Biden administration, other governments, and the Bretton Woods institutions.

Image: Reuters